Interesting news from today.

1 Like

Good Points. A lot of interesting observation. I am sure if PNB being PSU is so confident, Repco will be way ahead in terms of NPA handling. and LAP specifically.

It was given that LAP will be problematic once tide of asset inflation turns. Unfortunately all events were too sudden to react.

Isn’t Repco also a PSU like PNB Housing?

It is interesting to see what Reliance Housing Finance is doing in this space.

I have a doubt in how the deferred tax asset is calculated with respect to provision for npa

For example in the latest AR , page 68, note 4, the Provision for Non Performing, Standard Assets and Contingencies is 34.45 crore rupees, where does this come from ? how is this calculated?

Thanks in advance

Average cost of funds at 9.2%; further declines soon: Repco Home

With Banks cutting MCLRs and hence housing loan rates, they may give tough competition to HFCs in the salaried customer space where both compete. HFC margins may come down. In this situation, probably Repco could be at an advantage vs other HFCs as it lends a big percentage to retailers/non-salaried where banks generally don’t lend. Additionally, since it borrows a big percentage from banks who have cut down MCLR, its borrowing cost could also come down significantly in next few quarters.

3 Likes

The interview confirms that it would not suffer margin compression and growth slowdown is given. Not sure how much is discounted.

The article clearly suggests REPCO will be able to match competition since it is still largely dependent on bank funding

1 Like

Knight Frank tracks the primary housing markets of eight cities — Delhi-NCR, Mumbai, Kolkata, Chennai, Bengaluru, Hyderabad, Pune and Ahmedabad. It says that housing sales shrunk by 44% yoy in these eight cities in Q4.

It says that New home launches fell by 61% yoy in Q4 in these cities!

The Delhi-NCR market was hit hardest with sales volume dropping by 53% yoy in Q4 while new launches falling by 73%!!

H1Fy17 sales were positive with 7% yoy growth but H2Fy17 was below the comparable period last year!

Disc: Not invested

These cities are not the target market for Repco.

Repco is present chennai particualry in sub urban area

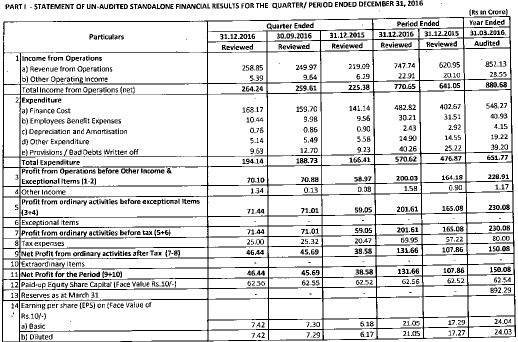

Q3 Results on Feb 13

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=8754480b-38c2-4be9-a569-d233570f2cb2

Result is out… Around 20% yoy growth in top/bottom line.

1 Like

Repco GNPA and NNPA levels are quite high this qtr. Please go through the detailed presentation in BSE

Also can anyone share the conference call details ? Thanks

its at 3 pm the concall

Very True.

can any one explain NPA (before Regulatory Forbearance) and further insight on how is it different /impact?

The RBI had allowed an additional 60 days on top of the usual 90 days due to demonetisation; so a with forbearance NPA means the payment is 150 days delayed without means 90 days.

But I feel, we need not panic Repco over the ast 14 -15 years has net NPA of .05%. They have exemplary record. Also unlike Gruh, they shared a lot of details in the presentation in difficult times. Level of transparency pretty good.