Rossell Techsys sits at the intersection of aerospace, defense, and advanced electronics—an industry where entry is slow, mistakes are costly, and trust is earned over decades. What began as a manufacturing-led business is now evolving into an engineering and lifecycle solutions provider embedded in global defence platforms.

As Western OEMs diversify supply chains and India emerges as a preferred manufacturing and MRO hub, Rossell’s transformation represents more than scale—it signals a structural repositioning within a high-barrier, long-duration industry.

1-Business Model

-

Rossell is a Global Export Engine. Nearly 99% of their revenue comes from the world’s biggest military and tech giants in the US, Europe, and Israel.

-

They have graduated to become a Tier-1 supplier, meaning they deal directly with the “Big Three” (Boeing, Lockheed, and Honeywell) rather than through middlemen.

The company is currently undergoing a massive “Promotion” in how it makes money:

-

The Old Way (Build-to-Print): They were the expert “builders” following someone else’s blueprints. This provided the volume and the initial trust.

-

The New Way (Build-to-Specification): They are becoming the “Architects.” They are moving away from just assembling parts toward high-level engineering. Instead of just selling their labor, they are now selling their intellectual property. When you own the design, you own the profit.

2-What Rossell Actually Builds (And Why It Matters).

a. EWIS: The “Nervous System”

-

What it is: They design and bundle all the wires that carry power and data throughout a plane.

-

Think of it this way: If an airplane was a human body, this is the nervous system that tells your hand to move or your heart to beat. Without it, the pilot is just sitting in a very expensive metal tube.

b. EPA: The “Control Dashboards”

-

What it is: These are the physical panels and boxes full of switches and screens that you see in a cockpit or a machine’s control room.

-

Think of it this way: This is the dashboard and fuse box of the aircraft. It’s where the pilot actually “talks” to the plane to make things happen.

c. ESSI: The “Smart Boxes”

-

What it is: Instead of just wires, these are the “brains.” They take circuit boards (like the ones inside your phone) and put them into protective metal boxes to do specific jobs.

-

Think of it this way: Think of this as the computer or game console of the system. RTL designs the logic, but they let partner factories do the heavy manufacturing while they handle the “smart” engineering and testing.

d. ATE: The “Super-Testers”

-

What it is: You can’t just fly a jet and “hope” the wires work. You need a way to test them on the ground first.

-

Think of it this way: These are custom-made giant charging stations/diagnostic tools. Before a part goes into a plane, it gets plugged into an ATE rig to make sure it won’t fail mid-air.

3-BTP (Build to Print): and BTS (Build to Specification).

BTP (Build to Print):

- What it is: The customer sends over the exact blueprints and drawings. Rossell’s job is to manufacture the part exactly as shown.

It’s like being a world-class chef following a specific recipe someone else wrote. You didn’t invent the dish, but you’re the only one trusted to cook it perfectly.

- Value addition: This is the “foot in the door.” It’s how Rossell proves to giants like Boeing that they can handle extreme quality standards. It’s also where localisation happens—taking a part that used to be made in the U.S. and building it cheaper and better in India.

Build To Specification

-

What it is: The customer simply says, “I need a box that controls the landing gear and works at -50 degrees.” Rossell then designs, engineers, tests, and builds the solution from scratch.

-

This is being the architect. You aren’t just following a plan; you are creating it.

-

Value addition: This is where the highest profit lies. In BTS, Rossell owns the Intellectual Property (IP). They aren’t just selling their labor; they are selling their “brains.” This makes them a true engineering partner, not just a vendor.

4-Strategic Moats: High Entry Barriers & Customer Lock-In.

a. Getting Approved Takes Years (Certifications & Law)

Before you can even bid on a contract, you need a lot of paperwork that takes years to acquire.

-

Gold Standards: Rossell holds 45 NADCAP audited processes—the highest in Asia. These are the “black belts” of aerospace manufacturing.

-

The ITAR Shield: To handle sensitive U.S. defence data, you must comply with strict ITAR regulations. Rossell’s U.S. subsidiary is already registered and vetted, a process that acts as a legal “wall” against competitors who don’t have a local American presence.

b. The First Part Is the Hardest

When Boeing or Lockheed orders a new part, the supplier must pass a First Article Inspection (FAI).

-

This is a grueling “stress test” of the first unit produced.

-

It is slow, incredibly expensive, and carries a steep learning curve.

-

The Moat: Rossell has already cleared this hurdle for over 250,000 different parts.

c. Experience Matters More Than Machines

You can’t learn how to build a fighter jet’s nervous system from a YouTube video.

-

The Secret Sauce: Rossell relies on “tribal knowledge”—proprietary process engineering secrets for soldering, crimping, and shielding that they’ve perfected over a decade.

-

Certified Hands: Their staff doesn’t just have degrees; they hold specific global soldering and wiring certifications (like IPC 620 and J-STD).

d. Customers Don’t Change Suppliers Easily

In this business, switching suppliers is like trying to change the engine of a plane while it’s in mid-air.

-

The 30-Year Lock-In: Once Rossell’s wiring is “designed into” a platform like the Apache helicopter or the F-16, they are effectively there for the life of that aircraft (often 30+ years).

-

Risk Aversion: In defence, the cost of a single failure is catastrophic. Customers like Boeing prefer the “zero-defect” track record of an incumbent like Rossell over the risk of an unproven newcomer.

-

Strategic Agreements: Rossell has over ₹2,500 crores in long-term strategic agreements.

e. High Capital Heavy business

This isn’t a “lean” startup business.

-

Cash-Heavy: It is working-capital intensive. Rossell holds 5–7 months of inventory to ensure they never miss a delivery for a multi-year defense contract.

-

Global Footprint: Having a facility in Bengaluru is only half the battle. Rossell’s physical presence in Arizona (near their customers) provides the “near-shore” support and repair services that purely offshore competitors simply can’t offer.

5-Rossell US subsidiary.

a. Working locally — Rossell Techsys Inc. (Arizona)

Rossell doesn’t just operate from India; they have a “home team” in Tempe, Arizona. This office does three critical things:

-

Speed: If a US customer needs a repair or a part fixed, Rossell does it in Arizona immediately. No waiting for shipping to India.

-

Trust & Laws: US defence secrets are protected by strict laws (called ITAR). Having a US-based office allows Rossell to handle these “top secret” details that can’t be sent overseas.

-

Relationship: It’s easier to win contracts when you can meet your customers for coffee in their own time zone.

b. Cutting Out the Middleman

In the past, Rossell often sold their parts to another company, who then sold them to the “Big Three” (Boeing, Lockheed Martin, and Honeywell). Now, Rossell is dealing directly with these giants.

- They’ve moved from being a “sub-contractor” to a Direct Tier-1 Partner.

c. Tapping into newer segments (Space & Chips)

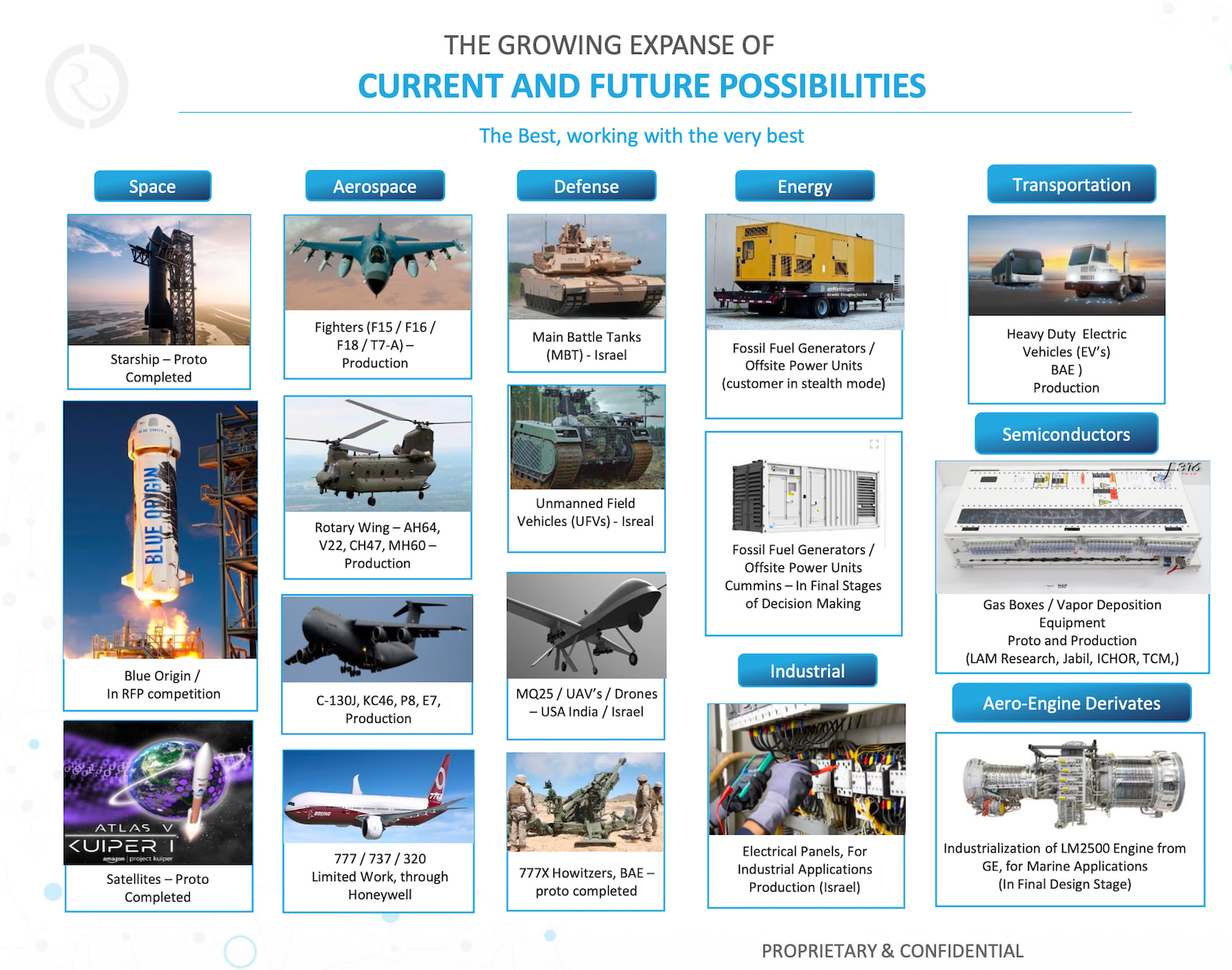

Rossell is using its reputation in fighter jets to win business in two “exploding” markets:

-

Space: They are now building wiring for SpaceX, Blue Origin, and Amazon Kuiper.

-

Microchips: They supply the “nervous systems” for the massive machines made by Lam Research that manufacture computer chips.

-

The Goal: These new sectors are expected to grow from 25% to 40% of their total revenue by next year.

d. Aggressive customer acquisition

For years, Rossell grew through word-of-mouth. Now, they have hired a professional sales team to target the top 100 US companies.

6-US Military Equipments that have Rossell’s components.

a. The Frontline Fighters

Rossell is deeply embedded in the U.S. fighter jet program.

-

F-15, F-18, & T-7A Red Hawk: They provide critical connectivity for these high-speed jets.

-

F-16 Falcon: This is a standout program for Rossell, serving as a massive, long-term revenue driver for the company.

b. The Heavy-Lifters (Helicopters)

If you see a U.S. military helicopter, there is a high probability Rossell is inside.

-

AH-64 Apache: The world’s premier attack helicopter.

-

CH-47 Chinook: The iconic heavy-lift transport.

-

MH-60 & V-22 Osprey: Essential multi-mission aircraft that rely on Rossell’s wiring to operate in extreme conditions.

c. Patrol and Support Aircraft

-

P-8 Poseidon

-

C-130J Super Hercules

-

KC-46 Pegasus & E-7 Wedgetail

d. Next-Gen Tech and Artillery

-

MQ-25 Stingray

-

777X Howitzers

7-Vertical Integration: Moving Up the Value Chain.

a. Backward Integration: The Cost-Cutting Moat

Instead of just buying parts from others, Rossell is taking control of its own supply chain through “localization.”

-

Indian Sourcing: They used to import mechanical components from the U.S. Now, they source them from within India. This simple switch saves their global customers 20% to 30% in costs.

-

In-House Control: By bringing metalwork and electro-optics in-house, they reduce their dependency on outside partners, ensuring they can always deliver on time without waiting for a middleman.

b. Forward Integration: From “Parts” to “Systems”

This is where the real profit lies. Rossell is transitioning from a manufacturer into a high-level engineering firm.

-

The “Black Box” Strategy: Instead of just making the wires that connect computers, Rossell is now building the integrated electronic modules (the “black boxes”) themselves.

-

Building the Muscles: They are expanding into actuators, sensors, and solenoids. In simple terms, if the wires are the nerves, these are the muscles that make the plane move.

-

The Aftermarket (MRO): With their new MRO license (AS9110), Rossell can now maintain and repair parts for the life of the aircraft. This turns a one-time sale into a 30-year revenue stream.

-

Design Ownership: They are shifting from Build-to-Print (building from someone else’s drawing) to Build-to-Specification (designing the solution themselves). When you own the design, you own the profit.

8-Research AND Development focus of the company.

-

Rossell spent nearly 5% of their total turnover on R&D.

-

Expanding Beyond Wiring

-

The “Wiring Analyzer”: Their R&D team has built a home-grown device that automatically tests complex cable bundles. Instead of buying this tool from others, they built it themselves, making their own testing faster and more accurate.

-

Reverse Engineering for MRO: A major focus is “figuring out the past.” They study old, obsolete parts from 30-year-old jets and use reverse engineering to build brand-new, modern replacements.

-

Robots and AI: To handle massive orders for semiconductor and space clients, Rossell is investing in Robotics and AI. They are automating their assembly lines so they can produce thousands of high-quality parts with minimal human error.

-

Atmanirbhar (Self-Reliance): They are focused on “Indigenization”—replacing expensive imported parts with high-quality Indian versions. This supports the government’s mission and slashes costs for their customers.

-

In the last year alone, Rossell poured over ₹12 crores into R&D. While most manufacturing firms spend their money on just buying bigger machines, Rossell is spending its money on brainpower.

9- Semi conductor, Data centre and Marine segment

a. Working with the World’s Chip Manufacturers (Semiconductors)

-

Rossell is a critical “upstream” supplier. They build the high-tech wiring harnesses for the tools used to process silicon wafers.

-

High Volume: Unlike defense (where you build a few parts for a few jets), the chip industry needs thousands of parts fast. To handle this, Rossell is investing in robotics and semi-automated machinery to speed up production.

-

Revenue Explosion: Combined with their Space business, these new sectors are expected to grow from 25% of revenue this year to 40% by next year.

b. Building Data Center Equipments

-

While Rossell doesn’t build the data centers, they build the equipment that keeps them “always-on.”

-

They are in the final stages of a partnership with Cummins, a global leader in power generators.

-

Rossell builds the electrical panels and wiring that make that happen.

c. Marine Segment

- Rossell is currently in the final design stage of industrializing the LM2500 engine for marine applications.

d. Faster Cash, Better Efficiency (Working Capital Benefits)

-

This shift into Chips and Data Centers isn’t just a tech move—it’s a brilliant financial move.

-

Faster Cash: Defense contracts take years to pay off. Semiconductor and Industrial contracts move much faster (6 to 12 months).

-

The “Four-Turn” Goal: By doing more business in these sectors, Rossell can get their cash back faster.

-

This helps them reach their goal of a “3-month inventory cycle,” making the company much leaner and more profitable.

10-What exactly is MRO?

-

Think of it like a car. Buying the car is a one-time expense, but over the next 15 years, you spend a lot more on servicing, oil changes, and replacing worn-out parts.

-

In the aerospace world, a fighter jet or a commercial plane stays in service for 30 to 40 years. Over that lifetime, the plane will be taken apart and put back together dozens of times to ensure it’s safe to fly. MRO (Maintenance, Repair, and Overhaul) is the specialized business of keeping these aging machines in “like-new” condition. It’s a massive global market worth over $50 billion annually.

11-Rossell’s Plan: From Manufacturer to Lifecycle Partner.

Rossell isn’t just content with building a part and walking away. They want to be the ones who fix it for the next three decades. Here is their plan to conquer the MRO space:

a. The “Golden Ticket”: The AS9110 License

-

Rossell has applied for the AS9110 license, which is the specific legal “stamp of approval” required to perform aircraft maintenance.

-

The Shift: This license transforms Rossell from a factory that follows a blueprint into a certified service center.

-

The Readiness: They expect to secure this shortly, which will allow them to immediately serve existing customers like Boeing and Lockheed who are already asking for local repair support in India.

b. Solving the “Extinct Part” Problem

-

Many military jets flying today were built in the 1990s. Often, the original company that made a specific circuit board or wire harness has gone out of business.

-

The Strategy: Rossell is using Reverse Engineering. They take a broken, “extinct” part, figure out how it was designed, and then use their R&D team to build a brand-new, modern version. This keeps old planes flying and makes Rossell indispensable to the military.

c. Doubling the “Wallet Share”

-

Right now, if you look at all the electronic components in a plane, Rossell manufactures about 5–7% of them.

-

The Goal: By entering the MRO space, they aim to jump to 12–15% in the short term, and eventually 30%.

-

Why it works: It’s much easier to sell a repair service to a customer you already have a 10-year relationship with.

-

Better Margins and Domestic Growth

-

Higher Profits: Manufacturing is high-volume, but MRO is high-expertise. Because it requires more specialised skill, the profit margins are typically much healthier.

12-The Tailwinds Government Policy and Regulatory Impact.

-

Largely Insulated from Trade Wars: While many exporters worry about tariffs and sudden policy changes, Rossell is relatively shielded.

-

Duty-free access to the U.S.: Most U.S. defense imports are exempt from standard tariffs. Rossell uses strict tracking systems to ensure shipments qualify for duty-free entry.

-

Tax-free imports in India: As a 100% Export Oriented Unit (EOU), Rossell can import high-tech raw materials from anywhere in the world without paying customs duty or GST.

-

India’s defence policy requires foreign suppliers to reinvest a portion of large defence contracts back into India. This is known as a defence offset.

-

Here’s where Rossell gets an edge.

-

Because Rossell is classified as a “Medium” enterprise, foreign OEMs receive a 1.5x offset credit for every rupee spent with Rossell.

-

In simple terms, one dollar spent with Rossell counts as ₹1.5 worth of compliance for the foreign supplier.

13-Board of Directors and top management.

-

Founder leadership:

-

Harsh Mohan Gupta (Executive Chairman): 50 years of industry experience, providing long-term strategic direction.

-

Rishab Mohan Gupta (Managing Director): Founding member of the aerospace division and a trained pilot, ensuring a strong focus on mission-critical reliability.

-

-

Professional global CEO:

- Senthil Balasubramanian (CEO): 30+ years of global manufacturing leadership, with senior roles at Collins Aerospace, ITT Interconnect Solutions, Ultra Maritime, and Blue Star Limited.

-

Strong independent board:

-

T. Suvarna Raju: Former Chairman of HAL, brings deep aerospace execution experience.

-

Shobhana Joshi: Former Secretary (Defence Finance), Ministry of Defence, adds policy and procurement insight.

-

-

Execution-focused operating team:

-

Zeena Philip (COO): 16 years at GE Healthcare in factory and sourcing leadership roles; earlier experience at Hewlett-Packard and Thermometrics.

-

Jayanth V (CFO): Leads financial discipline and capital management.

-

-

U.S. presence:

- Prabhat Kumar Bhagvandas heads the Arizona subsidiary, supporting U.S. defence customers locally.

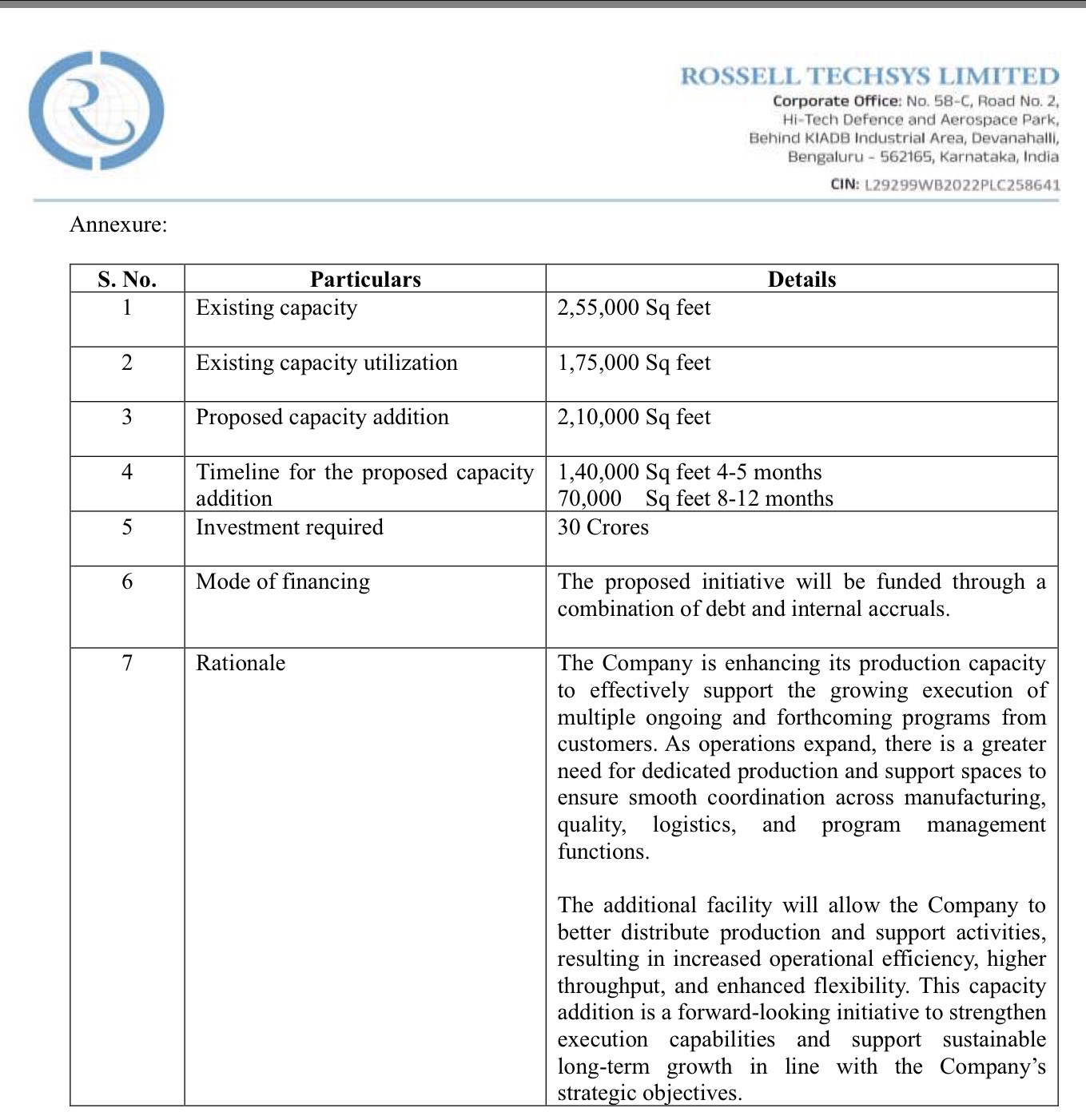

14-Capacity Addition & Funding.

a. A Two-Phase Expansion Plan

The expansion of Rossell’s Bengaluru campus is being done in a phased and practical manner.

-

Short-term expansion: An additional 15,000 sq. ft. is being added to handle immediate demand and enable second-shift operations.

-

Long-term expansion: A new 150,000 sq. ft. facility is under planning. Once completed, Rossell’s total manufacturing footprint will increase from 225,000 sq. ft. to 375,000 sq. ft.

-

Technology upgrade: Alongside physical expansion, Rossell is investing in automated and semi-automated machinery. This is critical for high-volume, precision requirements, especially for semiconductor and advanced electronics customers.

b. When will the Capacity Come Online

The expansion is well-sequenced to match demand visibility.

-

Phase 1: The 15,000 sq. ft. addition is expected to be operational by Q3 FY26.

-

Phase 2: Construction of the larger facility is scheduled to begin in Q4 FY26, with a build and ramp-up period of roughly 18 months.

c. How the Expansion Is Being Funded

Scaling at this level requires a strong balance sheet and careful capital planning.

- QIP funding: Rossell plans to raise up to ₹300 crore through a Qualified Institutional Placement (QIP). This will support both capex and the working capital required to execute a large order book.

Internal cash and debt: The company will also use internal accruals and measured bank borrowing. As of early 2025, total borrowings were around ₹240 crore.

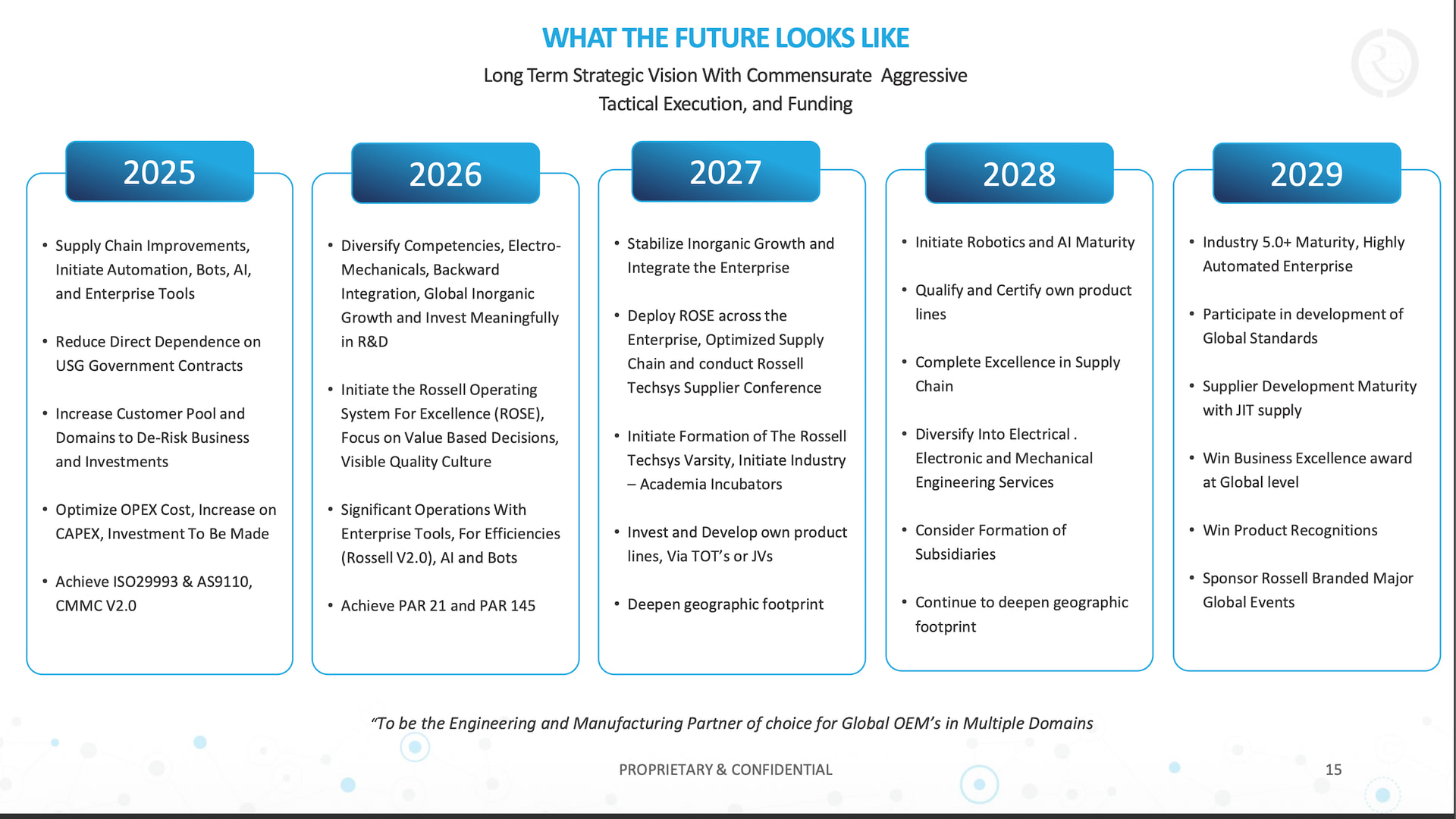

15. Next 5 years roadmap.

16-Financial Health & Long-Term Vision.

Rossell Techsys is currently in a “non-linear” growth phase, having transitioned from a period of heavy investment into a profitable turnaround.

Revenue & Profitability Turnaround

-

The Surge: H1 FY26 revenue reached ₹212.24 crores, more than doubling the ₹95.9 crores achieved in the same period last year.

-

Turnaround: Profit Before Tax (PBT) turned positive at ₹10.7 crores in H1 FY26, marking a significant recovery from prior losses.

-

Margin Profile: The company targets an EBITDA margin of 18% to 22%. Current gross margins (37-38%) are temporarily compressed due to First Article Inspection (FAI) costs—the “learning curve” required to qualify new products for new customers.

-

Revenue Mix: Defence remains the core (60-65%), while the Space and Semiconductor sectors are expected to contribute 40% of revenue by FY27.

Capital Structure & Efficiency

-

Inventory Management: The business holds 5-7 months of inventory to de-risk defence contracts. The goal is to reduce this to 3 months within 18-24 months.

-

The QIP: The company is evaluating a ₹300 crore fundraise through a Qualified Institutional Placement (QIP) to pay down debt (currently ₹240 crores) and fund expansion.

-

Capex: A ₹70 crore facility expansion is underway in Bengaluru, adding 150,000 sq. ft. of production space.

The $240 Million Roadmap (2034)

The company has set a long-term revenue vision to achieve $200 million to $240 million (approx. ₹1,600–₹2,000 Crores) by the year 2034:

-

The Americas: $100M–$120M.

-

Middle East: $50M–$60M.

-

Europe & Australasia: $25M–$30M each.

17-Order Book & Strategic Momentum.

Rossell’s future growth is underpinned by a massive “bank” of confirmed work and long-term strategic relationships with global giants.

a. The Pipeline Numbers

-

Confirmed Order Book: As of September 30, 2025, Rossell holds over ₹700 crores in firm, ready-to-execute purchase orders.

-

Strategic Agreements: The company has long-term agreements valued at over ₹2,500 crores. These are foundational contracts (typically 3-5 years) with major OEMs like Boeing and Honeywell.

-

Recent Activity: In Q2 FY26 alone, the company submitted bids and secured firm orders totalling ₹932.2 crores.

b. Flagship Program: Boeing T-7A Red Hawk

-

The Deal: A long-term strategic agreement with Boeing to supply electrical wire harnesses and cockpit panels for the T-7A pilot training system.

-

Status: Deliveries have started. While the initial ramp-up was slow due to design changes within the program, those changes are now implemented.

-

Outlook: A significant ramp-up in production volume is expected to start in FY27, with the program gaining full momentum over the next 18-24 months.

c. Sector Expansion (Space & Semiconductors)

-

Satellite Broadband: Secured a “significant order” for components, with production ramp-up expected shortly after Q2 FY26.

-

Semiconductor Speed: A new customer in the semiconductor domain saw revenues ramp up significantly in the very first quarter after Rossell was qualified.

-

Global Qualification: A leading global customer recently qualified Rossell for their wire harness requirements, serving as a key future revenue driver.

d. Upcoming Contracts

- Lockheed Martin: Rossell is currently in the process of securing another contract from Lockheed Martin, which is expected to be finalised by the end of the calendar year.

18-Key Risks to Watch.

-

Customer concentration: Revenue is heavily dependent on a few large U.S. defence customers. Any program delay or order rescheduling can impact cash flows.

-

U.S.-centric exposure: Most revenue comes from exports, with a large share tied to the U.S. market. Policy, trade, or geopolitical changes could affect demand.

-

Working capital intensity: High inventory levels (5–7 months) and upfront material purchases tie up cash and create funding pressure, reflected in the planned ₹300 crore QIP.

-

Margin volatility: New programs involve learning curves, leading to short-term fluctuations in profitability.

-

Regulatory and compliance risk: Defence manufacturing requires strict adherence to ITAR and cybersecurity norms. Any lapse could impact market access.

-

Execution risk post-demerger: As a newly independent entity, operational and talent-retention risks remain in the near term.

Disclosure: Holding a small quantity of Rossell Techsys (allotted at demerger @ ₹71). Not investment advice.