negative sales growth and their return on incremental capital also declined drastically.

1 Like

Hi,

Can someone please help me understand why there has been a significant increase in the traded volume (buy/sell) recently? It appears to be at or near an all-time high.

Could you please confirm if there is any positive trigger or event driving this unusual activity in the stock?

1 Like

actual reason is unknown (atleast for me), but this is the explanation the company has officially provided to the exchange.

1 Like

The Bamboo Theory: Why I am Buying the ‘Silence’ in Relaxo

How a boring footwear company is mastering the art of growing downwards.

The Promise in the Dust

Walk into a general store in rural Uttar Pradesh. Amidst the hanging sachets of shampoo and jars of candies, ask for a slipper. The shopkeeper doesn’t sell you a product; he sells you a promise. “Take this, sahib. It won’t break.”

Relaxo is the custodian of that promise for 400 million Indians. It is the asphalt of the economy—rugged, essential, and invisible.

But right now, the silence around the stock is deafening. The crowd says “Death.” We say “Dormancy.”

We are looking at a Chinese Bamboo scenario. For four years, the bamboo grows roots underground with zero visible shoots. In the fifth year, it shoots up 80 feet in six weeks.

The Question: Did it grow 80 feet in 6 weeks, or in 5 years? The Answer: It grew in 5 years. For 4 years, it was growing roots —deep, complex networks underground to support the massive weight that was coming.

Relaxo is in Year 4. Here is the Deep Dive into the root system.

The Crucible: Why the Bamboo Went Underground

(The Context & The Challenge)

To understand the beauty of the strategy, you must first respect the ugliness of the situation. The management didn’t choose this difficult path out of boredom; they chose it out of necessity.

The Bleeding (Q2 FY26 Context):

- Revenue: ₹629 Cr, down 7.5% YoY .

- Profit: Flat.

- The Narrative: The “growth compounder” is broken.

The Trap: Relaxo was caught in a “pincer attack”:

- The “Blind” Supply Chain: For years, they force-fed distributors to hit targets (”Channel Stuffing”). Revenue looked good, but stock was rotting in godowns. They had no real data on what the customer was buying.

- The “Pest” Problem: Unorganized players (Agra/Delhi clusters) were evading taxes and undercutting Relaxo by ₹30/pair. In rural India, ₹30 is a dealbreaker.

The Hard Choice: Most managements would stuff harder to hide the problem. Relaxo’s leadership chose to stop the drug. They voluntarily cut primary sales (causing the revenue drop) to clean the pipes. They traded short-term vanity for long-term sanity.

The Four Pillars of Reinvention

(The High-Leverage Strategic Pivot)

Management has moved from a passive “General Trade” model to an “Optimized Engine.” This isn’t just a tweak; it is a four-part reconstruction of the business.

Pillar 1: The Revenue Integrity Pivot (Digitalizing the Channel)

From “Stuffing” to “Sensing”

The pivot shifts control from the distributor to the management, fixing the core issue of opaque sales data.

- The Action: Deployment of the Relaxo Parivaar App (RPA) . They onboarded 100,000+ small retailers directly to track final retail sales (”Secondary Sales”) and purge non-compliant distributors.

- The Consequence: They are deliberately starving the channel of excess inventory to build a “Pull” model. While this makes revenue look terrible today (First Order Effect), it guarantees that future growth is high-quality and predictable. They now know exactly which color Flite slipper is selling in a specific district in Bihar.

Pillar 2: The Competitive Pivot (Weaponizing Policy)

The Winter Strategy

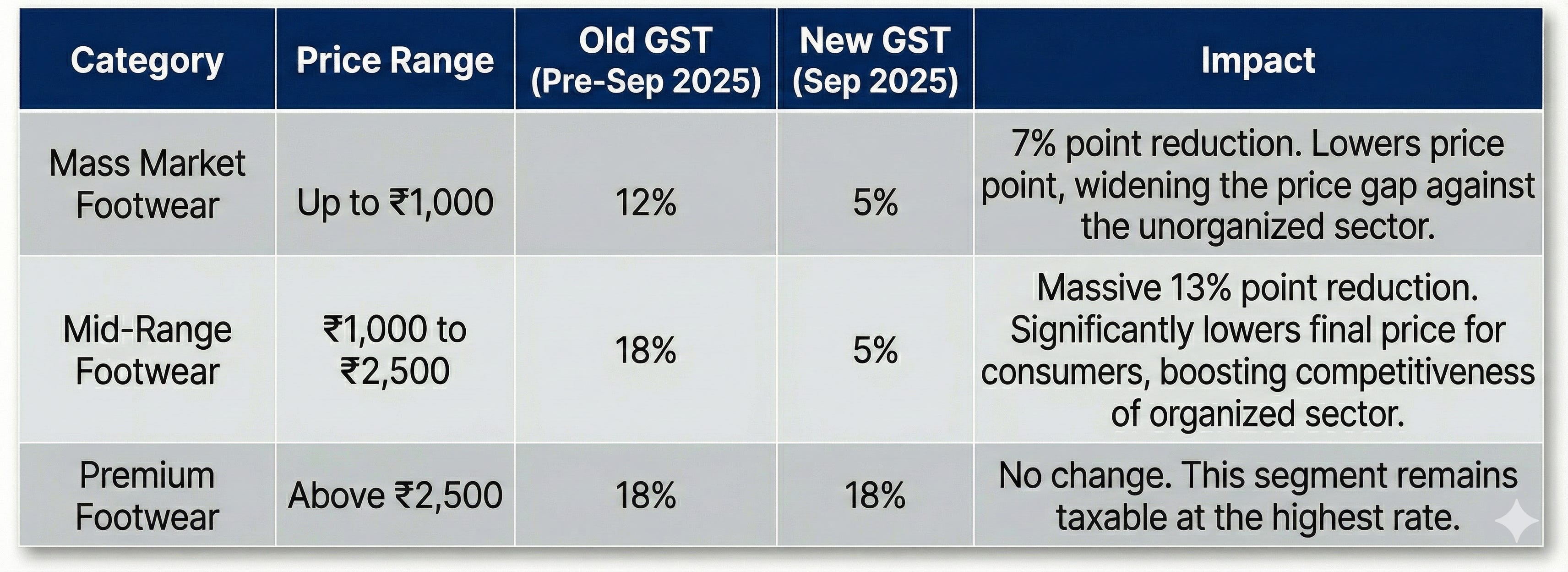

This pivot creates a permanent, policy-driven price advantage. When the government slashed GST to 5% (for items <₹2,500), Relaxo didn’t pocket the margin. They weaponized it to create a “Volume Engine.”

- The Kill Zone: They dropped their Average Selling Price (ASP) to ~₹153, shrinking the gap against unbranded “local chappals” to just ₹20-30.

- The “Sparx” Unlock: In the premium segment, the shift from 18% to 5% GST creates a mathematical anomaly.

The Verdict: The organized product becomes structurally cheaper than the unorganized competition.

Pillar 3: The Quality Pivot (Structurally Lifting Margins)

Beyond the Chappal

This is the pivot the market is missing. Management is ensuring that when volume returns, the profit earned per pair is permanently higher.

- The Mix Shift: They are aggressively moving the mix toward Closed Footwear (Sparx sneakers/shoes) vs. Open Footwear.

- Value Engineering: By focusing on cost efficiency and higher-value products, they are structurally elevating the Return on Capital (ROC) base.

- The Insight: This isn’t just about selling more; it’s about a favorable margin mix. They are securing a long-term profit baseline above historical averages.

Pillar 4: The Capital Pivot (Activating Sunk Assets)

The “Empty Factory” Paradox

This pivot maximizes returns on assets already owned while eliminating unnecessary financial risk.

- The Discipline: Management has severely curtailed new growth Capex (₹61.64 Cr in FY25 , down drastically from ₹231.80 Cr in FY24 ).

- The Math: With the factory at 56.5% utilization , the recovery will trigger non-linear profit growth. They don’t need to spend a Rupee to grow.

- The Target: This operating leverage is expected to drive a surge in EBITDA Margins (targeting 13.7% → 15.0% ), maximizing the PAT for a debt-free balance sheet.

The Catalyst: GST 2.0 (The “Needle Mover”)

While the internal pivot is great, the external environment is about to provide a massive tailwind. The upcoming GST rationalization (effective September 2025) fixes the inverted tax structure that has held the industry back.

The Shift: Previously, any shoe over ₹1,000 was taxed at 18% . This created a “glass ceiling” for mass-market brands. GST 2.0 slashes the rate to 5% for footwear up to ₹2,500 .

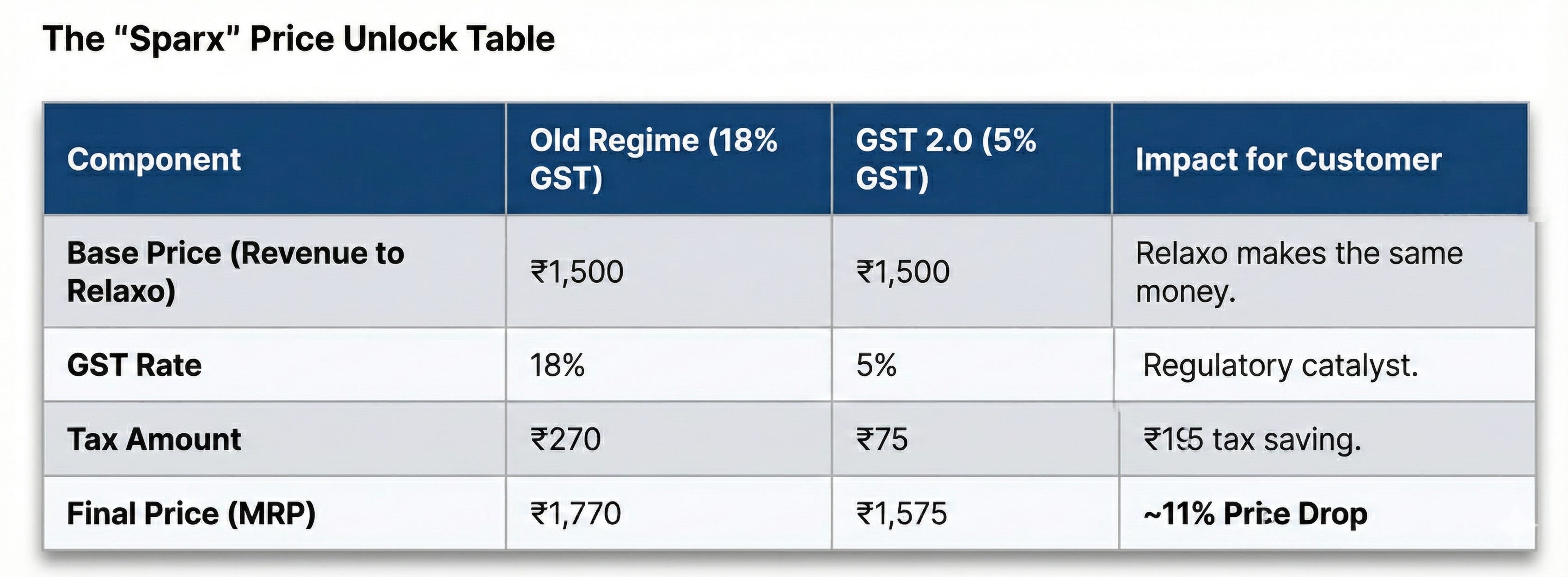

The Customer Benefit: A Real-World Example

How does this actually help the consumer and drive volume? Let’s assume Relaxo decides to pass on the full benefit to gain market share.

The Result: The final price drops by ~11% . This 11% reduction is critical because it makes a branded Sparx sneaker cheaper than many unorganized alternatives, destroying their value proposition.

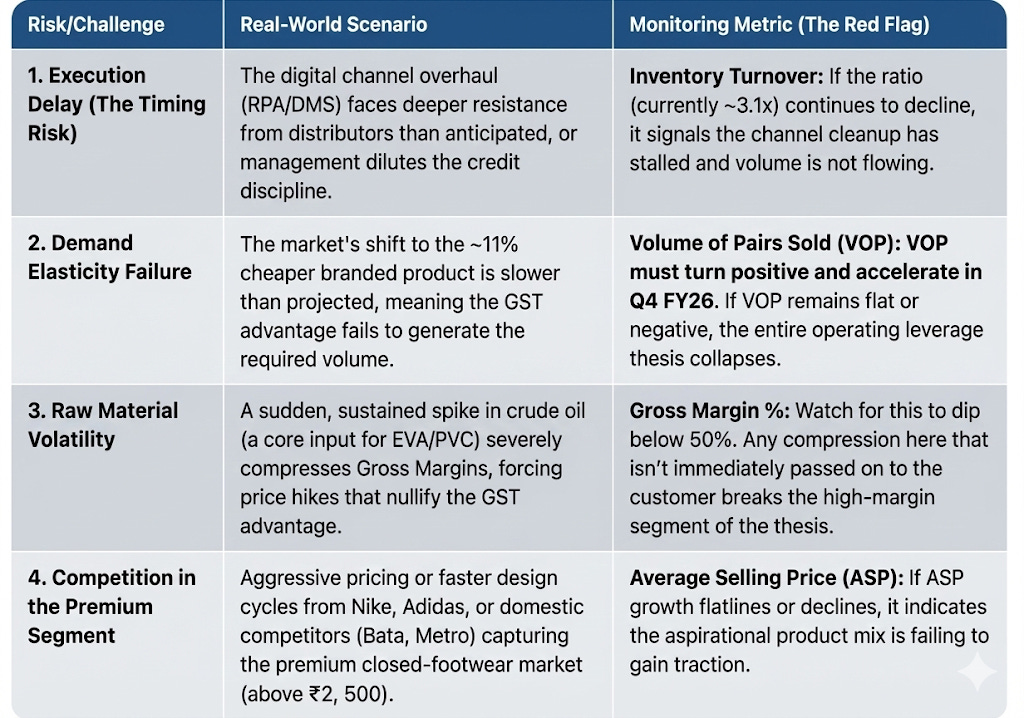

Risks and Challenges: What to Monitor

The biggest risks to the thesis are not financial collapse, but execution failure and external demand shocks . Given the premium valuation, any delay in the volume recovery will be harshly penalized.

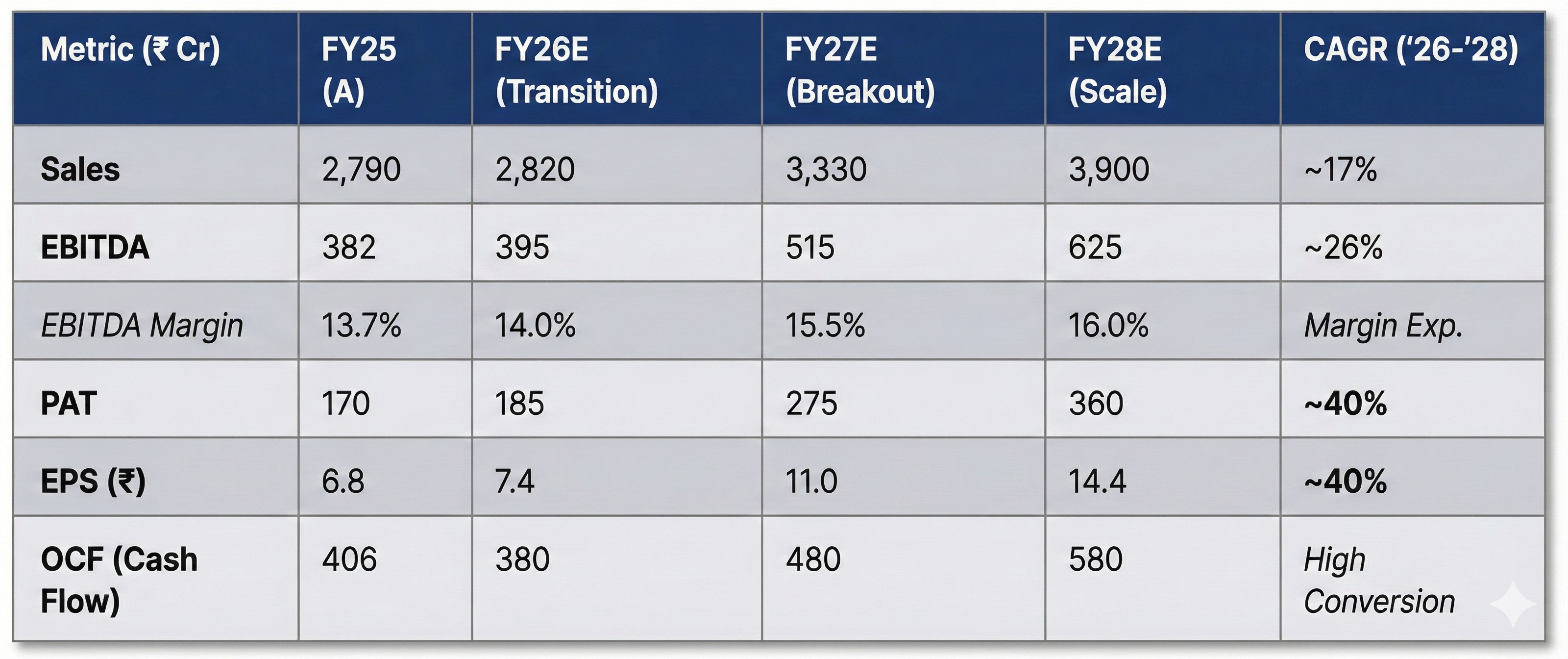

The Financial Shoot: The Math Behind the Bamboo

(FY26E - FY28E Projections)

If the Bamboo Theory holds true—if the roots (distribution) are set and the fertilizer (GST 2.0) is applied—the financial “shoot” will be vertical.

We are modeling a transition year (FY26) followed by two years of non-linear breakout (FY27-28).

The “Source of Truth” (Decoding the Numbers)

1. Sales: The Volume Engine (FY27 is the Key)

- The Remark: FY26 stays flat as we finish “cleaning the pipes” (Pillar 1). The 18% jump in FY27 isn’t magic; it’s the GST 2.0 tailwind killing unorganized competition + the Premiumization of Sparx driving higher realizations.

2. EBITDA: The Efficiency Engine

- The Remark: This is the “Empty Factory” dividend. We are moving from 55% → 82% utilization without adding new fixed costs. When you sell more shoes using the same machines and staff, margins naturally expand (13.7% → 16.0% ).

3. PAT & EPS: The Wealth Multiplier

- The Remark: Profit grows 2x faster than Sales (40% CAGR). Why? Because Relaxo has stopped new Capex (Pillar 4). With flat depreciation and zero interest cost, the entire EBITDA gain flows straight to the bottom line.

4. OCF: The Reality Check

- The Remark: OCF is slightly lower than EBITDA because growth has an entry fee. We assume ~₹75 Cr gets stuck annually in Working Capital (Inventory/Debtors) to support the volume surge. This is the healthy “Growth Tax” of a scaling business.

The Valuation: The Shopkeeper’s Math

To understand Relaxo’s price, we ignore complex models and look at three business realities: The Utility, The Peers, and The Cash.

A. The Consumption Angle: The “₹2 per Day” Subscription

Why is Relaxo’s revenue quality superior to a fashion brand? Because it is a utility.

- The Math: A pair of Bahamas costs ~₹400 and lasts 6 months. That is ₹2.2 per day .

- The Moat: It costs less than a pouch of Vimal . At this price point, demand is inelastic. Relaxo doesn’t need to steal market share to grow; it just needs India to hit the global average of 3 pairs/year (vs current 1.7).

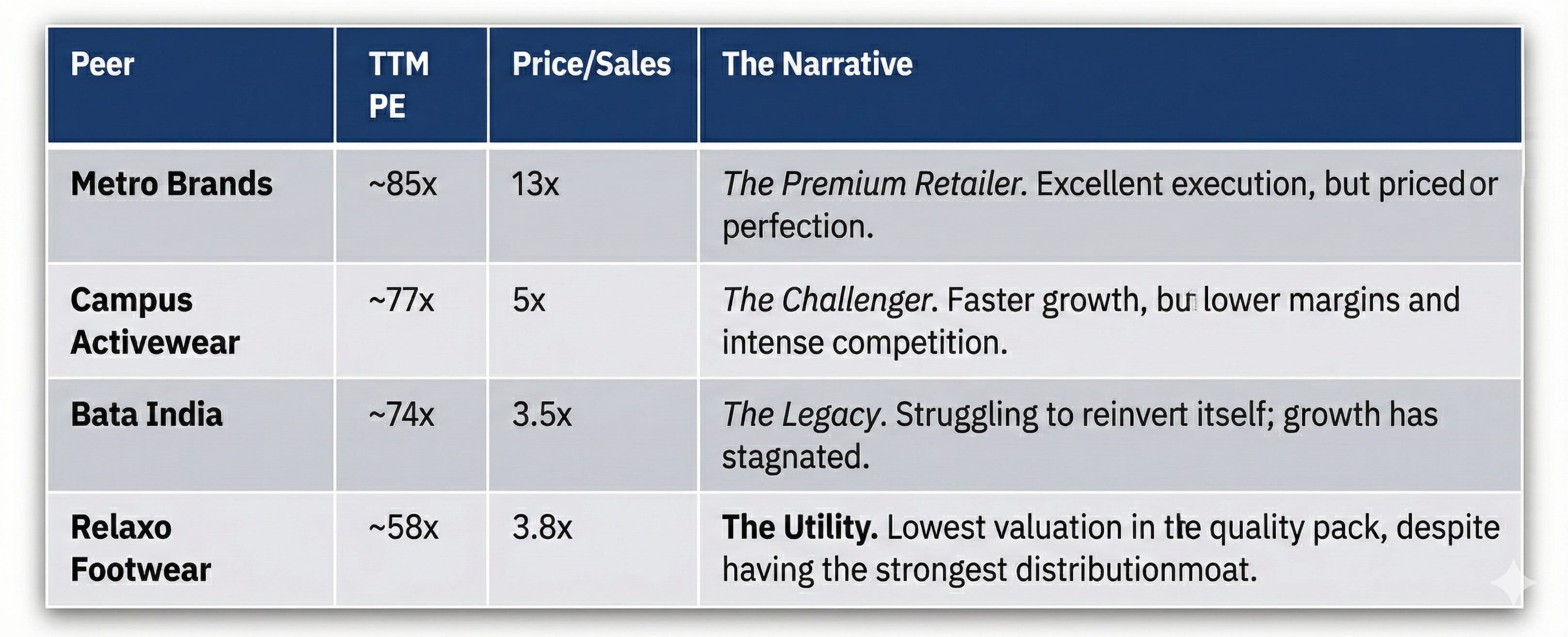

B. Peer Comparison: The “Relative Value” Check

Is Relaxo expensive? Let’s look at the neighborhood. The market assigns premium multiples to footwear companies because they are high-ROCE, cash-rich franchises .

C. The “Cash is Truth” Rationale

Why we use Operating Cash Flow (OCF) > Net Profit (PAT)

In a turnaround, Net Profit lies. Relaxo has huge non-cash expenses (Depreciation) from its recent factory expansion, which artificially depresses Net Profit. OCF adds that back.

- The Logic: You are buying an Inflation-Protected Bond . Its cash flow rises with rubber prices and population growth.

- The Price: Paying 40x OCF for a dominant monopoly growing at 17% (with 0% Debt) provides a massive margin of safety compared to paying 50-60x for slower FMCG stocks.

The Investor’s Mental Model

(Why the algorithm hates it, but we love it)

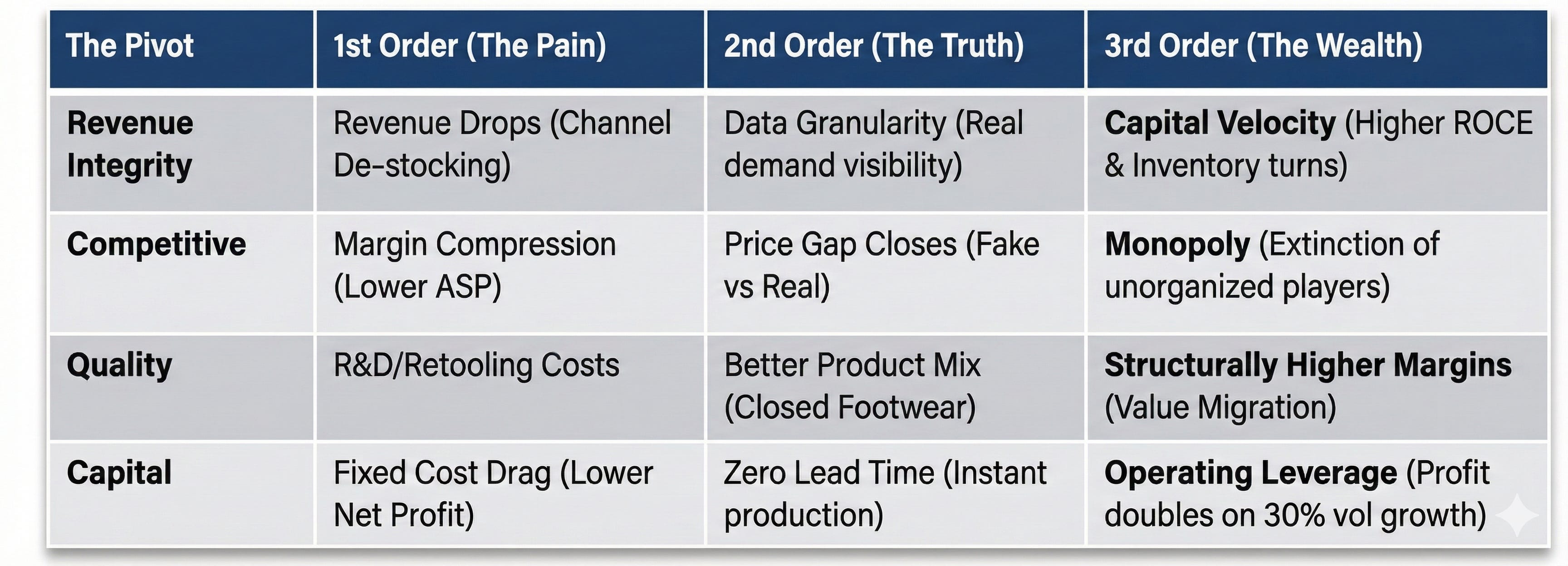

The reason Relaxo has flatlined is that the market is stuck on First Order Thinking . As investors, we need to look at the Consequence Chain :

The Takeaway: The market is pricing the stock based on the “1st Order Pain.” We are buying the “3rd Order Wealth” at discount.

The Verdict: The Shoot

Investing is often about differentiating between a business that is broken and a business that is building. The market sees a broken revenue line. We see a building root system. The First Order effects are visible in the price. The Third Order effects are the hidden optionality.

The Bamboo is about to shoot.

Investment Status & Thesis

• Disclosure: Invested. (No transactions in the last 30 days.)

• Thesis Written On: December 12, 2025

• Current View: Biased due to holding. I plan to exit this position only if there are material corporate governance lapses.

• Strategy & Risk: This is a thesis focused on a strategy pivot, and I will be closely monitoring execution. If the thesis fails to materialize, I will exit the position. This is a small, initial allocation (max 1% of the total portfolio).

Formal Disclaimer

I am not a SEBI-registered research analyst or investment advisor. Nothing in this post constitutes investment advice, a recommendation, or a solicitation to buy or sell securities. All cited facts are sourced from the company’s official filings and the Q2 2025 earnings call.

Please conduct your own thorough due diligence before making any investment decisions. Your capital, your responsibility.

10 Likes

Excellent thought .. But one should focus on BIG picture ..

Indian Pop : 150 crores and Relaxo sells 19 crores of pairs of footwear ..

That is good penetration .. so what is problem with Relaxo .. It is cheap functional brand .. that sells @ Rs 160 ARPU ..

So issue is of brand APRU uplift .. It may get some one time growth because GST .. but that will be just for one year FY 27 .. Post that its problem persist .. ie will grow at 3- 7% in long run

Hence it should quote at PE of 10 -15 .. Yes PE of 10-15 .like it did pre 2009 ..

You cannot compare this franchisee with HUL of world which has negative working capital .. This company has decent trade receivables of and has cash conversions cycles > 100 days ..

1 Like