Kolkata’s ravishing music star Roy has received numerous prestigious national awards for his works, including but not limited to- the 64th National Film Award for best lyrics for the song Tumi Jaake Bhalobasho, and the 61st Filmfare Award for best music director and best background score for Piku.

In this first-ever deal with Saregama, Roy intends to produce independent music adding to his stellar set of widely adored singles and albums. Currently, the Saregama team and Roy are collectively working on a pop-set for Valentine’s Day this year.

Vikram Mehra, Managing Director Saregama India, said, “It has been Saregama’s belief that regional music consumption will hold a definitive stronghold over the entire Indian music landscape. We are betting big on regional tunes and stories. Taking a leap in the Bengali music space, we look forward to this long-term association with Anupam Roy, who I believe is one of the greatest present-day Bengali musicians. We hope to create music that passes on for generations to come with Anupam.”

Given Subscription as a kicker is called out by Vikram as next growth driver( beyond organic growth of 25%), some data from Spotify - Subscription already at 65% of their reported revenue( though data is for FY 20, focus on Subscription would have continued )

FY20. The Indian entity of the Stockholm-based company has recorded Rs 16.12 crore in operating revenue during the financial year ending March 2020. Spotify India makes money through subscriptions and advertising. Income from subscriptions contributed about 65%~ Rs 9.75 crore ~ to the total revenue in FY20

That said, homegrown platform Gaana’s FY21 results didn’t show any growth in revenue. According to Fintrackr , growth in its operating revenue remained almost flat in FY21 as it grew by a mere 2.65% to Rs 123 crore as compared to Rs 120 crore in FY20.

While Gaana has ambition of 500MAU by 2025 per media articles ( sub 200M currently), can they afford to grow by one metric while topline staying flat? Spotify is under pressure globally and MAU growth India holds key for them, however Subscription seem to be a clear focus for them - Industry can’t show Divergence for long, if one key player is going Subscription path, others will follow suit sooner or later.

If anyone has latest on Subscription status industry/company , kindly share.

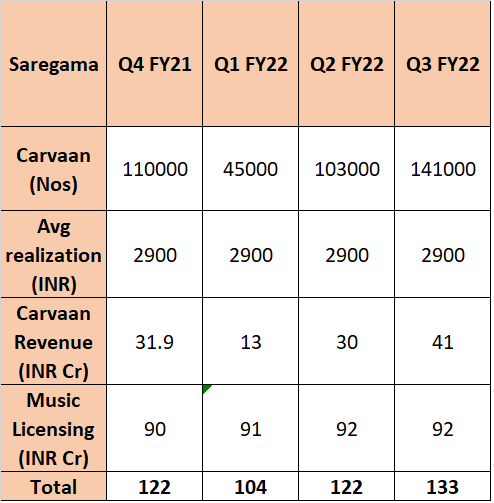

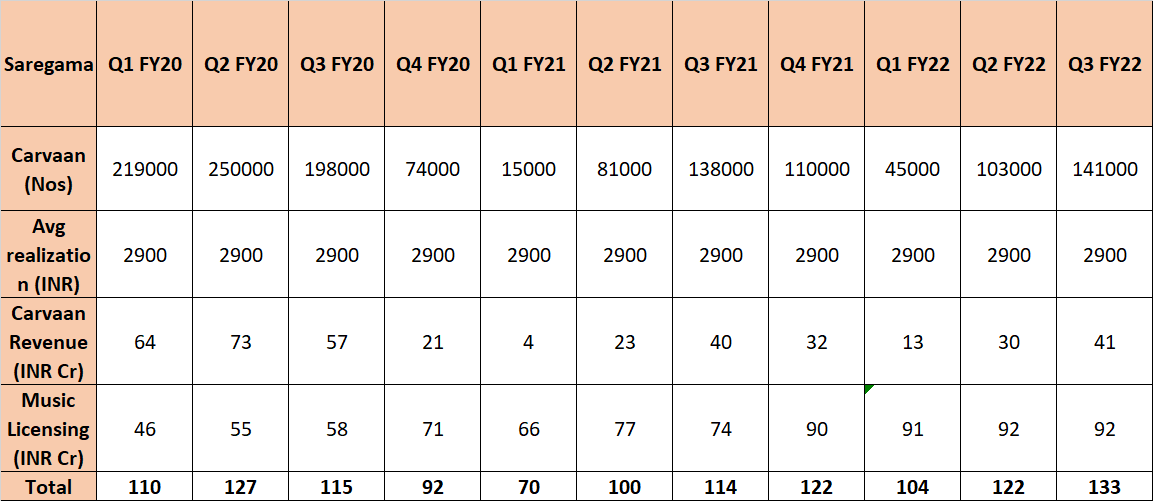

I tried to divide the music revenues in past 4 Quarters between Carvaan and licensing. Managed to create below table (I had Carvaan unit sales realization to be around INR 3000 basis last AY, if its wrong please point out)

Your numbers are more or less as per my thinking and I’m disappointed. For me streaming revenue is of paramount interest. Growth narrative and valuations mismatch may be there in the near to medium term in my personal opinion and my entry price doesn’t have much margin of safety, so I have sold out today - which is not a recommendation for buy/ sell as I’m not sebi registered analyst.

It is 16X sales, 50X EBDITA type valuations at current Qtr annualized ( if taken purely for Music streaming its 25X+ sales)

Mgmt own guidance has been 20-25% growth trajectory, seem to be very well factored in

QoQ growth on streaming is missing/flattish for Saregama as well as Tips, been a pattern for few qtrs now

Tseries which has multifold subscribers has YT revenue share sub 20%, so this segment can’t move needle much

All key licensing deals are done with all platforms ( majority) -unless renewals happen at bump up, delta may not be much - need to understand more on call

Most music streaming platforms are reporting flat rev growth and are loss making, though MAU may be increasing, any re negotiations on per streaming chances look bleak

New Content quality on YT seem to be mixed, again YT being small pie in revenue, alone can’t move needle much unless growth is hyper - can subscribers base/views grow 2-3 X every year, given high base now?

Higher share of films, Carvaan may help consol topline but don’t have similar returns profile.IMO these two seem to be more in mgmt control currently, Carvaan affinity may cost margins if mgmt decides to push aggressively - a risk though mgmt clarified earlier.

Sector is fantastic, and mgmt may continue to deliver 20%+ growth, to justify current valuations and deliver higher growth, trends like subscription model picking up , content finding consumption in new high growth verticals such as gaming etc is needed.

Would be interesting to hear mgmt commentary in concall on next leg of growth strategy, QIP utilization, subscription trend, any new monetization channels etc.

Went back a few more quarters to look at licensing revenue growth. Full covid impact starts from Q1 FY21, so it can be safely assumed that most of the licensing revenue since this quarter is online music streaming/licensing with no physical licensing component.

It seems the streaming revenues may be lumpy. The rates remain uniform for the period of contract with streaming platforms and then jump when contract renewal happens. Seems like renewal cycle is April-March judging by jump from 74Cr to 90Cr in Q1 FY22 and flat revenues for next 2 Qtrs. Vikram addressed this in Q3 FY21 concall

So we should wait till Q1 FY23 results are out before concluding whether music streaming can keep growing at 25-30% per year or not. What seems to be clear is # of streams is not growing much Q-o-Q, but its possible that Saregama negotiates a price hike with streaming platforms (Even a 1.5 paisa hike increases streaming revenue by 15%; Another 10-15% growth in #streams next year can increase segmental revenue by 25-30%. So its not completely unrealistic)

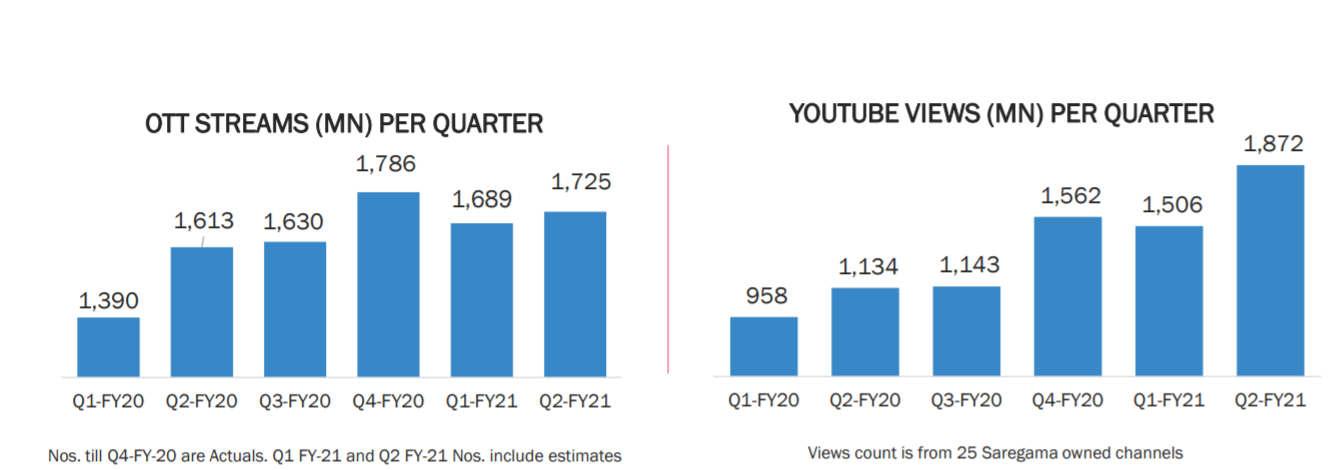

By the way, why did they stop publishing the number of streams metric in their investor presentation since Q2 FY21? I couldn’t find any answers in the concall transcripts as well. This action does make it seem like the metric was flattening out and management didn’t want to highlight that.

Can someone please explain me why is the caravan segment so looked down upon and why cant it be a successful product ? Also would love Ishmohit’s view on the results

In my view saregama doing miss-allocation of funds, sometime ago they were raised QIP round for 700cr, & now they are declared dividend of ₹30 per share, approximate 57cr. of fund out from the balancesheet, as such cash generating businesses doesn’t required external funds, also they keep run loss making Magazine segment too.

Curious, how is this dividend related to the fund raise? They have declared Rs 30/share dividend which is about 40% of FY22 expected PAT. Last year they declared Rs 20/share dividend which was 30% of FY21 PAT. And if I am not wrong they have declared dividends each year for the last 7 consecutive years.

The fund-raise size may well be too large to deploy but declaring Rs. 30/share dividend may not be the reason for calling it so. However, I do think acquiring music IP is not going to be a cheap affair for Saregama as every target company knows Saregama is sitting on a lot of cash with promises of fast growth to its investors. Curious to hear what Management has to say about the QIP money tomorrow.

Although I have not ever read their magazine yet, I believe it is also a cheap way of marketing. They can pump in as ads as much they want.

If you revisit the concall and commentary from Vikram Mehra, you can connect some points mentioned by fellow investors out here and what we see in the results.

As @nirvana_laha mentioned above music streaming apps revenue may be or may not be under pressure for stupendous growth with the current content. Now coming to asset allocation, Vikram Mehra seems to be clear about the decision if something does not come on his way. I said that because he has mentioned something like this “We will try push carvaan as much as possible right after 3rd wave as the production from china back to normal. If it does not go well (overall carvaan segment) they will be even ready to stop trying for that”. He sees saregama as an IP ownership company rather than trying many things and ends up being “jack of nothing”.

About the movie segment, There are no plans to splash money out in high budget Bollywood/other industries. For me, the vision is clear, investing in industries like Malayalam is like investing in small-caps with a moat. I can explain it, Malayalam movies are generally low budget movies with high art value. That means, at the moment they will be able to own the IP of the high art value movie which can be just dubbed and pushed to the audience across India.

QIP fund raised was resulting in equity share dilution means your percentage of ownership is reduced,

let’s assume company required 700cr. of fund so, they could raise only 650cr. of funds & another 50cr. came from internal funds(not declaring dividends),

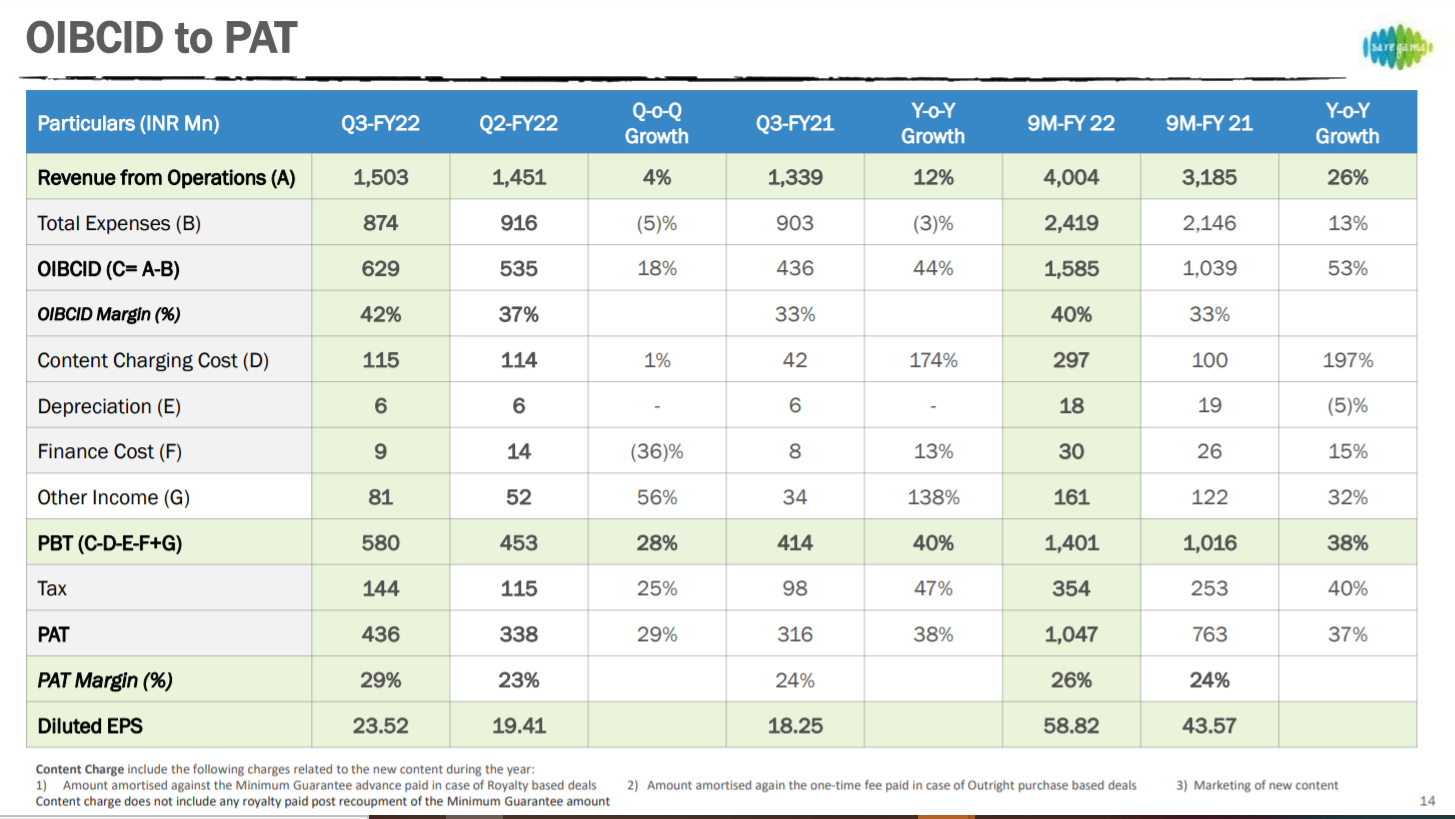

Quarterly numbers distort the picture because of film business. Always is rolling 12/9 months.

OIBCID margin number should be 32-33%. It seems high today at 42% because there were no major movie cost writing off.

Pani Pani became biggest hit of 2021. But if you look at top 20 there will be more Saregama songs.

165 songs released this quarter.

Two deals in licensing: Chingari & Planet Marathi

20% growth is coming from → Industry growing(11%) + constant increase in market share

We are going to be aggressive in new music but not any content at any cost.

Public performance was hit this quarter. This generally comes near New year and give bump to Q4. But it wont happen this year.

141,000 Caravan Sales: Everything is happening on Zero marketing expense. It is all pull demand.

Every unit under Caravan is break-even.

No films or web series were released this year but two web series are almost complete and already licensed to another platforms.

We have no intend to do big budget films. We can do small regional movies.

Web-series will only be pre-licensing basis like giving to digital players

They spent money/start making the web series only when they sign pre-licensing deal.

Q3 is the time where most brands advertise a lot and that is when we get more revenues.

“We are preparing this company for big growth.” - Vikram Metha, CEO

For majority of old songs they have only audio rights that is why they don’t have the video on the YouTube channel.

Q: Streaming business is roughly flat quarterly basis.

Answer: look at yearly revenue because contracts are yearly contracts and minimum guarantee comes in quarter basis but over flow comes at the end of contract, hence you see bump at the end of the year.

Every time they renew the contract they try to increase the minimum guarantee

The push towards paid subscription is not great as of today.

Streaming business is not sustainable only on advertising.

Globally paid subscribers crossed 500 million.

Older generation population have also started listening to music due to pandemic and they tend to prefer old songs.

They are investing in film business: Karan Johar and Leela Banali (2 movies), Ranveer Singh with a famous reginal director, etc.

They are also interested in nurturing the new talent but right now they are doing business with top talent.

Find new talent and give them chance to get featured in big Saregama songs and Saregama gets commission from their activities.

They raised money to strategically look for acquisition of music label or buying out catalogue. They will let the investors know when something is ready.

All the funds raise is for music business.

25-30% growth guidance for music & film business is with organic or inorganic growth next 3-5 years.

This guidance does not include industry structure shifting towards paid revenue model.

Business model:

They get paid 10 paisa per stream from the free user on the streaming platform.

Paid customer on streaming platform: 50% of whatever the streaming partner gets on the basis how many Saregama songs are played.

If customer listens to only Saregama songs after paying then all Rs.50 is ours.

They one of the few labels who have maintained 10 paisa per stream.

1 billion streams on YT to now 32 billions stream per quarters (because this stream also includes videos where Saregama’s song is used)

They have hired a team of Data scientist who track every song released in India and do modelling. This team earlier used to work at Tata Sky with Vikram Mehta.

Further only people below age 30 in the company are allowed to judge the songs and no one above that age.

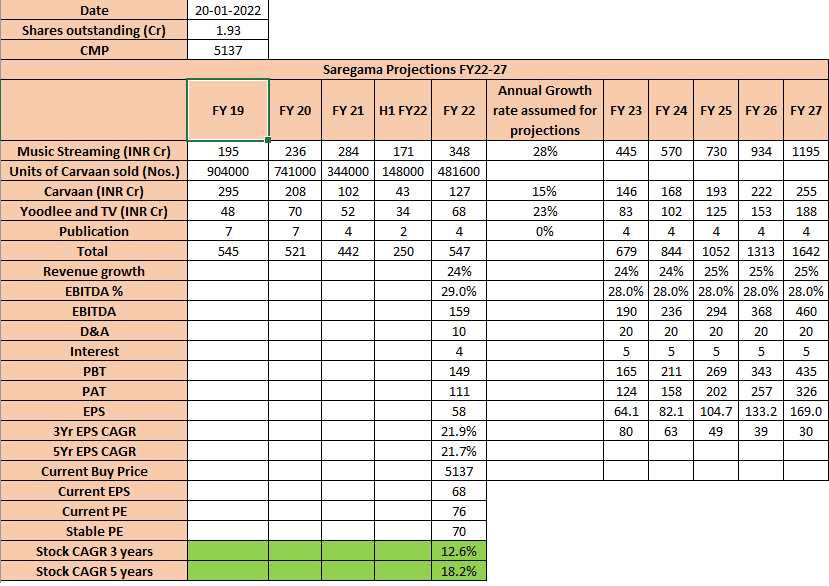

Good con-call by Saregama. Not going into the details of the concall, but projecting Vikram’s given numbers to form a view about fresh investment starting from CMP of INR 5137.

Assumptions: Music streaming revenue growth CAGR - 28% (Vikram guidance 25-30%; This includes QIP war-chest effect but does not include significant growth in music streaming subscription growth) Carvaan revenue growth CAGR - 15% (Although no guidance by Vikram, but this CAGR will take us to annual sales of 6.5 Lakh Carvaans by FY25 end which is 1.6L a quarter. This number can easily be achieved in a Covid free environment without incurring any ad spends; Current quarter no is 148k without any ad spends) Yoodlee growth CAGR - 22.5% (Vikram guidance 20-25%) EBITDA - 28% (Strong guidance by Vikram for OIBICD of 32-33% per annum; Assuming 5% content charge below this to arrive at EBITDA)

With these numbers, my projected FY25 full year EPS is 105. CAGR returns at various exit PEx are as follows:

50x PE - 0% CAGR 60x PE - 7% CAGR 70x PE - 13% CAGR

As you can see, there is very little margin of safety in these valuations. Who can say with confidence that Saregama will command a PEx of 70 at FY25 end? PEx are a function of many external items like liquidity situation for example.

Looking for counter takes please.

PS: @sahil_vi thanks for asking Vikram about the music streaming revenue! He revealed a lot of information. I guess we have to wait for Q1 FY23 results and FY22 AR to find out the extent of spillover of streaming revenue. It seems like Saregama is only recognizing minimum guarantees as revenue in Q1-Q3 and will recognize spillovers post contract period end (Which I am guessing is FY end based on previous lumpiness)