Sanghvi is used to make 350crs of operating profit during good times.i.e FY2016,2017. and cashflow from operating activities was more than 250crs. Now they are not looking for Capex in near future + interest cost have been reduced significantly even during bad cycle from > 60 crs to 30-32crs, so net cash flow will be much more.

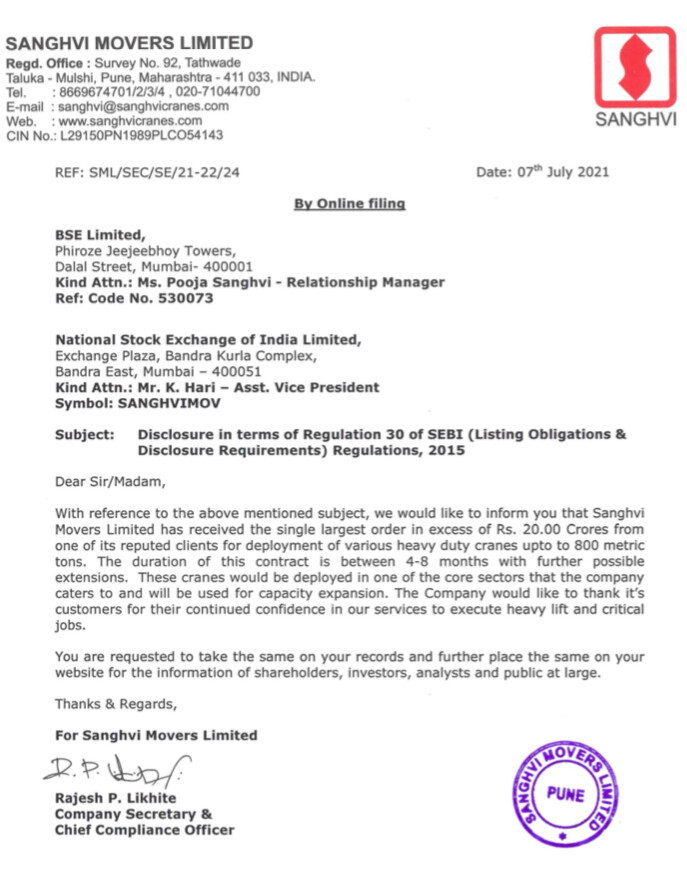

Company Update:

This is to inform you that, Hon’ble Bombay High Court vide its order dated 03rd February

2021 set aside the assessment Order passed by the Deputy Commissioner for F.Y. 2012-

13 demanding VAT and CST on crane rental income and have granted absolute stay in

our favour.

I have written a post on my blog (click HERE) in regards to Sanghvi Movers. While my post is more about the mistake I made by NOT buying this stock when it was trading at Rs 100 as it offered a great margin of safety with an upside of atleast 30% at that price, some of the insights in the blogpost maybe useful to investors:

This stock, even when viewed most pessimistically i.e. from a Cigar Butt perspective (a company which generates positive cashflow but only a limited number of years prior to being liquidated), has a value of around Rs 130/share (and that is why it was a value buy at 100). The detailed calculations are also shared in an excel linked in the above post.

What about buying the stock at the current price

Before that, one should understand the revenue growth of the company. Crane rental business quite obviously is dependent on the infrastructure investment cycle. The company showed spectacular growth from FY06 until FY12 by tripling its revenues. As the investment cycle started slowing down from FY12 onwards, the revenues started to fall. The company ended the decade at a revenue of Rs 323 crores in FY20 – almost the same amount as it was 10 years in FY10. Furthermore, in the entire decade this company could not earn a return above its cost of capital. Consequently, you could make a return on this stock only if you bought it at a substantial discount. There is a post by @premsagar above and it is tremendously insightful in this regard.

IMHO, at the current price the market is asking you to take a view whether they company will increase revenues over the medium and/or whether over the long term it can earn a return above its cost of capital or a combination of these two factors. If your answer to this is in the positive then you can consider buying it.

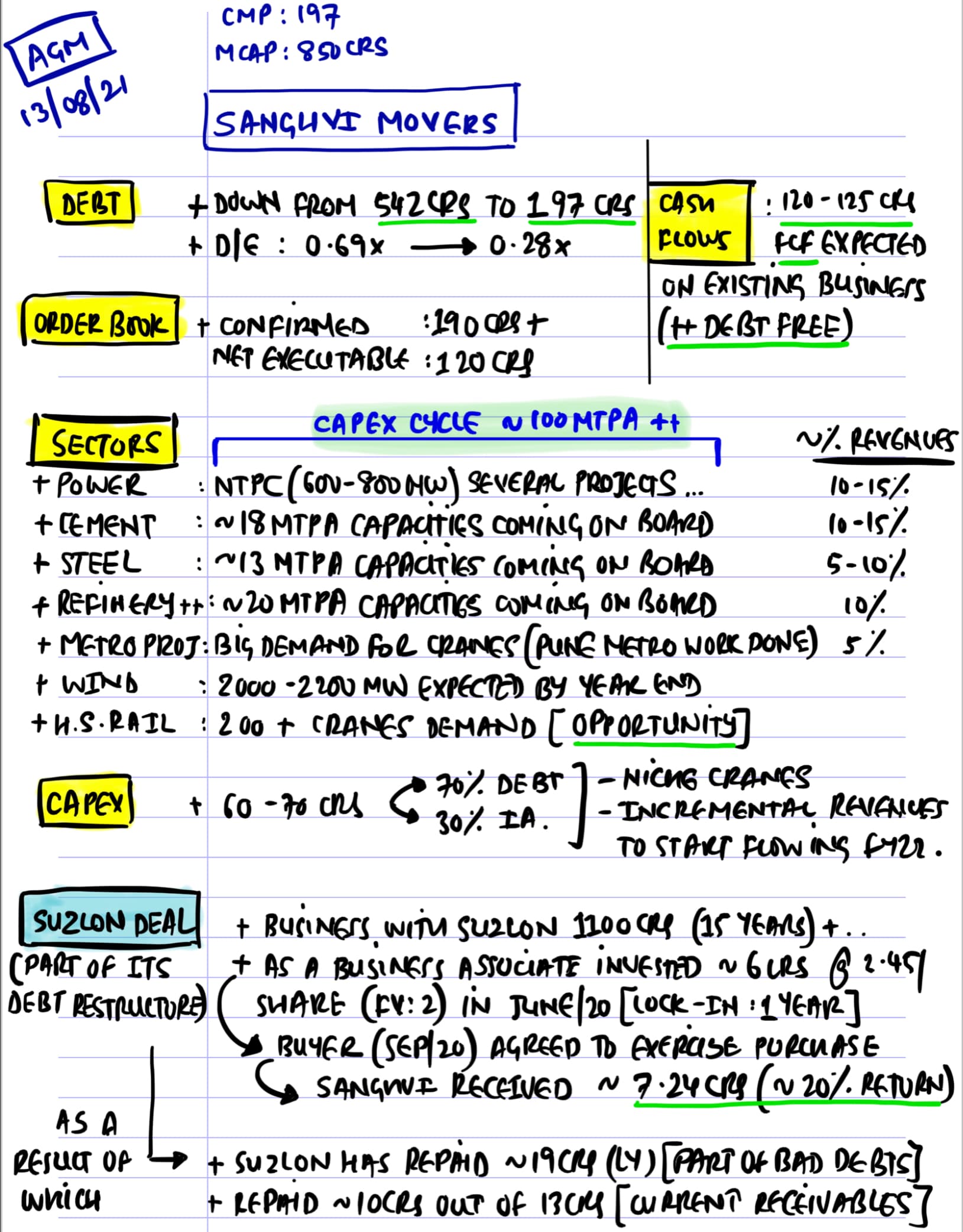

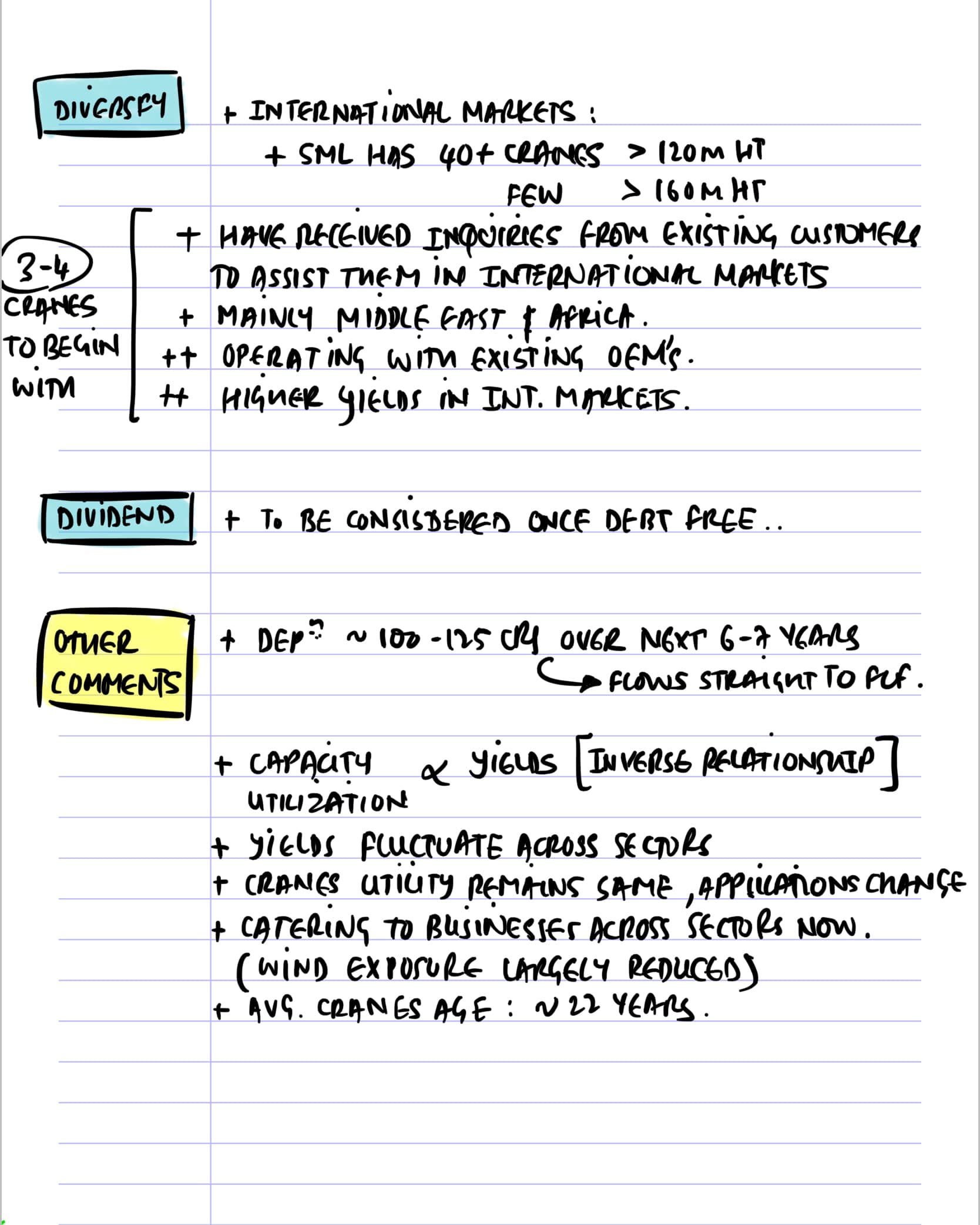

Sanghvi probably should get traction from this project. Recent result presentation shows steps being taken to recover money from Suzlon, Agm mentioned Suzlon being a top client, also Wind sector contribution reducing further from 40% to 36%.

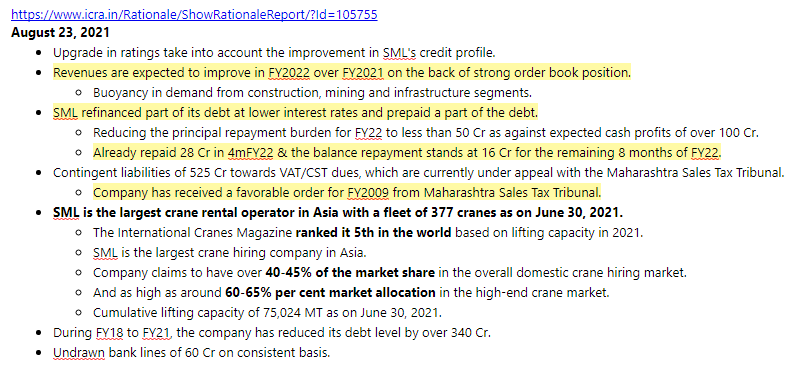

Sharing my notes from Sanghvi’s latest credit rating report.

It is good to see a rating upgrade for the company and continuous debt pre-payment despite going through a difficult phase for last 3+ years. Management showed prudence in using cash profit and monetizing non core assets.

Post 2017, management quickly shifted gears from adding capacity to using the cashflow in reducing the debt and making the balance sheet lean. Which I believe will help them perform better over the next growth phase…as company will have the runway to add assets if needed.

Overall, management sounded optimistic for coming years at this year’s AGM. @rcinvestor999 has captured the discussion beautifully and highlighted the key points. Such notes are very helpful…please keep sharing such good work with the community

As per my view,Business model of SML is not successful in last ten years because of Asset heavy Business model. So,Net Fixed Asset to Turnover ratio is the key factor for valuing SML.

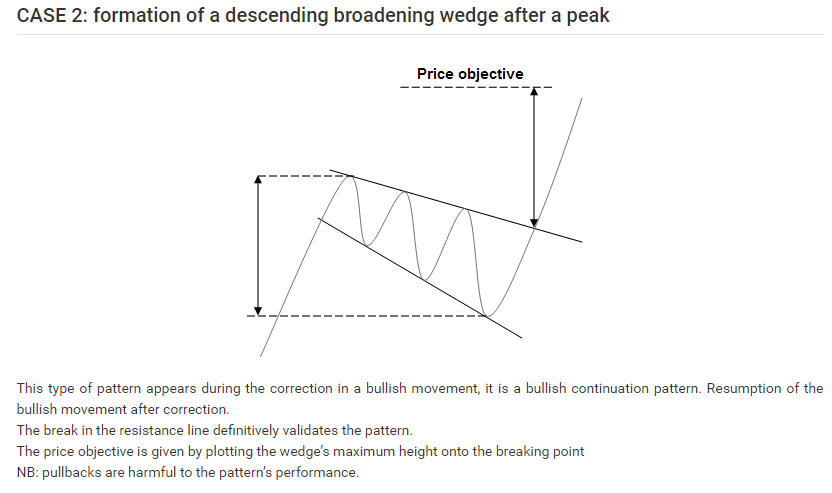

Volumes have picked up last few months. Stock has done well with months of consolidation between upmoves. (yellow blocks). The downward descending broadening wedge pattern has played out well, with the target yet to be achieved.

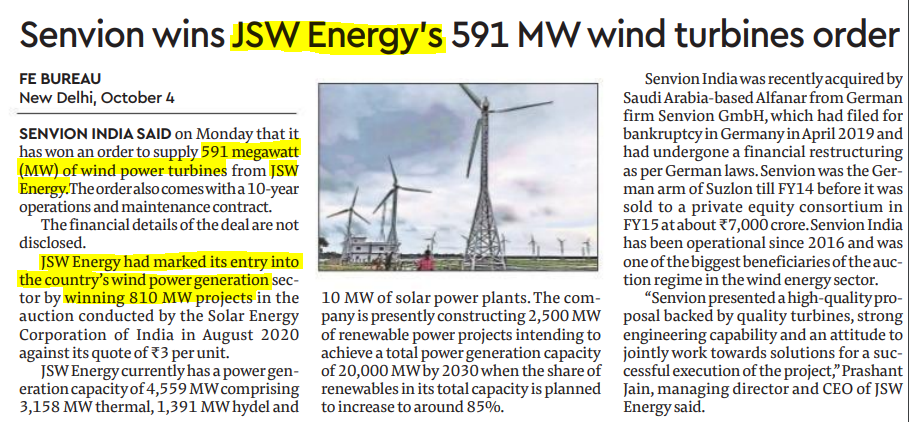

Should clarify that Inox Wind is a former client of Sanghvi Movers. This order doesn’t directly benefit SML. SML has had trouble collecting receivables from Inox Wind in the past and I believe they don’t do business with Inox Wind anymore.