Sorry , 158 room count in NCR was wrong count so deleted that post. Actually in Delhi-NCR they operate 3 hotels (Hyatt Place in Gurugram - Upper Mid scale , 2 Holiday inn Ex 1 each in Noida & Gurugram ) out of total 32 hotels.

3 Likes

“Revenue of 1530 Cr and EBITDA of 630 cr with 41% EBITDA Margin” Is it for FY26 projection?

SAMHI Hotels targets Rs.2,300 crore revenue with strategic growth and asset recycling

Samhi trading at FY26 EV/EBIDTA ratio of 13, Market cap to Sales 4, Forward PE 25. Within two years it wil transform into upper upscale premium Hotel Owner. Safety of margin is very high.

7 Likes

Fair results. But the stock price is really a test of patience. Been invested into this since last year.

Any opinions about why it fell so sharply this time?

2 Likes

The only reason I can think of is high expectations. Samhi was doing north of 15% revpar growth consecutively since last 8 quarters, and finally you end up at 10% (yeah there were reasons for May quarter due to the geopolitics but April and June were still only 12-13%), so I think people are just worried about slowdown overall

3 Likes

Overall performance across the hotel industry is very positive. One only needs to look at the Indian hotel company to see this for themselves. Its quite a wonder why Samhi dropped so much today considering they have done things like they said they would; De leverage balance sheet below 3.5 net debt to ebidta, recycle assets and improve hotel performance. I believe its only a matter of time before earnings violently catch up to valuations. Or maybe the market knows something we dont

10 Likes

I was trying to calculate the current valuation (EV/EBITDA) of Samhi post the Q1 earning and the sale of Caspia:

Mcap = 4513cr

Net Debt = 1369cr (reduced due to asset sale)

EV = 5882cr

EBITDA (TTM) - 442cr

EV/EBITDA = 13.30 as of 14th Aug 2025

Expected EBITDA for fy2026 = 489cr (as per PL Capital, linked below)

EV/EBITDA = 5882/489 = 12

so,

EV/EBITDA = 13.30 as of 14th Aug 2025

EV/EBITDA (fy2026) = 12

Could somebody cross check? Looks quite undervalued when compared with the peers who are at-least trading at EV/EBITDA of 20.

7 Likes

Also they are able to sell their assets on avg of 20 EV/EBITA

1 Like

In FY 26 Q1 PPT, page 24 : they mentioned “even assuming no growth in RevPAR from FY 25 level, still they will easily do EBITDA of 630 Cr”. If we take 10% increase in RevPAR ( very much possible ) EBITDA comes Appx 700 Cr. I see good valuation gap , but not sure when Mr market will see gap in valuation and reward accordingly.

Also I think they have some cash in their book that we need to minus while calculating EV.

Dis : Invested and fully biased

6 Likes

This year belongs to Samhi rerating, friday reaction is to snatch stocks from weak hearted retailers. One of best bet to make up to 100% in a years time, have started increasing my holdings. Fair valuation is close to 12000 cr in three year timeframe. Great example of fear and greed. Have seen same thing when Force motors was dragged from 10000 to 6000 despite posting great numbers, once PMS acquired enough quantities it more than tripled from 6000 to 20000. Current valuations are no brainer as interest cost reduced from 234 cr to 137 cr, even with 12-15% growth and huge tax assets, EPS of 8 should come.

25 Likes

Hello members!

One question is bugging me. As per mgmt. they have sold non-performing assets at avg 20x EV/EBITDA, while in the recent GIC deal, they have sold their best performing assets at roughly 17x EV/EBITDA. Why such a divergence? Is there something, i am missing?

Any community member have any insight, will be helpful. Thank You.

Disc: Have tracking position.

6 Likes

There is a difference between selling a single asset for capital recycling and getting a strategic investor of GIC stature. At the time when GIC invested in SAMHI’s assets some of them (please cross check) had debt and overall SAMHI had some 1967cr of net debt. So, you get the valuation as per the quality of your balance sheet. The deal has to be sweet for both the parties, hence, the 17x EV/EBITDA.

Also, one shouldn’t evaluate this investment in isolation, please also consider the 2nd level advantages to SAMHI:

- Absolute debt decreased by 27% and the interest cost by 26%. This will directly flow to PAT.

- 35% of any new investment in upper upscale assets would be funded by GIC. Given these assets are extremely expensive, this is a huge catalyst for growth.

- Improved balance sheet quality and reputation of GIC lead to credit rating upgrade and consequently decrease in credit cost.

- Such PE players bring pristine corporate governance standards and SAMHI will also be benefited by that. As SAMHI do not have any single promoter such an investment at least giving me a huge comfort.

9 Likes

Hi. Thanks…

What i understand from the deal structure is;

- Out of 752 Cr, 488Cr is being used to repay debt in two subsidiary where GIC is JV. So from debt perspective this favours GIC more. I am assuming that, ASCENT & SAMHI JV is now debt free.

- GIC JV deal has already set aside 149 Cr for expansion in Inmar, which will be infused subsequently. Any more funding will be done either by debt or more equity.

- Only 115 Cr has come to the Samhi Hotels in the deal.

- Samhi has a long history of association with PE firm. And their business model is around getting international brands to run the hotels. I am not sure how much GIC association will actually be value accretive for Samhi.

4 Likes

Not sure if ASCENT & SAMHI JV is now debt free. Most probably JV is debt free, need to check this in detail.

I guess 149cr is GIC’s part and the rest SAMHI will contribute from its cash flow. Debt is not required as SAMHI has very good OCF after all the deleveraging drive.

Also, SAMHI got 227cr that they gave as a debt to Ascent. Ultimately, SAMHI used it (along with the 115cr) to repay its own bank debt. So, they didn’t earn any cash equivalent from this capital infusion if that is what you are looking for. It was predominantly an investment to strengthen the balance sheet and not to earn a direct cash flow.

GIC’s balance sheet would be available as part of the JV for the next leg of growth in upper upscale assets. This is what at-least I am banking on. SAMHI needs a partner who can support them financially else they end up taking loans as the upper upscale assets are very capital intensive propositions. At the same time highly value accretive.

6 Likes

While the recent events are all but optimistic, stock has fallen 25% in three weeks ; more so after q1 results. What is the market discounting, or is it attributable to general market volatility?

1 Like

Maybe, Govt. of Singapore is divesting now.. after GIC they might not need to hold additional equity and can divest slowly from the 8% they own.

3 Likes

SAMHI has been loss making for many years, hence has very high accumulated losses. This differed tax assets aka accumulated losses need to be first squared off against the future earnings before they actually start paying taxes.

In one of the earning calls(check the attached link and screenshot) i learned that they have some 600cr worth of differed tax assets and won’t be paying any taxes for the next 6-8 years.

So most of their PBT will directly flow into EPS for the next 6-8years, i,e until 2031-2033

Page 15

Could someone please cross check and validate my understanding? If this is the case than the cash flow from operation would be very significant.

22 Likes

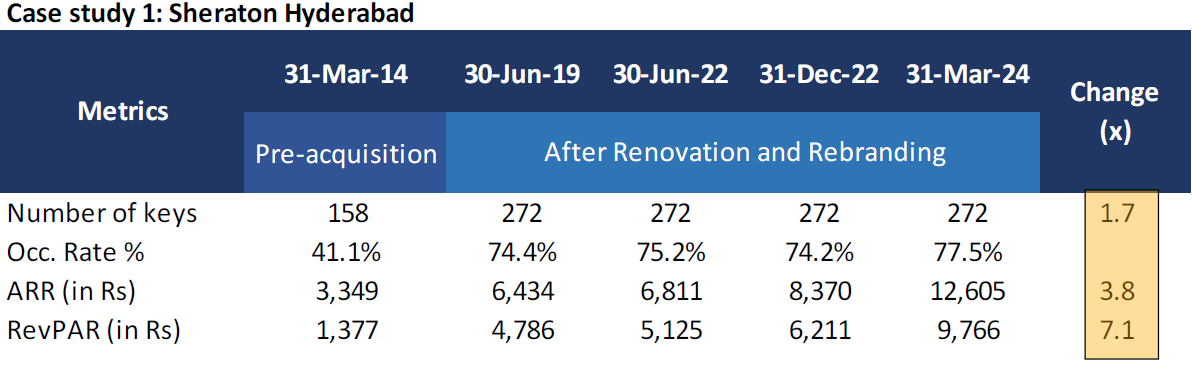

SAMHI bought Sheraton hyderabad at INR 170 Cr march 2014 with 158 keys . Now, even if we take the current numbers of 272 keys, 77.5% occupancy rate, 12600 ARR, and 365 days, the annual revenue for FY24 from this comes to only INR 97 Cr.

I am taking 365 days occupancy of 75%, and INR 12600 as ARR. How long is it sustainable? I do not know. I also do not know the amount of capital invested in renovation and rebranding the properties over the years.

Based on above data..I got the above data from different forum…is this business is sustainable?

The whole idea of IPO is to clear debt…now debt increased more than IPO time…

Where its struggling? to generate cash

Based on above assumption…they have to keep looking for debt or equity dilution to run the show? with recent GIC capital infusion…may be thats what Mr market understood…not giving multiple

I may be wrong in my understanding…just enlighten me

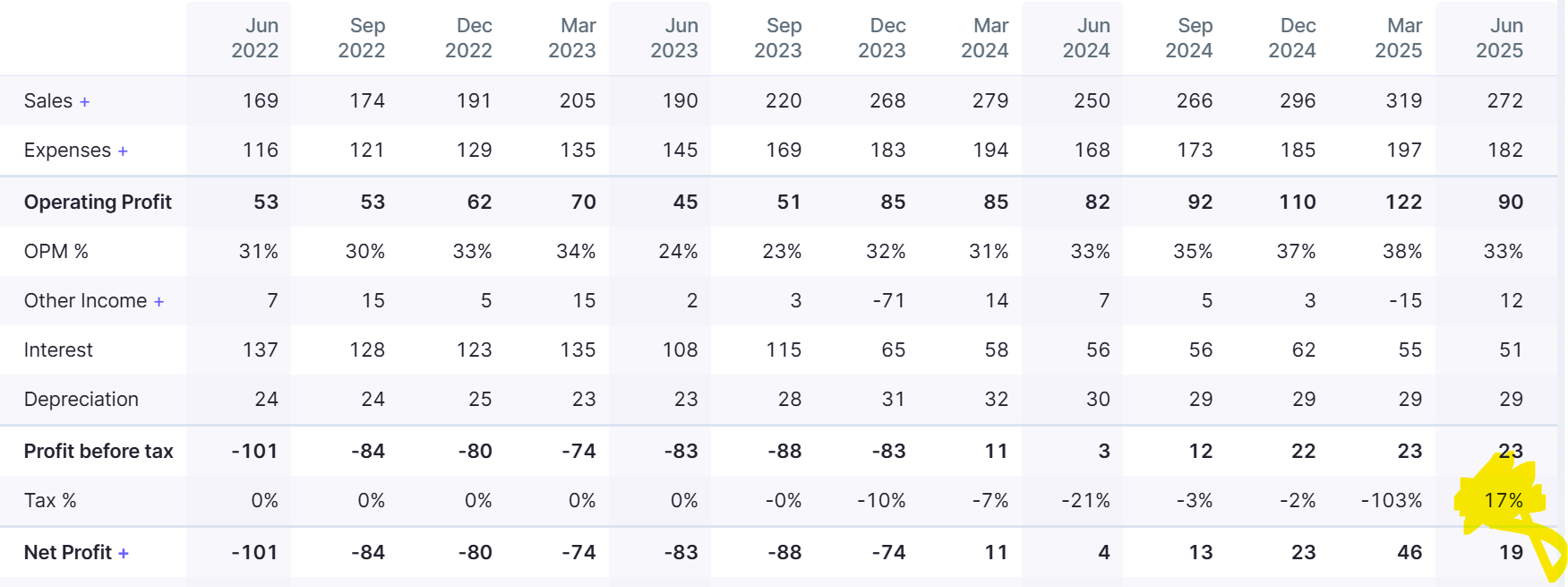

If it is zero tax based on deferred tax…why June 2025 showing 17% tax…Not sure…Please see the screen shot for the same.

7 Likes

97 crore revenue from a 170 crore property purchased in 2014 is stupendous return that too a company which has 35% operating margins.

6 Likes