@Kailasa_Tiwari do you have any fair value assigned to raymond realty based on FY26 numbers and future growth outlook?

I attended the call and on the cash flow accrual , the speaker mentioned approx 400cr from thane and 200cr from other projects as a run rate right now. Might be useful for someone here

They have the roadmap to 600cr PAT by FY28

If you take a 20x PE multiple (industry average is at 25-35x) market cap would be 12,000cr, per share could be 1800

however I am looking at the 1200 per share as a decent value for the stock

However to caveat this: real estate developers are valued at P/NAV multiples. Calculating NAV is cumbersome without management inputs

so I’m working on building a detailed NAV model but it will take some time.

Rough back of the envelope math will also point to an NAV of around 1200

Very very rough math

Project surplus - 8500cr (launched projects)

Land bank - 40 acre at 40cr per acre - 1600cr

Asset value - 10,100 cr

Less: Net Debt - 656 cr

Net asset value - 9444 cr

Net asset value per share - 9444cr/6.65cr shares = ~1400

Take P/NAV of 0.8x (discount to NAV and lower than other listed developers) =0.8 x 1400 = ~1120 per share

13 Likes

Institutional Research Summary: Raymond Realty Limited (RAYMONDREL)

Date of Analysis: May 9, 2026 | Current Price (CMP): ₹635

Context: Following Q4FY26 results (₹1,519 Cr Pre-sales | 21.5% EBITDA Margins)

Key Brokerage Ratings & Price Targets

| Brokerage House | Rating | Target Price | Primary Research Thesis |

|---|---|---|---|

| Motilal Oswal (MOFSL) | BUY | ₹880 | Focus on FY27 Launches: Cites the upcoming ₹3,000 Cr Kandivali project and ₹1,700 Cr Mahim JDA as massive revenue triggers. |

| YES Securities | BUY | ₹860 | EBITDA Acceleration: Highlights the sharp margin recovery to 21.5% in Q4 and the successful transition to a 55% JDA (Asset-Light) sales mix. |

| JM Financial | ADD | ₹820 | NAV-Based Valuation: Values the demerged entity on a sum-of-parts basis, giving a premium to the 100-acre Thane land bank. |

| Emkay Global | NEUTRAL | ₹800 | Execution Watch: Remains cautious on the collection-to-sales gap but acknowledged the record Q4 pre-sales as a “pivotal” positive. |

| Morningstar (Quant) | Fair Value | ₹787 | Intrinsic Model: Uses DCF of existing projects to suggest the stock is still trading at a ~20% discount to its base intrinsic value. |

5 Likes

It will be good to understand why customer collections should lag, while there is much of front loaded cost (approvals, jd , initial construction, launch and other operating expenses), is it Rera regulations that prevent, or competitive land scape (so company is motivated to onboard customers with very little payment). If this continue with the pace they are launching JD projects, it might be difficult to maintain healthy balance sheet. What are regulation from Rera on collection side? from launch to handover? Are the regular construction phases front loaded too?

2 Likes

(post deleted by author)

1 Like

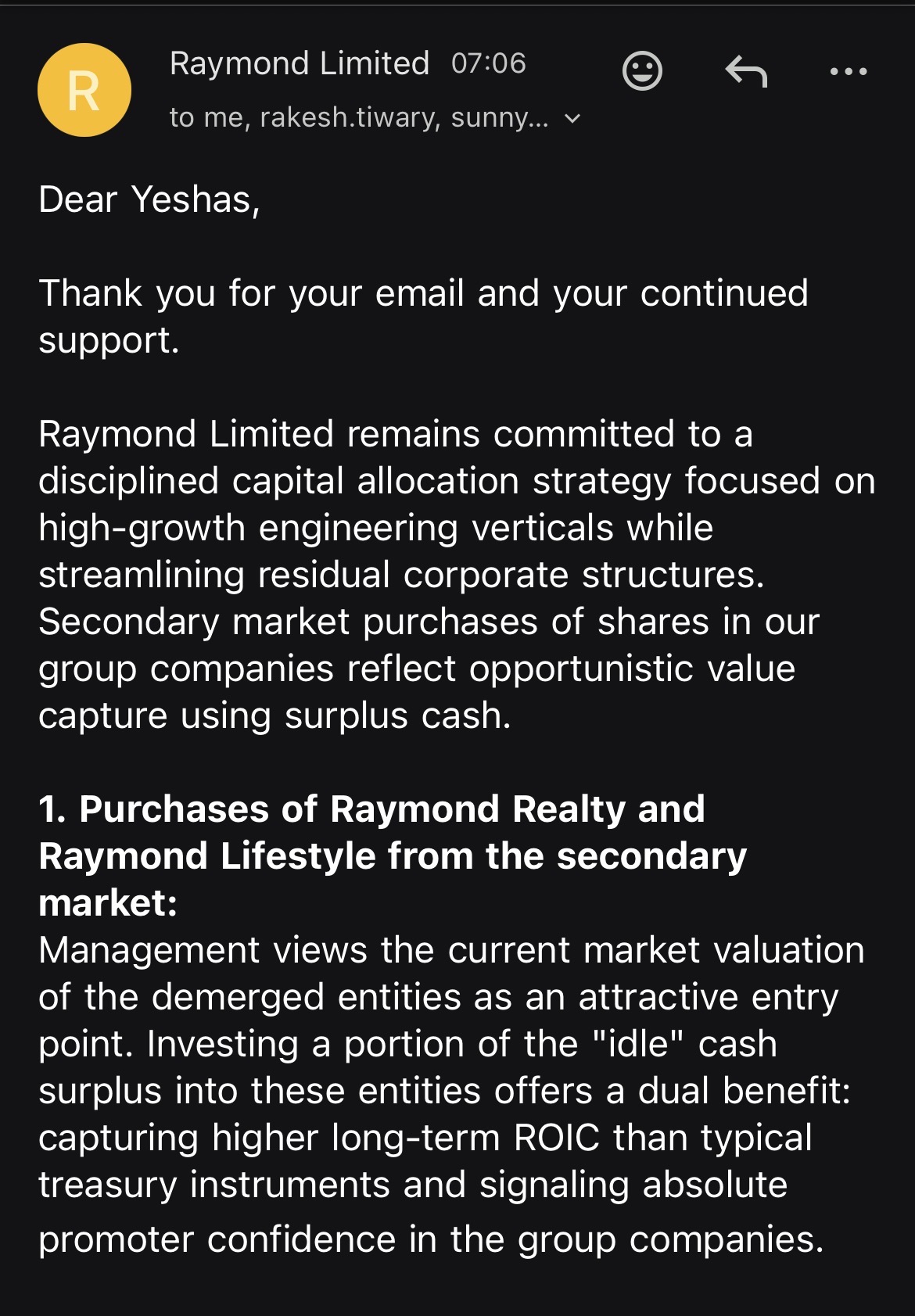

Here’s one of the clearest signals yet:

I asked Raymond Limited (promoter entity) why they are buying shares of Raymond Realty if they have their own capex plans of 200cr per year

My question:

Raymond Limited’s purchase of Raymond Realty shares in January and March 2026 was certainly a welcome move as I own shares in Raymond Realty and the promoter group signalling the confidence in the company.

However, I would like to understand the rationale of purchasing these shares (from what I can approximate at 35cr), while the company intends to spend 200cr a year on capex for the next 5 years.

From a capital allocation perspective, does the company believe that deploying capital to purchase Raymond Realty and Raymond Lifestyle from the secondary market at current prices present an attractive opportunity to earn a return on the cash higher than what may be generated by allocating it to the more near term capex requirements for the engineering business?

Raymond Limited response:

Meaning - they view Raymond realty to beat at least FD returns over the next 2-3 years

17 Likes

RRL Project list.xlsx (18.4 KB)

here you go

1 Like

quick new updates about RRL.

Positive - Raymond realty Growth engine - Address by GS Wadala [ Revenue potential of 5000 cr rs] is Selling like hot cakes i mean incredibly well and this particular project Success opens more gates for Raymond realty in other MMR region Premium Micro markets .

negative - Currently Thane is facing major Residential Oversupply concerns and the Residential property Momentum is Slowing down and intense competition among existing branded developers.

8 Likes

Some good insights on CASH COLLECTIONS

For the full year, a lot of retail investors panicked because the company’s pre-sales zoomed to a record ₹3,023 crore, but actual customer collections lagged behind at ₹1,725 crore, even dropping 9% compared to last year. This gap isn’t a red flag; it is just how real estate math works.

Raymond Realty uses construction-linked payment plans. When a buyer books a flat, the full value is immediately logged on paper as a sale, but the buyer does not pay all that cash up front. Instead, the cash is collected incrementally floor-by-floor. As the physical building slabs are cast on the ground, the company bills the clients, and roughly 80% of the flat’s total cash value flows into the bank account as the superstructure gets completed. Because Raymond launched a massive cluster of new projects in the second half of the year (like Wadala and Sion), their sales numbers exploded instantly, but the actual cash collections are trailing behind because construction is just starting.

The true safety net of this business is visible when you look at the total lifecycle of their launched inventory, which is worth ₹25,700 crore. Out of this entire pile, they have already collected ₹7,602 crore in hard cash from day one until now.

The most comforting number for investors is the ₹4,000 crore sitting in “pending collections”. This is legally locked-in, guaranteed cash from flats that the company has already sold but cannot pocket just yet because they are waiting to build the physical floors. On top of that, they have ₹14,098 crore worth of unsold inventory left to book. When you add the pending collections to the unsold inventory, Raymond has a total of ₹18,098 crore in future cash collections coming in from current projects. Since it will only cost them ₹9,573 crore to completely construct these towers, future collections minus construction costs leaves a massive net project surplus of ₹8,526 crore flowing into the bank over the project lifecycles.

This is exactly why the ₹589 crore civil construction contract awarded to Capacit’e Infraprojects for the Wadala project this week is a massive trigger for collections. By putting a top EPC contractor to work immediately, Raymond will cross those physical building slab milestones rapidly. This directly unlocks that ₹4,000 crore cushion of pending collections, turning locked-in paper receivables straight into flowing cash in the bank.

9 Likes

Thanks for details. How should one value the company based on this model?

1 Like

Here you go

2 Likes

vs a market cap of 3.9k cr

Its as if the market is putting 0 value on the land bank, and believes that Raymond Realty will not deliver the rest of the projects and will be distressed

I’ve seen several worse developers - 3 years delayed projects but still going along fine, launching new projects and get financing, whereas Raymond Realty delivers projects 2 years ahead of schedule and is still getting discounted

4 Likes