I assume this was known to folks following REC. Does it portend poorer efficiency?

Could you pls explain how this is indicative of poorer efficiencies in the future? I was under the impression that being granted ‘Maharatna’ status is a good thing as the pre-requisite to get there is to be a high performing Navaratna for 3 or more years.

Typically, when you get maharatna status, it’s similar to “too big to fail” equivalent. You intra gov to gov file approvals and access to PSU bank funds etc is a bit easier. Along with the expectation that you’d pay higher dividend back to the GoI.

It’s all supposed to be positive.

4 Likes

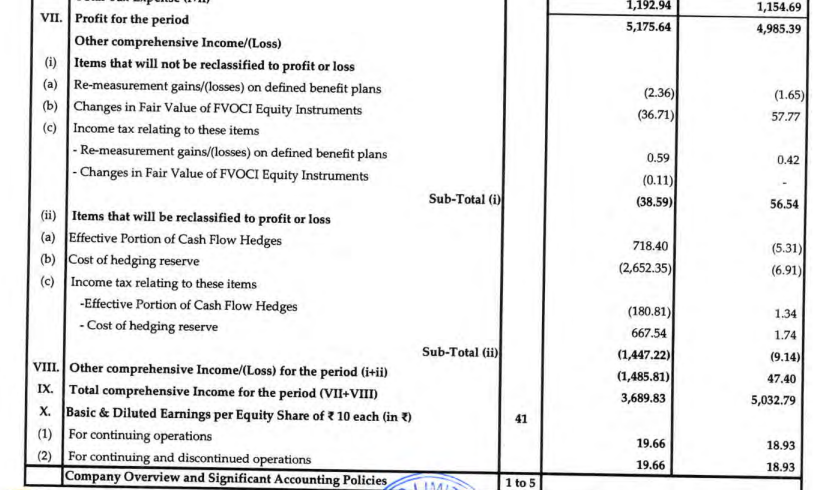

Can anyone explain what are the items mentioned at VII (ii) a,b and c…How come H1 fy 22 EPS is 18.93 when profit was 5032 crore and this H1 EPS 19.66 for a profit of 3689 crore (whereas bonus shaeres also have been issued this quarter)??

1 Like

Cost of hedging reserves is not included in EPS.

Why bonus shares arent considered I have no idea.

1 Like

With a interim dividend of Rs 5, one is already up at FD levels when CMP is 99Rs. This is again one of those PSUs which gives good dividend due to energy needs of a growing country with its loans mode of working.

1 Like

will REC give similar dividend in future after 1:3 bonus shares in august,… like in 2022 it gave dividend of 15.8 Rs and 2021 11.21 rs… and dividend yield become like 16, but with additional bonus shares i guess dividend also will get decreased as the number of shares increased… so is it good for fresh investment … any idea anyone…

REC currently is only paying 25% of its profits (and cash flow) as dividends. Check the various retention and dividend payout ratios. There is a large capacity to retain or increase dividends. I haven’t seen an explicit dividend payout policy. Future dividends will all depend on how much the government wants money in its coffers.

2 Likes

Current norms prescribe PSUs to pay a minimum annual dividend of 30 per cent of profit after tax or 5 per cent of net worth, whichever is higher.

Source: Govt asks CPSEs for quarterly dividend payouts, higher share of profits | Business Standard News

3 Likes

Yes, they do. Infact, the whole NPA mess that got created in these companies was because of this.

However, I don’t see any problem now as the earlier loans that turned NPA were given at the time of euphoria when everyone and their uncle wanted to build power plants without PPAs in place.

Disclosure: Invested

5 Likes

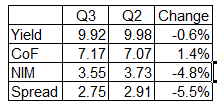

Not a great Q3 though. All below parameter shown some dip

300 provision writeback saved PAT to look like great results. In entire 9m period of FY23, there hasn’t been any new NPA. This Quarter we have 1 upgradation and 1 resolution. So Asset quality wise REC doing great

3 Likes

The provision write back was there but they also had incurred losses of 162cr on hedges. Thus overall pretty solild quarter.

Also per a sell side note loan disbursements had happened towards the end of the quarter which compressed the NIMs a bit - thus should correct to some extent next Q.

3 Likes

Loan book

- Margin compression is real, company expects 3.5% NIM as a sustainable one. REC did not passed enough rate hike to offset raise on CoB. Drop in spread can be marginally offset by increase in equity component, which helps in sustaining NIM(Personally I believe, there will be some more compression, NIM will settle around 3.25% and spread around 2.5%)

- Lending in renewables are highly competitive and has spread of only 2% and Infra will be around 3%

- This 9M REC made a sanction of 1.92 lakh crores of sanction, against a disbursement of 59K crores. This helps REC in growing their AUM by at least 10% yearly

- In this Fiscal FY23 REC anticipates a disbursement of 85-90K crores and 1-1.2 lakh crores in next fiscal FY24

- With 10% rundown in loan book due to repayment and current sanction level, AUM growth of 10% is achievable. With some visibility over AUM growth and investment in PAMC, increase in dividend pay out is highly unlikely

Infra lending

- This quarter REC disbursed 1000 crore in infra projects. In FY23 9M, REC sanctioned around 24k crores of Infra loans. REC has max cap such that infra loans cannot be more than 33% of disbursement per year and also at overall loan book level

- Currently REC looking for only infra loans where there is state govt guaranteed. After time period of 2-3 years where REC will build its expertise in lending to infra and then they will lend to other infra projects on merit basis.

Asset Quality

- In this 9 month period, not even a single account moved to NPA bucket.

- There is a 70% provision on all NPA accounts. This is more than sufficient since all the recent Resolution happened there is some form of write backs happening.

- Adani sanction is 13000 crores and currently disbursed 8000 crores. All the loans are backed by PPA

- Repayment risk from state govt power companies is temporarily offset by the STL support.

PAMC

- Company recently acquired a project which is under resolution where they will be developing/running the power project via a JV, since the competitor quote is way below fair value(Assessed by REC). They will operationalize the project and look for potential suiter in future.

- REC proposes this model to govt and in future we can expect some of the projects acquired via this route

Disc: Invested

11 Likes

Thanks. Great summary and very helpful.

A small edit/clarification on Adani exposure: Total disbursements have been 8,200crs of which they have received back 1,200crs. Thus the current exposure stands at 7,000 crs.

1 Like

Looks like REC has already broken out of a 5 year range. Expecting this to move towards 150 during this counter. Even at 150 this will remain a high dividend yield, deep value stock.

Disclaimer: Holding from last many years. Views are biased.

AJ

1 Like

This quarter also there is a reduction in loan yield. I expected NIM to reach 3.25 in Q1 FY24 and will settle there, but in Q4 itself it reached 3.29.

There is no new asset quality issues in private book, two very small account resolved this quarter, but public sector book is facing lot of heat(Evident from the increase in STL / RBPF book). Sanctions in infra are very high, once disbursed this will be growth driver in AUM.

If we normalize the provision writeback in the reported profit, due to the NIM compression, this quarter is pretty average quarter.

Disc: Invested

1 Like

Results… (please verify for yourself before acting on the below):

| Results | 31-Mar-23 | 31-Dec-22 | 31-Mar-22 |

|---|---|---|---|

| Revenue | 10,123.00 | 9,711.00 | 9,601.00 |

| Other Income | |||

| PBT | 3,811.00 | 3,558.00 | 2,833.00 |

| PAT | 3,000.00 | 2,878.00 | 2,287.00 |

| EPS | 11.27 | 10.93 | 8.56 |

| Growth | QonQ | YonY | |

| Revenue | 4% | 5% | |

| Other Income | |||

| PBT | 7% | 35% | |

| PAT | 4% | 31% | |

| EPS | 3% | 32% |

and YoY

| Results | 31-Mar-23 | 31-Mar-22 |

|---|---|---|

| Revenue | 39,252.00 | 39,230.00 |

| Other Income | ||

| PBT | 13,738.00 | 12,424.00 |

| PAT | 11,054.00 | 10,045.00 |

| EPS | 41.86 | 38.02 |

| Results | 31-Mar-23 | 31-Mar-22 |

| Revenue | 0% | |

| Other Income | ||

| PBT | 11% | |

| PAT | 10% | |

| EPS | 10% |

I see margin has improved, but market doesn’t seem not agree. Insights welcome…

Results link:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/748dc2f7-7fe4-417d-8139-b698723d046e.pdf

What do you mean by margins improved, can you elaborate?

My opms calculate as below:

| Date | 31-03-2023 | 31-12-2022 | 31-03-2022 |

|---|---|---|---|

| OPM | 38% | 37% | 30% |

YoY

| Date | 31-Mar-23 | 31-Mar-22 |

|---|---|---|

| OPM | 35% | 32% |

What you are referring as OPM is PBT/Revenue, this is a wrong metric to track finance companies. You have to look for yield, cof, spread, NIM, Creditcost, RoE, RoA

1 Like