This is behind paywall. Can you post a summary here? Interesting point to note is valuations are considered fair and not dirt cheap as we assumed.

Just visit this website

This website/author changes the view on Raymond Realty with every post

Started with calling it severely overvalued - made several basic calculation errors, arithmetic errors

Now the narrative is turned positive on their posts

At the bottom of it all is that the website is churning out posts focused on quantity than quality and often resorts to lazy AI summaries. Not a reliable source

4 Likes

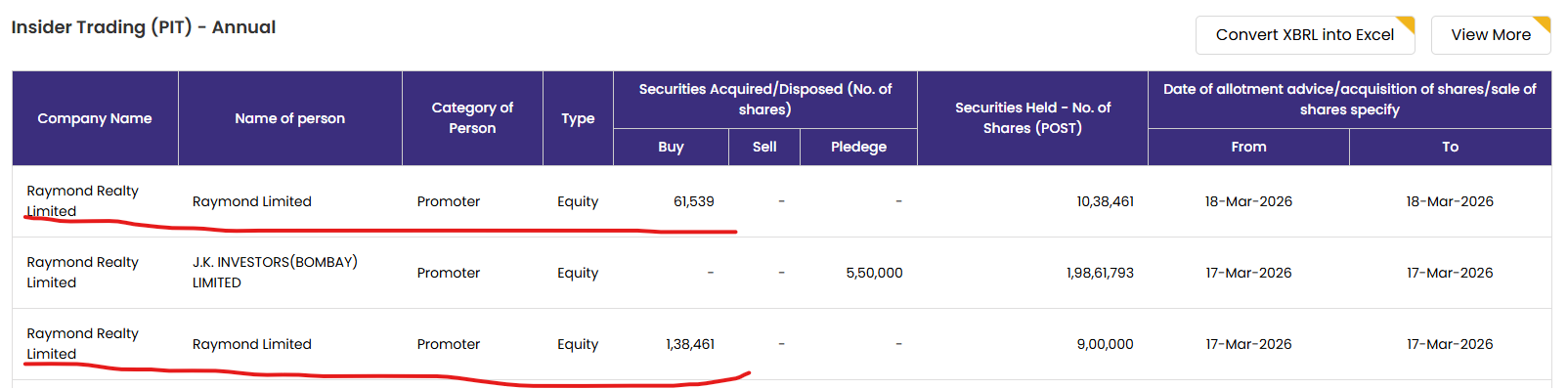

Turns out we’re not the only ones seeing the undervaluation

Raymond Limited has been buying up shares of Raymond Realty Limited

31 Dec 2025 - Purchased 1,00,000 RRL Shares

30 January 2026 - Purchased 7,00,000 RRL Shares

and now again

17th March 2026 - Purchased 1,38,461 shares

18th March 2026 - Purchased 61,539 shares

Promoter stake increased from 48.87% to 50.43% in the last 6 months

Promoter Holding is increasing steadily - Promoter buying is good - I like where this is headed

12 Likes

2 Likes

Looks like Gautam Singhania can’t catch a break.

One thing which goes in my mind these days is how much is too much promoter discount. Ultimately, everyone wants to make money here. Insiders continue to buy the scripe but do they wish to create value for everyone or just wants to acquire majority stake (>50%). This will be a good experience of investing in a company with promotor having red flags. A first for me!

Disc: bought more today and my top 5 holdings now

2 Likes

Forget about if he is involved in anything or not but Why does he need to indulge in these octane activities? He is now 60 years of age and his involvement in businesses is required far more than before with listing of subsidiaries. There is definitely a clear value at this price but its the promotor actions that market will keep evaluating from time to time irrespective of results.

1 Like

He is an adventures and Macho Man. ![]()

jokes aside Raymond Realty is 100% Professional management driven Company and Promoters does not engage in any day to day activities [ he himself said this in a TV interview]

has anyone got an idea of estimated sales of Wadala Project this quarter. that project is a maker or breaker for Annual pre-sales target of 2800 cr and Walking the talk will be important for Re-rating. Kailash Please if you have any insights…?

5 Likes

I eyed this : Promotor guided 2700 crs of Revenue where I am expecting Q4 as 1100 to 1300 crs revenue , last time he said OPM can be 15 / 16 % so PAT can be near to 200 crs. I see sales executives celebrate cakes on achieving numbers .

Achieved (9M FY26): ₹1,504 Crore.

Required in Q4 (Jan–Mar): ₹1,296 Crore.

The Q4 “Launch Stack”:

-

Wadala (The Address by GS): Estimated ₹700 Cr.

-

Sion JDA: Launched in March 2026; estimated contribution of ₹200–₹300 Cr.

-

Thane Inventory: Continued sales in TenX and Address GS Thane are expected to chip in the remaining ₹300–₹400 Cr.

post this we can see the stock re covering and one thing i see stock is falling from 900 and many might have booked loosed for Tax harvesting . I see all good with the stock and still things what are we all missing , leave the promotor name see the brand and run by professionals, I keep sending emails to the mangment have not received any thig yet if anything i will share.

If the April operational update confirms pre-sales of ₹1,200 Cr+, the narrative will shift from “falling knife” to “execution powerhouse.” The margin of safety at a ~₹2,500 Cr market cap against a ₹40k Cr pipeline is becoming hard to ignore.

Latest update was this sales team working very hard to close high number before FY.

4 Likes

Quite an unfortunate incident.

However as you rightly said - this is a professional management that’s running the business with direction from the board of directors.

1 Like

Recording from IIFL Global Investors Conference, gives a broader vision for all three businesses and also some history about group and restructuring that was done.

At 7:50 mentions that 50k sq feet sold in BKC project in a month and 100k sq feet is sold in Wadala Project, this event was from 24th to 26th February. The Wadala pre sales number till february then become 350 crores @ 35k per sqft. Ten X District 9 and retail launch of Park Street will also support pre sales this quarter.

On the downside, we can maybe see some slippage due to missing the Sion launch which was originally planned for mid february but hasn’t been launched yet.

7 Likes

I’ve always felt like Gautam Singhania after having worked on building Raymond since the 1990s has taken a back seat to focus on other pursuits in life that he’s passionate about

but this speech was a reminder that he’s still sharp as an entrepreneur and promoter. He’s learned to appoint the right people to run his business day-to-day, while also having conviction on the longer term strategy.

Great watch for anyone that wants to understand why this opportunity is attractive - explained by the man himself in straightforward and simple language.

On a side note, and this is a personal pet peeve - there’s no such thing as stupid questions, but if there were, it would go to a question asked by the attendee on AI taking away the work of financial consultants and as a result the Mumbai real estate market to crash. Just unbelievable lack of critical and second order thinking

4 Likes

A World Bank report highlighted that unlike previous waves of automation, AI has the potential to displace a range of non routine, white collar service sector jobs precisely the jobs India built its economy on.

Prolonged stagnation in entry level tech/finance hiring could soften demand in mid market areas like Thane and Navi Mumbai over a 5–10 year horizon, while premium and luxury segments remain resilient.

1 Like

Fyis and dyis both have reduced stake , so concern is there

100 cr at launch day before 31 march in Sion project so it will show up in this quarter Pre-sales numbers.

a rough and conservative calculation of pre-sales in this quarter.

wadala - 300 cr

tenx district - 200 cr

invictus by gs bkc- 200 cr

address by gs bandra - 150 cr

invictus+address in Thane - 150 cr

address by gs Sion - 100 cr

tennx ERA - 75 cr

park avenue thane - 50 cr

so pre-sales in this quarter should be in the range of 1150-1300 cr. [these are my personal estimates] so great performance given the fact that they got only 3 days for Sion for this quarter.

disc- invested, core holding [above estimates can be wrong, not a buy sell reco]

11 Likes

I don’t think pre sales from Sion would be reported in Q4 because management told they only report once registration is done and stamp duty is paid. Anyways, great execution by the management and sales team leaving aside slight timeline delays.

3 Likes

Pre sales for Q4 at 1519 crores. FY26 at 3023 crores, YoY growth of 31% (Guidance of 20%). Net Debt at 605 cr @ 9.60% avg cost of borrowing.

Mentions margin has also improved in Q4 and hence for the full FY (earlier updated guidance to 15.5 to 17% EBITDA margins for full year).

Management completely walking the talk, flawless execution on sales side. I remember one interview of CEO around BKC launch where he casually mentioned 3000 crores and sounded confident.

Now its upto the street to re-rate the stock (current market cap ~2700 crores).

8 Likes

I request multiple time to show the pre numbers alike other companies does. Finally we see these in today notifications. Management is very professional below is there reply.

10 Likes

They actually did it.

Wow. The stock may not be performing but my god has the management been delivering amazing results.

unless there is some serious issue that we haven’t uncovered like fraud, accounting misrepresentation, embezzlement- this is actually a wonderful business and a wonderful price

3 Likes

You were quite good with the estimates. Q4 presales came in at 1500cr. Fantastic call @Azhar_12

10 Likes