Disclaimer: This report is the work of an investment adviser affiliated with the author. The report is the result of the adviser executing its investment strategy. The adviser holds a position in the security, however there is no assurance that the adviser will continue to hold the investment, or make additional investments and will not update the information to reflect future changes in the adviser’s assessment of the investment.

CESC Ventures (CESCV IN)

Non-fundamental selling and challenging market conditions create an opportunity for value minded long term investors

CESC Ventures was spun out of CESC Ltd earlier this year and has sold off since listing due to forced selling by mutual funds constrained by SEBI regulation on large/mid/small cap categorization in a tough overall period for small cap investors.

At least 18% of the company or 36% of the non-promoter shareholding was sold in the open market after the spinoff by large price insensitive mutual funds like HDFC Mutual Fund (18%), ICICI Mutual Fund (6.2%) and others. Actual spin-off related selling is probably higher given that ~75% of the named (largest) pre-spin shareholders exited.

Large discount to Net Asset Value

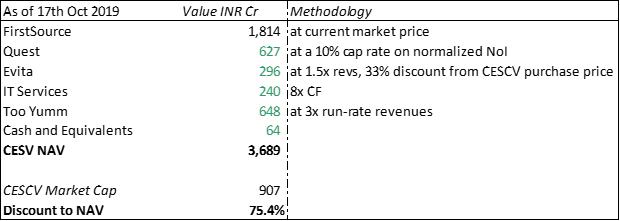

CESC Ventures trades at a 76% discount to fair “net asset value” on a SOTP Basis.

On a look through basis, CESC Ventures trades at a 20% FCF yield ex-FMCG if you assume FirstSource (FSOL) pays out ~50% of NI as dividends to CESC Ventures. Median HoldCo discounts in India are around 30% for active controlling stakes (i.e. Holding companies that actively turn over their portfolio by buying/selling assets) and sub-70% for non-controlling stakes. It is very rare to find HoldCos at discounts of 80% and HoldCos with this level of discount typically have corporate governance problems.

With that in mind, based on our work we think that it is unlikely that CESC Ventures’s HoldCo discount will widen further. On the other hand, if the FMCG business succeeds in doubling its revenues, is spun out, and trades at a 6x revenue multiple in line with peers, CESC Ventures could offer 10x upside from current levels over the next 5 years.

FMCG business - source of non-linear upside

The FMCG business, TooYumm, is headed by ex-McKinsey partner Suhail Sameer and the group plans to separately list the FMCG business once it reaches scale. CESC Ventures plans on using the cashflow generated from its mall in Kolkata and dividends from FirstSource to fund growth for TooYumm, which has grown to over 200cr in annual sales since its founding in 2017.

BPO business and Real Estate – underappreciated, steady cash-generative assets protecting downside

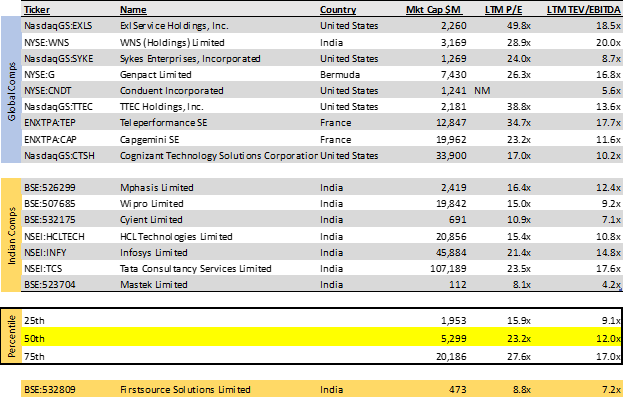

Since FSOL is publicly traded we won’t analyze it in detail, but we believe that FSOL could be an underappreciated source of upside and expect EBITDA to grow at a low double-digit pace over the next few years.

FSOL’s high dividend payout should provide a solid floor on the stock, while its modest valuation of ~9x trailing EPS is a large discount to comparable BPOs and leaves room for multiple expansion from currently depressed levels. Over the longer term, we’d expect FSOL to benefit from the increasing consolidation in the sector.

Quest is the premier mall in east India and has an 8% FCF yield which should grow at 4-5% a year. While Quest is operating at full occupancy (~99%), there is upside from re-pricing of the preliminary contracts signed by tenants when the mall was created. This should cause rents to increase 20-30% over the next few years as leases expire

We believe Sanjiv Goenka is a better capital allocator than the market thinks

Our conversations with other buyside and sell side participants suggest that Mr. Market has a negative view on Goenka’s capital allocation. While CESC’s shareholder returns over the long term have been in-line with indices, CESC has meaningfully outperformed power peers over the last 10 years

While power peers extrapolated the boom seen in power from 2003 to 2007 and engaged in leverage fueled capex to build out power plants, Goenka remained conservative while bidding for new projects. CESC continued to operate at 2-3x Debt/EBITDA while peer median leverage was ~5-6x Debt/EBITDA and the company’s balance sheet was described by analysts as “under-leveraged” and “conservative” at the time. This proved to be a winning strategy as CESC Ventures has meaningfully outperformed peers in its sector, including Reliance Power, Rattan Power, Tata Power, Torrent power, NTPC, and others.

CESC’s non-core investments in FirstSource and Quest Properties (Kolkata Mall and BKC assets) have been homeruns with +334% (CAGR of 23.8% incl. dividends reinvested) and +80% returns (not including interim cashflow) to date.

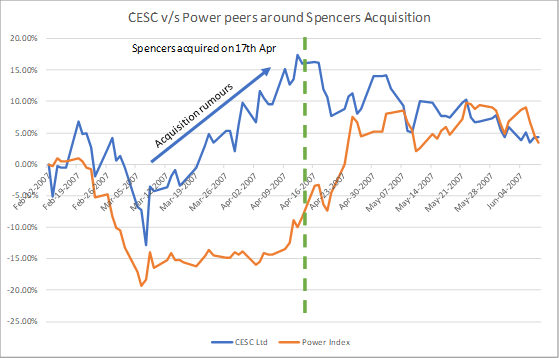

Even Goenka’s poor investments were driven by industry-wide issues rather than poor execution or high entry valuation. While investors criticize Sanjiv Goenka for the Spencers acquisition in hindsight, there was significant excitement around the stock and CESC greatly outperformed its power peers when Spencers was acquired.

The valuation paid for Spencers at 1.7x EV/TTM sales was significantly below Future Retail (3.2x)’s and V2Retail (2.9x)’s trading multiple even though the asset was acquired from Sanjiv Goenka himself.

Analysts were bullish on the space and generally applauded CESC’s use of capital into retail.

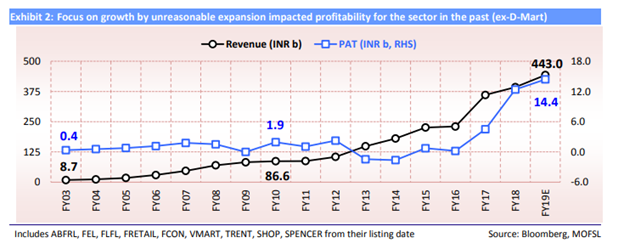

Spencers did not meaningfully underperform organized retail peers from the period. For example, both Vishal Mega Mart and Subhiksha Retail went bankrupt. Industry wide profitability was extremely lack-luster due to massive overinvestments. Profitability in the space has only started coming back as of late:

Note how aggregate industry profits were negative until 2016 due to the aggressive competition by existing retail players despite massive revenue growth

Hard catalyst to reduce holdco discount

We believe that the FMCG business will eventually be spun off and will exit the HoldCo. This will provide a hard catalyst for reduction in the HoldCo discount. Sanjiv Goenka has publicly mentioned plans to separate out the business once it reaches maturity in the past. The spinoff of noncore investments at CESC which created the CESCV entity in the first place provides further evidence that Goenka is willing to separate out group companies to maximize value.

Conclusion

We think CESCV offers a very interesting risk-reward skew for investors who are not constrained by market cap and have the 2 to 3 year time horizon: TooYumm is a very young company with dynamic leadership, and it will suffer missteps and pivot business models along the way, even if it is successful at building a lasting FMCG brand in the end. Either TooYumm does so-so/fails and you get your money back, or TooYumm works and CESC Ventures is a multi-bagger as the NAV discount closes, underlying NAV grows, and the market wakes up to CESC Ventures’s demerger/spin-off plans.

Others may also be seeing value as small/mid-cap stock pickers like Ashish Dhawan (personally and through Ellipsis Partners owns 5% of company) and Arvind Khattar (1.2% stake) have been buying shares of CESC Ventures.

Assigning a fair 30% HoldCo discount to CESC Ventures’s net asset value would result in 2.8x MoM or +180% upside and if the FMCG business succeeds and is spun out, CESC Ventures could offer a 10x return over the next 5 years from current levels.