@deevee - You can DM me in case you require any price data from NSE. I can provide NSE stock prices data in any format you require,

2 Likes

Hi

There has been a block deal in RBL

Also RBL replaces Karnataka Bank in the Private Bank Index

Got this news from a friend.

Rgds

Deepak

More on the block deal here:

1 Like

Hi

Was watching ET Now in the morning and they had the CEO Teresa Barger of Cartica Capital talk about RBL.

Cartica capital has 36% odd exposure to India and she said out of all the emerging economies she felt India was the most ‘Trump’ proof.

As far as I recall she said that she holds 3% odd in RBL from times before IPO. She emphasized the management change in a positive manner. She was bullish on ‘financialsation’ in India and said its a 3-5 year theme. Cartica capital has 7 holdings in India.

Regards

Deepak

2 Likes

One of the things that RBL powers from the backend or through collaboration are quite interesting technology start-ups and companies.

-

Happay - Happay is a expense management system start-up, used by around 4000 companies like Oyo, Symphony, Urban Ladder, etc. The Visa cards are issued by RBL - https://www.happay.in/terms.html Happay can be compared to Coupa which went for an IPO last year http://www.nasdaq.com/symbol/coup

-

PayUmoney - RBL powers the virtual wallet for PayUmoney http://www.thehindubusinessline.com/money-and-banking/payumoney-partners-with-rbl-bank-to-offer-virtual-wallet/article6805069.ece

-

BookMyShow - Pretty much everyone in my office has this card and I think RBL did a good job at marketing / introducing it bundled with free movie tickets like other banks - https://in.bookmyshow.com/offers/rbl-bank-fun-credit-card-offer/RBLCC1015

-

Oxigen: Virtual visa cards with RBL - https://www.oxigenwallet.com/virtuale-prepaid-visa-cards

-

The Mobile Wallet - http://indiacsr.in/essars-hazira-township-goes-cashless-with-the-mobile-wallet/ Essar’s Nand Niketan Township becomes India’s First Private Sector Township to go cashless with The Mobile Wallet (TMW). More than 12,000 TMW app downloads. Over 8,000 TMW-RBL Bank Prepaid Card issued. An average of Rs 2 lakh of digital transactions executed every day. More than 1,000 daily transactions executed using simply the TMW app

-

Zeta - You must have seen these stickers everywhere - The cards are powered by RBL https://zeta.in/terms-RBL/

-

Quopn - The online wallet is issued by RBL - http://quopn.com/my_wallet_Terms_of_use.html

Any others that I missed?

I am sure many banks do this too but I feel, RBL bank’s management is positively aggressive in finding new mediums in the field.

9 Likes

Hi

RBL is indeed the forerunner along with YBL amongst the banks for partnerships in the FinTech space imo like Praveen has pointed out.

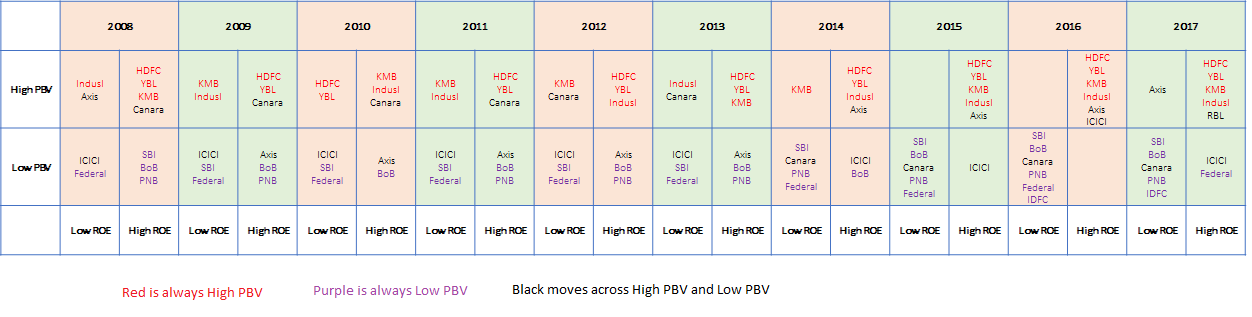

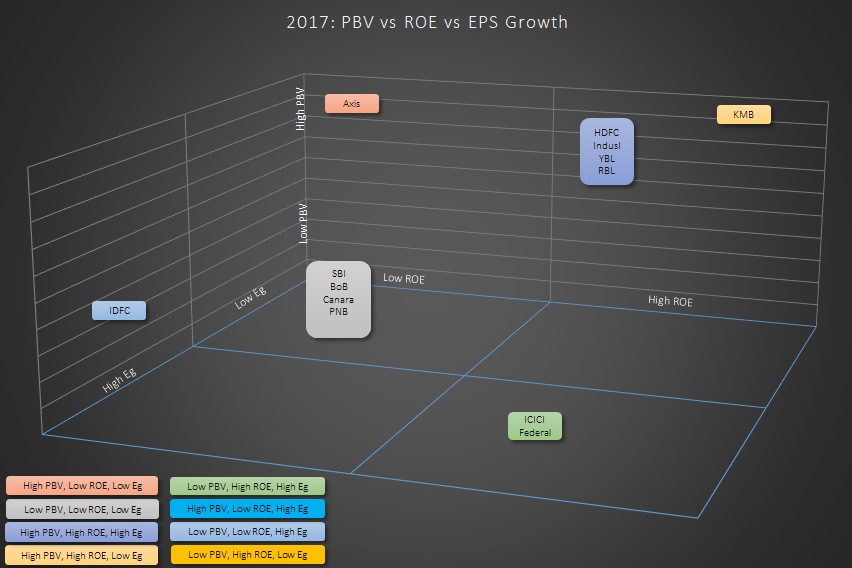

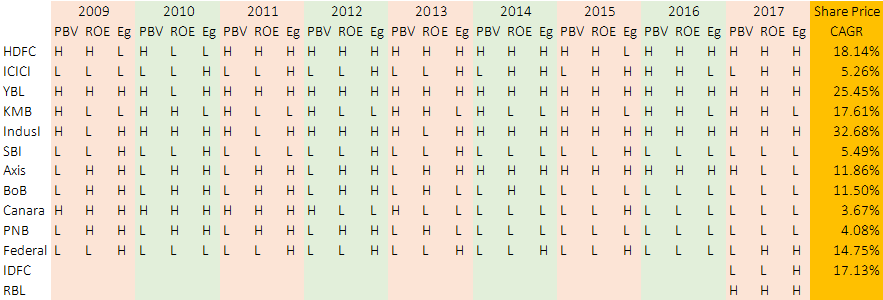

I had to share the relative valuation results which has been pending for a few weeks now. Not reiterating all the points covered before but very concisely putting down the plots/tables. I have put up more details on my ‘scrapnote’ blog (in my profile the link is there). I have put the rationale in the earlier posts too.

There were 2 ways in which we did this

-

Industry median based relative valuation -

Type A: PBV vs ROE (2 dimensional matrix)

Type B: PBV vs ROE vs EPS growth (3d matrix) -

Actual PBV versus Regressed PBV

Results Tables:

2D for 2017 (shared earlier)

2D YoY

(please open the pic for more clarity)

3D for 2017

(not able to paste the 3d matrix generated by R programming - still a learner there so put it on powerpoint!)

3D YoY

Regressed analysis for 2017 (shared earlier)

Now from our previous sections we had 4 outstanding investment candidates in this set of thirteen banks ie HDFC, KMB, IndusI, YBL. For the period 2014 to 2017 I have plotted the difference levels between actual PBV and regressed PBVs for these banks. The plot is below.

(please open the pic for clarity)

Results from this relative valuation approach:

- High PBV, ROE and Eg has translated to higher stock price growth. HDFC, YBL, KMB, IndusI have an average CAGR of ~23%+ from 2008 to 2017 with a median of ~25%. These 4 banks are the only banks which have consistently been valued at higher PBV multiples than industry medians. Also they are the top 4 banks in stock performance. Not a surprise!

- The banks which have consistently been valued at lower PBV multiples than industry median are SBI, BoB, PNB and Federal. SBI and PNB have had below 6% stock CAGR while Federal and BoB have fared better with 14% and 11% stock growth CAGR. In conjunction with the regression analysis we can say Federal looks to be a good option to bet on.

Conclusion is that the top 4 performers are always highly overvalued compared to industry but at the same time their earnings growth and ROE is always better than the industry median. So can we say that since they were overvalued we should not have invested? I don’t know.

Regards

Deepak

p.s. if there is an error please send me a private message. i am a little skeptical of a few things in this because of the kind of data quality I have. Only if I had free data streams ![]()

21 Likes

Has anyone analysed the quarterly results yet? I think it is a very good performance.

NPAT at Rs151crs (68% YOY increase).

1 Like

Q2 results and presentation

http://www.bseindia.com/xml-data/corpfiling/AttachLive/d90673df-33f5-40b0-9336-1524720bf287.pdf

Disc: Not Invested

3 Likes

It would be very much helpful if someone could clear this for me:

I am surprised at recent financial companies earnings growth rates as their ROE s are not so high but Earnings grow at 25-40%.

In case of RBL,

leverage (assets/capital)

30.sep.17 - 8.3

30.sep.2016 - 10.2

As everyone knows, Maximum Self sustainable growth rate = ROE ( assuming no dividend )

EPS

30 sep '16 = 2.44

30 sep '17 = 3.62

Growth = 48%

When leverage hasn’t increased, and ROE hovers around 10-12%, how is EPS Growth so high?

1 Like

Total Asset Turnover is very low, which I guess is dragging the ROE lower.

ROE’s are increasing for RBL due to high growth.

Lets take an example. Lets assume a bank has 100 Rs. capital and ROE of 10. So EPS will be 10. Next year EPS grows by 50%. So ROE goes to 15%. ROE has increased by just 5% for 50% growth. That’s what is happening in RBL right now.

2 Likes

Wrong calculation - if you EPS is 15 next year then the equity capital is 115 and not 100, so your RoE is 13%(15/115) and not 15%(15/100), besides it is not that easy to raise RoE sustainably by even 300 bps in a year for any bank. A 50% growth would readily lower your capital adequacy at the level of 10% RoE (as your growth is far higher than RoE, your capital consumption is very high) and you would soon need to a fund-raising round which will again increase the denominator of equity capital and lower RoE. Most banks guide for many years to reach say from 10% to 15% RoE - doesnt happen like you have mentioned.

6 Likes

A company which reports such growth may not be available cheap ever if it continues to grow at this rate.

1 Like

I just gave a simple example without any details or exact calculations. Why complicate it when it serves purpose of understanding how growth can be more than ROE.

http://www.bseindia.com/corporates/ann.aspx?scrip=540065

Acquisition disclosure by bank. Acquired more than 50% stake in swadhaa finserve pvt ltd.

http://www.bseindia.com/corporates/ann.aspx?scrip=540065

Further stake raised by rbl in swadhaar by 2.08% making total 60.48%

Disc . Invested pre ipo.

@spvk1, regarding your disclosure comment “Disc . Invested pre ipo”, may I know how to invest in companies even before IPO?

3 Likes

@spvk1 you could buy unlisted shares from dealers, brokers dealing in privately held companies…many such dealers are available. just google it and you will get to know…hope this helps!!!

There is a whole thread on that discussion.

http://forum.valuepickr.com/t/buy-unlisted-shares/

Also please subscirbe to Alpha Ideas News letter. Raoji occasionally send email about pre-IPO shares being available. Investor Wisdom Newsletter for Q1 FY2018-19 is out !! – Alpha Ideas

The other option is

These details apart, let us continue the discussion on RBL and its prospects.

1 Like

I am original shareholder of bank. I am from Kolhapur Maharashtra were rbl is having head office. So I am having shares since 2000. Face value was 100 then it was made 10 and then after ahuja took over management he revamped the bank and it’s functioning and then complied all ipo requirements and then there is a ipo and listing.

3 Likes