50 PE srock doing a 4% rev dgrowth deserves a big fall.

But i wont be surprised if it doesnt crack in this overheated market. their last quarter also was bad. but nothing happened to the price.

not invested.

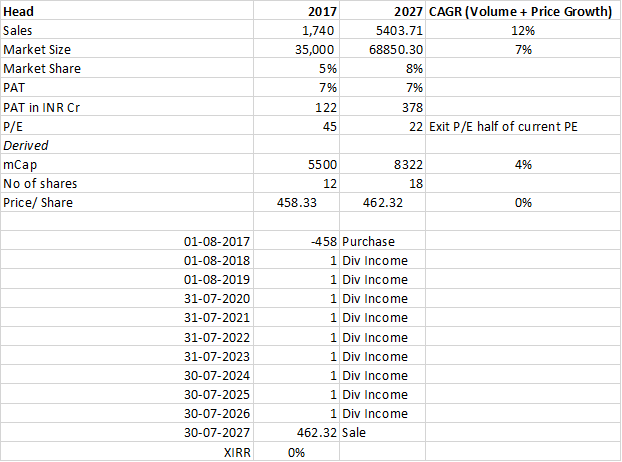

On 12/5/2017 , Relaxo declared a dividend of Rs 1 per share

With this announcement Relaxo has returned back Rs 33 per share to a shareholder who has been invested in Relaxo since 2005 without selling or buying a single share. The share price of Relaxo in 2005 was roughly around the 33 levels. The share price now is Rs 500.

The total investment of this shareholder is now free of cost and he has 10 times more shares now than he had in 2005 because there were splits and bonuses along the way. His Rs 33 ( Rs 33 X 1 share) investment in 2005 i now worth Rs 5000 ( Rs 500 X 10 shares ). An astounding gain of 151 times. or a CAGR of 58% in 12 years.

These returns could have been achieved by this shareholder even if the stock market had remained SHUT in these interim 12 years

How is that for wealth creation without wasting time looking at market prices?

But as an investor through this period another thought enters the mind - is the stock overvalued now even as it gives me more in dividends than the price I paid for it 12 years ago (as mentioned)? That’s because the stock has not only done nothing over the past 2 years; it has lost ~13 % in quoted value. An investor who measures his wealth in quoted prices (and like every human, suffering from loss aversion) will feel he has actually lost and not gained. Even when the above facts on dividends are placed before him. He will say (atleast in private) - ‘wish I had exited 2 years ago and just put the proceeds in an index fund’.

It also torture tests the emotional fortitude of those who in good times say ‘hold on to a quality stock almost irrespective of its price’; but find it difficult to hold on when the stock does nothing for a few years.

In terms of business performance it has grown its earnings by 9% pa over two years and by ~2% last year; now quoting at a TTM multiple of about 48.

Of course these thoughts would never have entered my mind if the markets were closed!

I never held the stock in meaningful quantities and could well be a sore loser

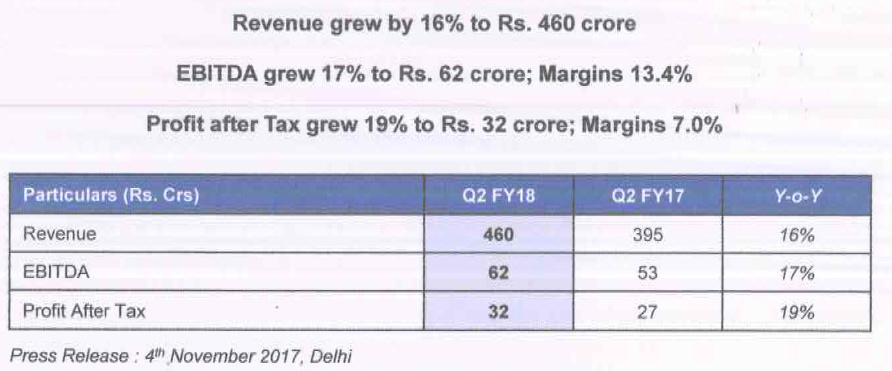

The results are getting better every quarter. This quarter is just stupendous - high margins, high growth in sales and profit, lower debt…all round improvement.

Relaxo Footwears Ltd. FY18 Notes

Like 2-3 years in the past this year’s Annual Report also showed management’s focus on new products launches, streamlining distribution network and new geographies. Company made some strategic changes during the year like company moved away from category led sales to geography led sales organisation structure. Company is investing heavily in capex but the details were not mentioned. In the latest Credit Rating Report of the company in July 2018, ICRA revised the outlook from Stable to Positive. Following are the notes compiled from Annual Report 2018 and ICRA’s Credit Report.

Growth in sales of 19%, EBITDA growth of 31% and PAT growth of 34%.

Company has 8 state of the art manufacturing facilities, 6 in Bahadurgarh (Harsyana) and 1 each in Bhiwadi (Rajasthan) and Haridwar (Uttarakhand).

Company achieved landmark target of opening 300th exclusive retail outlet. Total outlets increased from 270 to 302. These are on Company Owned Company Operated (COCO) model.

During the year company opened 8th franchise outlet (FOFO) in eastern region on experimental basis.

Company plans to open 30-40 more COCO/FOFO in FY19.

Focus on in-season launches with an optimal product portfolio has enabled us to deliver right product at right price at right time.

Streamlined the distribution network in underpenetrated market which has given substantial incremental sales.

Good growth in No. of Pairs sold during the year, from 13.46 cr pairs in FY17 to 15.74 cr pairs in FY18 a growth of 16.93%.Average Revenue per Pair increased from Rs. 122 to Rs. 124.

In order to maintain optimum inventory level, retail division has focused on store to store stock rotation and liquidation of aged inventory resulting in improved inventory days.

Company continued it’s efforts in international markets with special focus on Middle East, Africa and Oceania.

Company has opened an offfice in Dubai to cater to export markets of Gulf and South East Asia.

Employee cost increased from Rs. 177 cr to Rs. 214 cr, increment of 20.90%.

Debtor Days increased from 28 days in FY17 to 35 days in FY18.

EBITDA margins improved from 14.15% to 15.37%.

Capex done of Rs. 108 cr during the year.

Debt decreased from Rs. 176 cr to rs. 153 cr.

Advertisement exp increased from Rs. 69 cr to Rs. 86 cr. at 4.39% of sales.

Management remuneration increased from Rs. 22.69 cr. to Rs. 29.90 cr

Promoter’s stake decreased very slightly from 74.93% to 74.25%.

Company has a pan India network of distributors and retail stores supplying Relaxo products through more than 50,000 point of sales (POS), resulting in high geographical and customer diversification.

North India accounts for 50% share of revenue.

Over the years Hawai Slipper sales have come down to 29% of the total revenue and sales of higher value products have increased, Average Revenue per Pair increased from Rs. 111.80 in FY14 to Rs. 124.20 in FY18.

As per Businesswire, Indian Footwear Industry can grow upto 100% in next 5 years.

Bollywood actors like Salman Khan, Akshay Kumar, Shahid Kapoor and Shruti Haasan endorse co’s products.

Good info.

However, P/E re-rating (upward) is faster than growth rate. Hence, investors need to wait for longertime for good return…price will wait for growth to catchup

Consumer spending does not look good , even in low ticket price purchases like shoes. Looks like the company had to push stocks by giving more discounts.

While consumer spending trend over last few quarters has been changing/shifting but surprised to see this for relaxo considering the product to be a footwear. Is this information through channel checks? Just wondering on the accuracy of the source.

Total 9 plants: 6 in Haryana, 2 in Rajasthan and 1 in Uttarakhand.

Started commercial production in Bhiwandi for manufacturing Flip Flops in FY19.

During the year company re-strategized it’s export presence from an opportunistic geographic footprint to a focused international presence with a nation specific product portfolio and a dedicated onground sales team. The branch office opened in Dubai in last year and restrategizing export plans is expected to give boost to export sales and expand its business to newer geographies.

Post GST economic transmission from informal to formal has created a level playing field for organised sector.

Company continued it’s strategic initiative to strengthen it’s distribution network especially in under penetrated markets.

No. of pairs sold 18.39 cr at 16.90% growth yoy. (FY18: 15.74cr and FY17: 13.46 cr)

FY15

FY16

FY17

FY18

FY19

Sales

1480.81

1711.81

1651.97

1948.57

2292.08

No. of Pairs

12.28

13.55

13.46

15.74

18.39

Realisation per pair

120.58

126.33

122.73

123.80

124.64

The Company received order from NCLT Delhi for merger of Relaxo Rubber Private Limited and Marvel Polymers Private Limited (Transferor Companies) with your Company and subsequently allotted 36,18,453 fully paid up equity shares of Rs. 1/- each to the shareholders of transferor Companies during the year.

Capex during the year Rs. 258 cr, It includes 153 cr due to amalgamation. Net cash capex was rs. 105 cr.

Debt as on 31.03.2019 Rs. 112 cr.

R&D exp of Rs. 3.52 cr in FY19.

Advertisement expenses for FY19 is Rs. 76.76 cr (FY18 is Rs. 73.93 cr).

Forex earned Rs. 87 cr (Rs. 45.64 cr in FY18).

Revenue from operations increased by 17.63% to Rs. 2292.08 Crore from Rs. 1948.57 Crore in the last financial year.

EBITDA increased by 7.36% to Rs. 324.31 Crore from Rs. 302.09 Crore in last financial year.

Net profit increased by 8.92% to Rs. 175.44 Crore from Rs. 161.07 Crore in the last financial year.

Total retail outlets increased from 302 to 343 during the financial year. Company continued to expand its retail chain through COCO (Company owned Company operated) stores. The asset-light, FOFO model (Franchisee owned Franchise operated) has given a positive response encouraging the Company to venture into newer territories. We plan to open 50-60 more COCO / FOFO stores in FY20.

Fiscal 2018-19 was a great year as its new products in the shoe category gained healthy customer acceptance.

Relaxo Footwears Limited (RFL) had existing capacity of 7.50 lakh pairs per day for manufacturing footwear. To derive benefits of synergies and to meet peak season demand and to be ready for future growth, RFL is proposing to add capacity of 1.00 Lakh pairs per day of footwear in Bhiwadi Rajasthan. The capacity will be added in three years. The total investment required for installation of the proposed Plant is - Rs. 90 Crores.

The capacity utilization of the existing plants is - 75% which goes upto - 90% in the peak season.