Rupa is relatively undervalued when compared to peers lux and market leader page

once per capita increases, high margin luxury brands like fcuk and fruit of loom will see

increased sales adding to bottom line.

Sunil picking is a endorsement for this stock. should be on investors radar

4 Likes

**

**

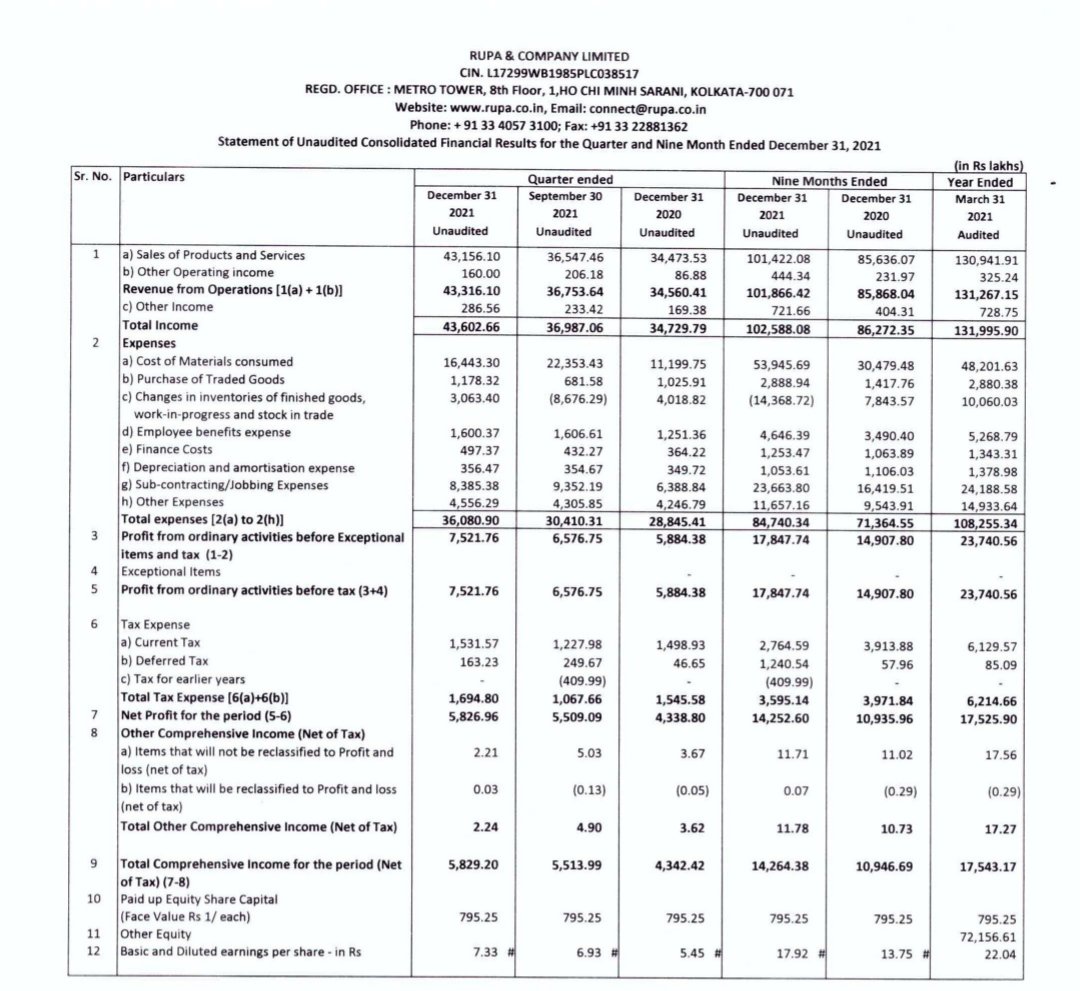

Yet another Strong Quarter

Record Q3 in terms of rev, EBITDA n PAT

Rev at 436cr vs 347cr

PBT at 75cr vs 58.8cr

Q2 PBT at 65.7cr

PAT 58.3cr vs 43.3cr

Q3 EPS 7.33rs vs 5.45rs

9m EPS at 18rs vs 13.8

2 Likes

thanks for your inputs Karthik, can you please help me with these two questions -

- When does the 10 year licensing period ends, is it 2026 or 28? Will it get extended?

- Debt almost doubled in H1 FY22, any updates on the same?

Thanks!

Sarav

Hi Sarav,

Ends in 2026. Extension - too early to comment I think. 10 years is a long period. Might depend on how much these brands contribute to profitability in coming years. They have big plans and have guided for 20% CAGR for this segment in next 3-5 years… Execution needs to be tracked.

Its mostly short term debt. So likely to be used in EBO expansion, etc. They had 11 at start of the year; at 17 now and planning to expand to 35 by year end. Debt to equity is at 0.43 (fairly comfortable considering the cash flows)

4 Likes

The OPM of the company has increased from the September 2020 quarter. It has increased from around 13% to 20%. Hence the net profits have become 3X from that quarter onwards compared to the previous quarters.

Does any one know the reason for the same?. Is this is due to any fundamental shift in business?

1 Like

When will the demerger going to take place? Any idea?

Rupa & Co. looks be ready for next leg of rally after months and years of consolidations. Even after showing tremendous growth in the past quarters the share price was in pressure due to continuous selling by one of the largest shareholders (Ziyan…) part of which is well absorbed by one of the most respected PMS (Sunil Singhania). With that out of the way the Business prospects and triggers are all lined up for good times ahead.

- Trades at the forward multiple of < 15 times whereas all competitors are well above 20 times.

- Management is focused on making the most of the under penetrated areas and Exports. Strong Corp Governance. Guidance of 18-20 % growth (peg <1).

- Tailwinds - Opening up theme, Travel & Tourism is booming, very good wedding seasons expected going forward, Increase in earnings and employments of youth and Women from Tier1, Tier2 cities.

Technical charts also suggest multi year breakout finally possible as most of the stuck supply looks to be at the verge of depletion.

9 Likes

Agree with most of your points.

BTW who are the people behind Ziyan who sold to Abakkus a big chunk of their holding in Rupa nearly 8% which they had been holding for years. Indirect promoter related entity or what?

How critical has been the role played by the New CEO Mr Dinesh Lodha a CA ex GE & Samsung who came 3 years back & seemed to have been a catalyst behind the improved performance of Rupa & co?

Also award of coveted Padmashri specially in today govt to group Chairman PR Agarwala seems a positive sign on ethics front & gives comfort on promoter quality.

This along with presence in good sector with good opp size low valns good ROCE ,brand, distribution reach , non cyclical nature of products augurs well for investment IMHO

11 Likes

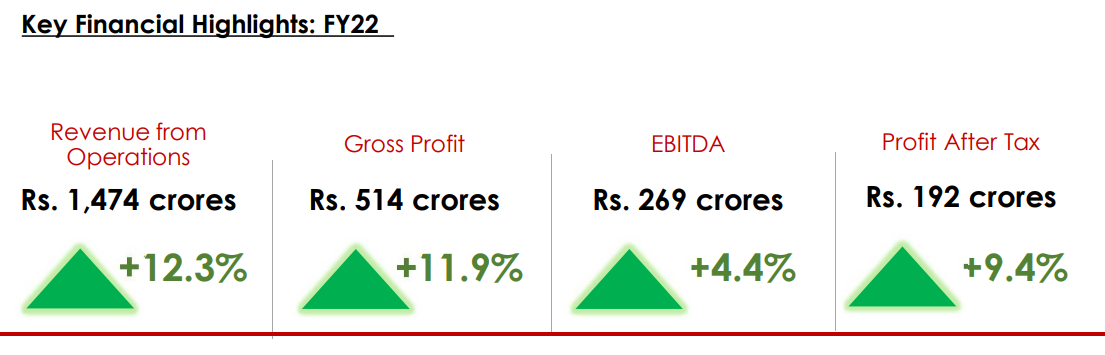

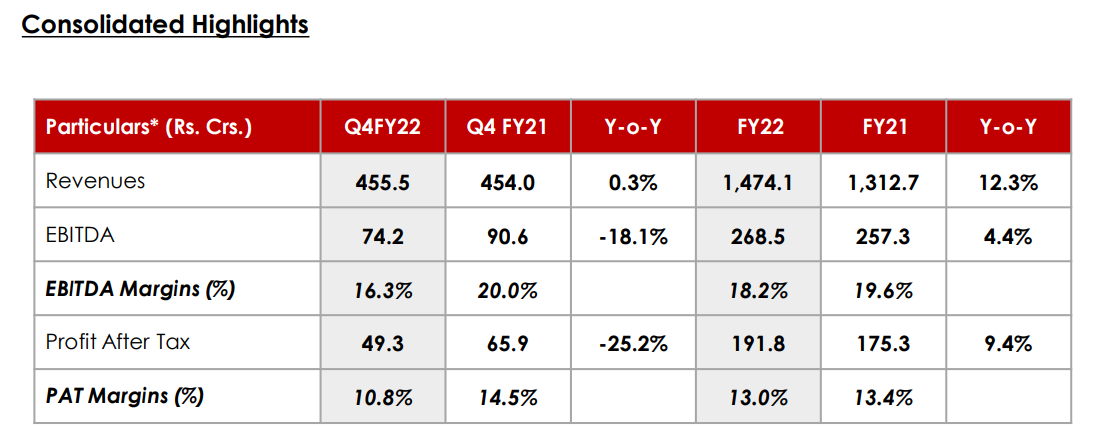

Rupa Q4FY22 Results Press release

Higher RM cost and Omicron has dented the performance in Q4.

Registers highest ever Revenue & PAT in company’s history.

Commenting on the Results, Mr. Dinesh Kumar Lodha, CEO said,

Recorded highest ever full year revenue & PAT in the company’s history.

Hence on an increasingly higher base from FY21, in FY22 we have registered encouraging growth in key parameters Revenues, EBITDA and PAT at 12.3%, 4.4% and 9.4% respectively.

The growth can be attributed to our efforts in scaling up high margin businesses and

strengthening our retail footprint nationwide.

In Q4 FY22, the industry faced headwinds in the form of a COVID wave early in the

quarter coupled with rising raw materials prices. In accordance with our brand scaling strategy, in this quarter we incurred higher advertising & promotion expenses. Thus, a multitude of factors led to pressure on margins. We are also taking steps to calibrate pricing as we balance growth and demand.

Our focus on key growth areas has shown good traction in this year and set the platform for a robust growth in the upcoming Financial Year 2022-2023.

cde4472a-3518-4a50-bec5-bcca44c9f0b4.pdf (bseindia.com)

Dividend Declared: Rs 3 per share.

Results

5234FAF9-36E0-4409-99E2-1D9669EAF246-194027.pdf (bseindia.com)

Investor Presentation: Good read

c89fddf3-c4e8-4242-a2f8-4052a0f4c3ac.pdf (bseindia.com)

2 Likes

Clarification by the company on CEO and CFO resignation:

2 Likes

is the demerger of oban fashions is still under process?

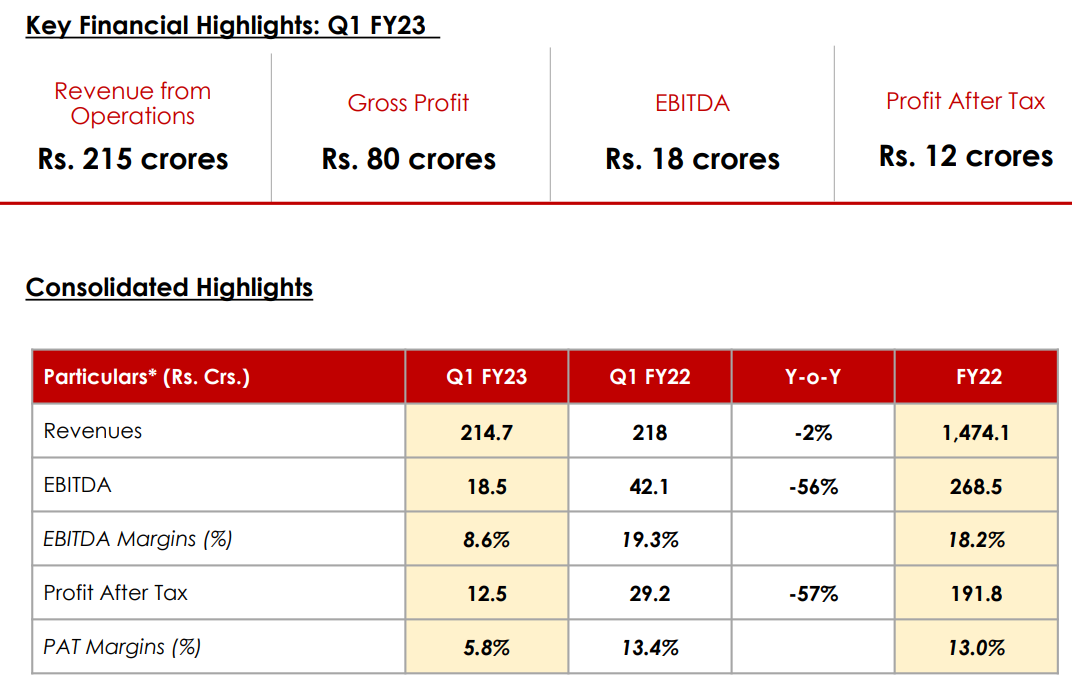

Q1FY23 results: Tepid .

Commenting on the Results, Mr. Vikash Agarwal, Director said,

“After delivering high growth for two consecutive years and registering highest

Revenue & PAT in preceding year, our growth this quarter has been flat.

We took a calibrated price hike to bring our prices in-line with rising raw material costs, this

enabled us to sustain our gross margins.

In the first quarter devoid of any Covid related disruptions, our costs were back to pre-Covid levels. We have also invested heavily in marketing by engaging celebrity brand ambassadors and running national campaigns.

The total advertising expenditure this quarter is ~10% of the revenue visà-vis ~4% in the corresponding period. Elevated fixed costs have had a pressure on our margins on account of being not absorbed completely this quarter.

These strategic expenses, however, will be beneficial for us as we have an operational leverage in future. Further, increased administrative and manpower expenses have also not been absorbed completely due to flat revenue in the quarter.

We are happy to announce the launch of our maiden flagship store in Kolkata along with 2 EBO. Online & e-commerce are focus areas for us and we have generated ~7% of the total revenue via modern trade business. We are also seeing good traction in

the exports business which has doubled year-on-year, contributing ~6% to the total

revenue. We are focused on our long-term goal of providing the highest level of

consumer satisfaction with our bouquet of products. We have stepped up our efforts

in branding to create a formidable brand equity. We are determined to deliver strong

operational and financial performance going ahead. ”

6 Likes

I went to watch the movie - “Laal Singh Chaddha”…Company has promoted its brand massively. For a while, I was feeling as if the movie is made to promote Rupa Corporation than anything else. I am not sure on effectiveness of brand promotion via such channel.

2 Likes

more so when LSC bombed on box office. ![]() …its a big risk associating one’s brand with any film

…its a big risk associating one’s brand with any film

2 Likes

Couldn’t find the concall on any site. Can you please help

Rupa Q1 FY23 results Concall Audio recording

2 Likes

Hi, was tracking Rupa through sideways. Post

recent decent correction, valuation appears undemanding at ~15x forward PE and 1.8 x PB with decent RoE profile (25%). Rerating will depend on EPS trajectory which so far has languished, however good margin of safety at current valuations. With softening cotton prices, margins should see an uptick driving EPS growth.

Any activity from Abakkus on it’s holding (4% stake)?

Anyone tracking the stock? No recent activity in VP forum on this stock.

Recently got interested in the stock and looked at Lux Ind and RUPA. It’s true that both have corrected significantlu from the highs and trading closer to historical low valuations. But, looking at absolute valuation, the PE is still in lower double digits even if we assume the margins would revert back to normal.

And there was no growth for RUPA. Lux seems better placed considering its growth (although partly inorganic growth).

I feel that both offer good valuation comfort. But, the considering the overall market condition, better opportunities are available elsewhere.

My key point. Valuation cheap, better opportunities exist

1 Like

Hi Praveen,

Rupa is the best opportunity I found in the market today as there is revenue and margin visibility. Care to share about the better opportunities?

Thanks

Xpro India, Kernex micro systems, where Promoter and non Promoter have subscribed to warrants above CMP. Visibility of growth.

Pitti engineering, Capex gradually coming online and getting utilized as it comes live.

Ujjivan SFB where post merger P/B would be 0.7-0.8x

Most companies are cheaper now, point is to select the ones with best risk adjusted reward.

Disc: Holding these

2 Likes