I remain interested in RBL bank because it is a simple stock picking story where best private bank in each licensing wave has created immense wealth. But I am not convinced to make a case for investment yet -

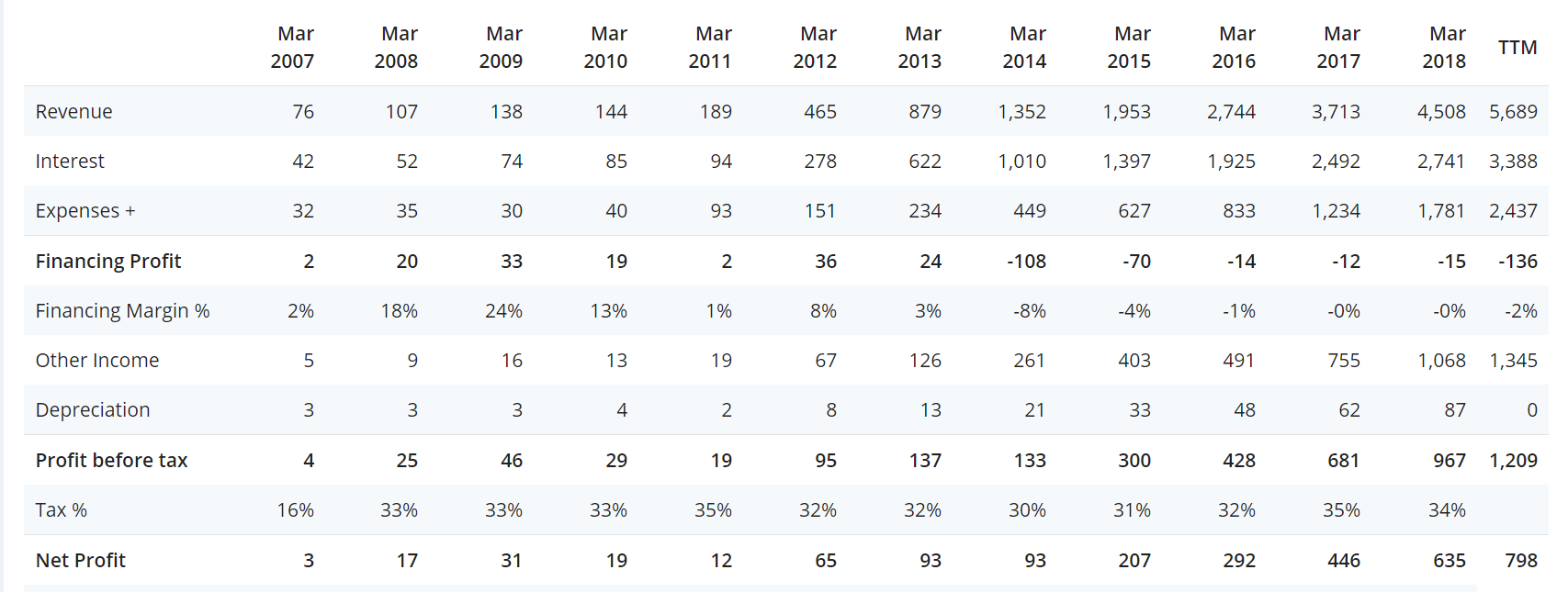

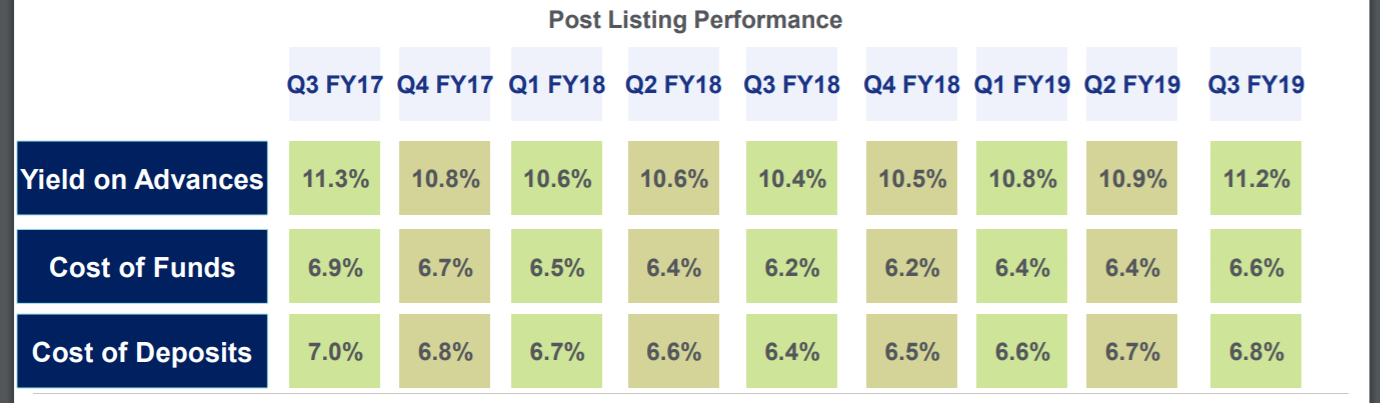

- Since FY14, for RBL bank PBT < Other Income. In screener parlance, this means they are reporting a financial loss i.e. the core banking business by itself is making losses. And this is despite very high NIM of 4%+.

If I am investing in a lending institutions, I would like the core lending operation to be profitable which validates management and business capability.

For a lot of banks like ICICI, Axis, Financing loss is due to higher provisioning on GNPA. But for RBL bank that is not the case. The financing loss seem to be from higher operating expenses.

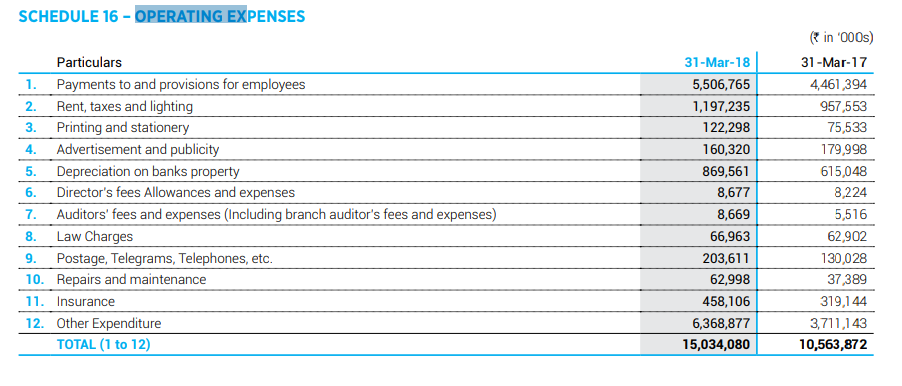

When I tried to find the breakdown of operating expenses, a large portion is towards employee expenses - which is okay as operating leverage will kick in business per branch and employee starts going up.

The real puzzle is other operating expenses for which AR18 provides no details.

It would still be okay to have higher other expenses if investments are made in branches or seeding newer higher quality lending businesses like retail housing finance or personal loans etc. but I don’t think that is the case based on conf calls. Also how much of these higher expenses are due to MFI piece also needs to be seen. In summary, far more details are needed on other operating expenses side.

- The NIM is higher at 4%+ but quality of NIM remains poor i.e. the kind of assets that are leading to these NIMs.

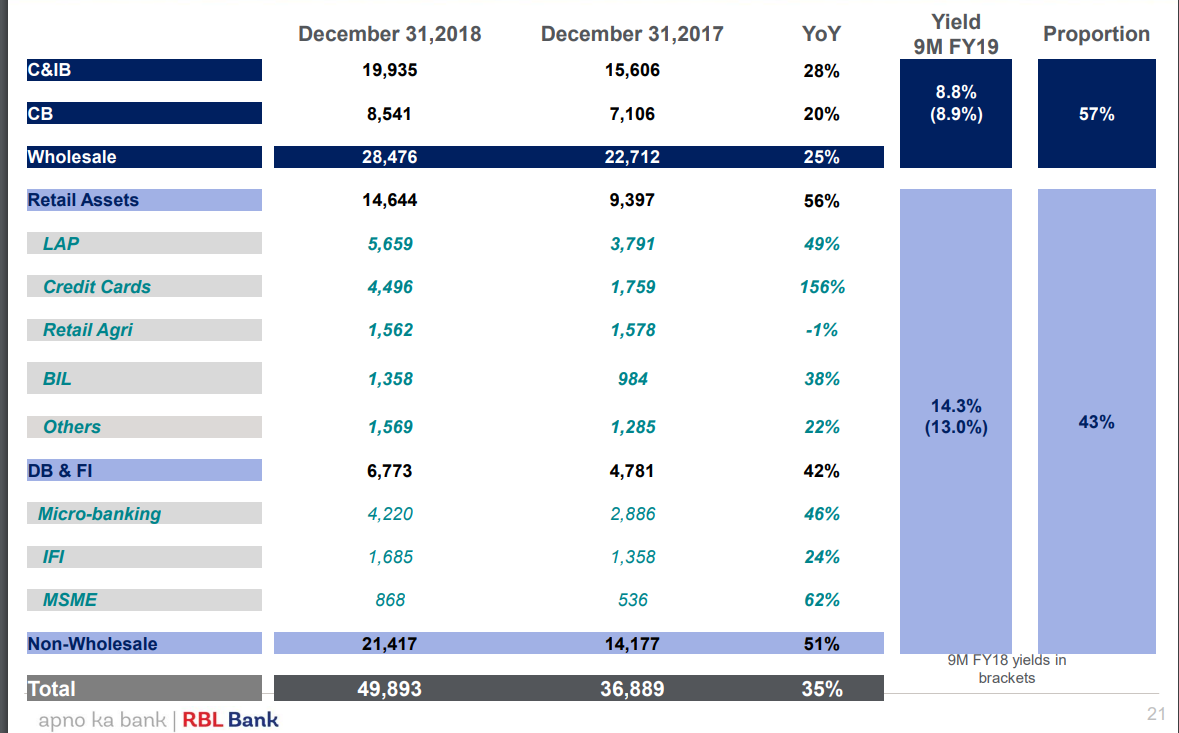

As one can see that yield on retail assets is 5%+ compared to wholesale assets. Out of the retail assets, only the credit card piece which I am comfortable/happy with. LAP + DB piece together forms 12,000Cr+ of retail assets. Although management claims LAP is against cash flows and GNPA ratios have remained low - I am still not comfortable with this. I would be interested to know the average duration of LAP loans and performance has to be looked across entire real estate cycle. There are far better opportunities if one really wanted to own the DB/MFI assets than RBL bank.

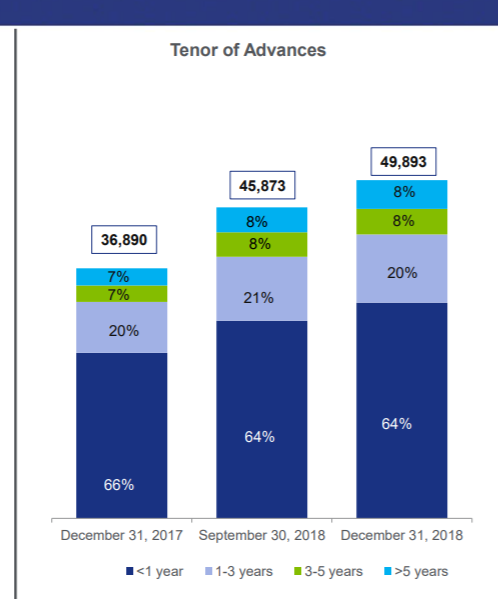

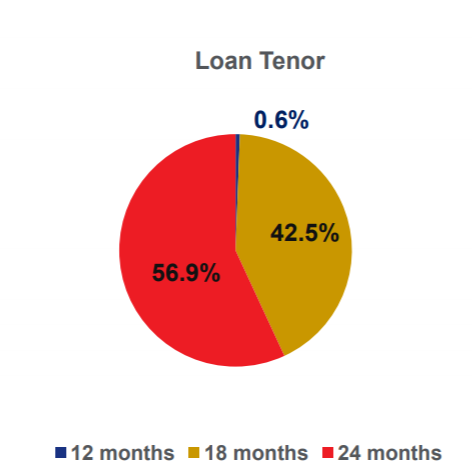

Further, 64% if the loan book has tenor of < 1 years which means majority of loans are working capital loans (which is good). But this also results in very limited pricing power for the bank and low yields on corporate side are a result of this.

Further 55%+ MFI book has loan duration of 24 months - which is a little bit on higher side.

So overall, the asset side things are average and a lot needs to be done to consistently generate more RoA, more spreads.

- One of the things that provides “anti fragility” in financing businesses is - no requirement to raise capital frequently. This allows for business to be shielded from stock performance and ability to dilute at highest possible multiple. This ability is primarily provided by high RoA.

RBL has never crossed RoA of 1.3% in last many years and RoE remains poor at 10-12% despite high leverage. With such low RoE and high growth rate of 30-35%, capital is depleting quite fast and RBL has to go to markets for dilution. This is why - I think financial companies with RoA of 1% vs. 2% vs. 3% vs. 4% have to be treated very differently.

That being said, capability to dilute at higher and higher price is also an important factor and Ahujas definitely seem to have this capability.

On positive side, entire networth of Ahujas is in RBL bank, GNPA ratios have remained quite decent with no adverse remarks from RBI so far, ability to scale thing also exists.

So RBL remains an interesting story to track but I am unable to make case for investment yet (despite very good rally in stock price ![]() ).

).

Disc - No investments as of now. Have bought and sold shares in 6 months as I was studying the stock. No transactions in last 60 days. Not a buy/sell reco.