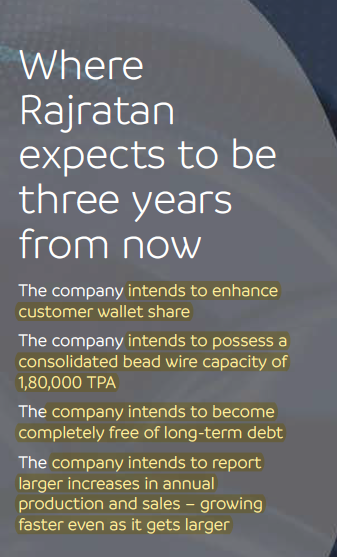

There is no Timeline or Guidance about this New Chennai Plant.

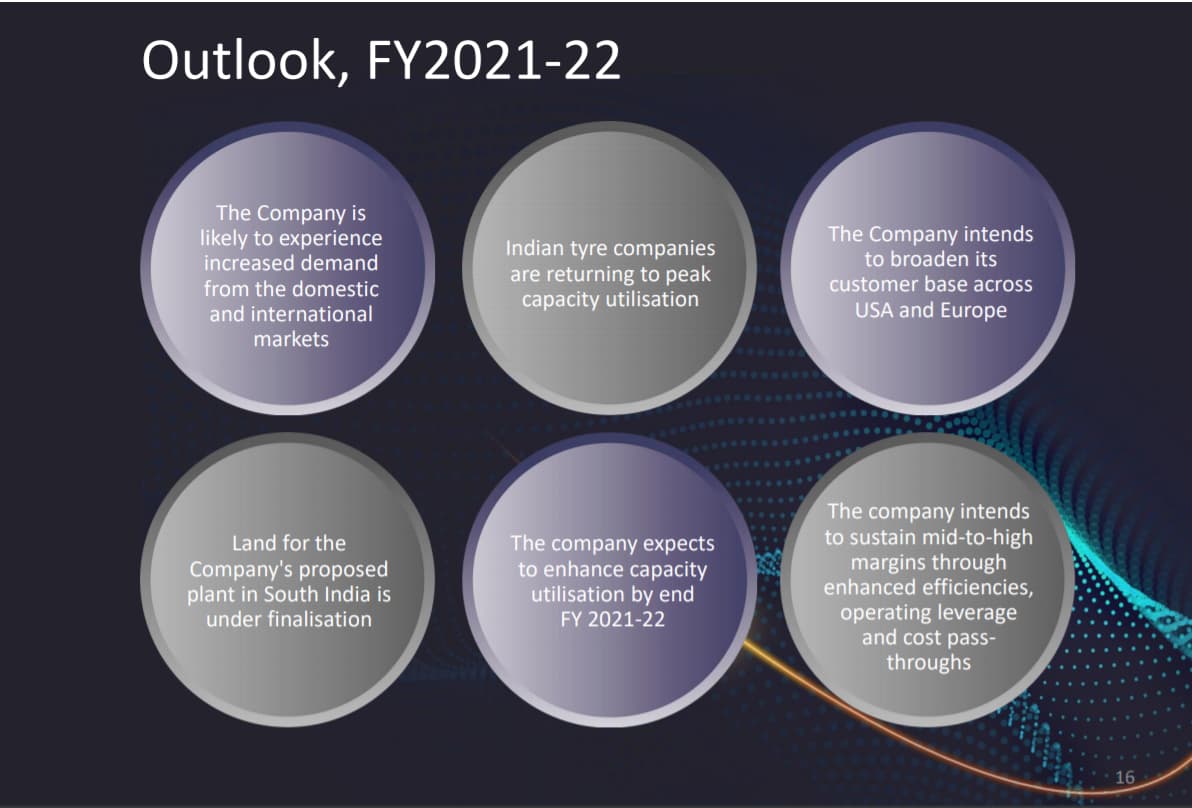

Since Auto is cyclic in Nature, the current demand may or May not sustain

being an ancillary company they may be in better position.

Invested around 350 levels and holding

There is no Timeline or Guidance about this New Chennai Plant.

Since Auto is cyclic in Nature, the current demand may or May not sustain

being an ancillary company they may be in better position.

Invested around 350 levels and holding

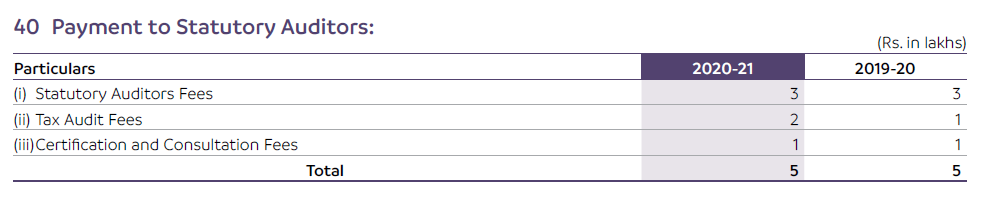

They pay 3 lacs for stat audit fees and a total of 5 lacs for the Indian co (topline of 120 crores and PAT of 48 crore). In 5 lacs what kind of auditing is this company doing i wonder?

The Chennai plant will come over the next three years. All capacity will not be available at one go they will piecemeal. They have just identified a land until now for the plant. In 3 years they expect total capacity to be 180k tons

1st point can be declared by the management at suitable timing…as the same is reiterated in fy 20-21 annual report…

About second point- even though auto sector is cyclical nature their ~70% revenue comes from replacement of tyres mostly commercial and buses…so it is comfort for investors about sustainable demand also they have retained their 83% of customers for more than 5 yrs.and most of them are expanding their numbers for catering to the increased demand/revival of auto demand.

Yes definitely they will be in better position after the expansion as most tyre makers are having their plants in Chengalpattu-Sriperumbudur industrial belt of Chennai which will be win win for tyre companies and rajratan.

For a company with 120 cr. of topline, auditor’s remuneration is not out of whack. For context, here are the sales numbers of Atul Auto and how auditor remuneration has varied over years.

| In crores | FY10 | FY11 | FY12 | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Auditor remuneration | 0.07 | 0.09 | 0.10 | 0.12 | 0.12 | 0.17 | 0.15 | 0.18 | 0.06 | 0.07 | 0.07 |

| Sales | 119.85 | 201.59 | 298.29 | 362.86 | 429.25 | 490.07 | 528.00 | 472.19 | 551.22 | 661.35 | 617.51 |

When Atul auto was a 120 cr. topline company in FY10 auditor remuneration was 7 lakhs and audit fees was only 3 lakhs (similar to Rajratan)

a different point but Atul changed their auditors in 2018 from Maharishi & Co to Kamelsh and Rathod. Could be possible that new auditors underquoted to win business which is why the audit fee drops or the new ICAI rule of not having the same auditors for more than 5 years or something.

I get the rationale for equating for low audit fee. I ran my fraud checklist points and i didn’t come up with significant accounting red flags for Rajratan.

I used to work in an auditing firm and I understand how much time it took us (as auditor) to get head around a biz. It involves time in understanding the biz process and workflow.

At 3-5 lacs involves at least 1-2 member team onsite. Mind you auditors also have limited reviews for four quarters + there is stuff like inventory counts + finalizing P&L and balance sheet. At any point it would be a 30-60 man day exercise. Also firms can’t run a biz with just one client paying them 5 lacs a year so you probably cut corners and hire below average resource which cost less.

Mind you here the company doesn’t break out money they pay auditors in consolidated financials so my hypothesis is a bit on shaky foundation as well.

From the AR -

‘’ the feared imposition of anti-dumping duty on tyres manufactured in Thailand from next year helped prepone exports to the US. ‘’

Can this be a risk for the Thai factory in the future?

Indian tyre market may be beneficiary of that

"The United States is our biggest automotive tyres market, and if they rule that we have to pay the anti-dumping duty they could switch to importing from our competitors, like Indonesia and India who are not yet subject to the anti-dumping duty,” he said. “The impact from the US decision could be either short or long-term, depending on their following moves. Domestic tyre manufacturers may have to look for alternative markets to make up for the loss of US orders.”

2025 is when it ends

Another strong quarter from Rajratan.Even compared to Q4,there is hardly any de-growth in revenues both in India ops and Thailand ops.This is even after multiple reports of auto slowdown & what not during wave 2.Operationally,there were labour issues again this time,dealerships were closed and so on.Company has been repeatedly saying that they have been having monthly stock-outs,volume offtake has been very strong since Q2.These results are a testament to the same & make me believe that the real demand is higher than the 180 cr. kind of revenue run-rate they are doing currently.

Disc.: Invested.Views are biased.

How can be get data of auditor remuneration and sales like this?

This can be another scenario. What if the audit fees for comparative year consists of other audit/consultation engagements such as adoption of IFRS 16, etc. Was the audit fee consistently reported s 5,00,000 and suddenly decreased to 3,00,000 ?

Is there anyways, we get breakup of audit fees?

It is totally dependent on tyre industry

When tyres companies will degrow it’s growth will slow

Folks - any info on why Rajratan has been in a free fall? There has been sellers circuit for past many days. And volume has been insanely low. Looks like not many buyers.

I recently invested at around 1700 and I have been skeptical of the company because of upper circuits, lower circuits as well low volume.

Fundamental looks good and this looks a monopolistic business but now I am not so sure.

Any advice from gurus here?

So nowadays because of so many robin hoods, most of the stocks are pumped like anything.

Also there are so many youtube channels and so called “experts” will recommend the same stocks in all the channels. Due to this greedy retails buy the stocks which will go beyond the valuation.

At the end, always “Earnings is the king”. So the smart people will book the profit at the top and greedy retails will be trapped.

Even I am tracking the stock and due to the valuation I didn’t buy this.

So I am assuming, it might get buying support at 1880 or 1620 levels.

Disclosure : Tracking and might enter with small quantities at the mentioned levels. Neither a financial advice nor a Financial advisor or an expert.

Great job sir. Can you please let me know what is the intrinsic value per share now-a-days ? Because it is trading at an all time high. Although this business has a high entry barriers one need to enter at the right valuations right?

It was available at around 1650 level before running up to 2700 with continuous upper circuit… you didn’t buy at 1650 level because valuation was high so how you are comfortable to enter at same level???

Stock goes from 200 level to 2700 level within one year… this can’t be done only because of so called ‘experts’ has given call on this stock. Please check the earning it has posted in last one year… Check out the expansion it has made recently. A company can’t be bad because it falls from 2700 level to 1800. Analyst are still bullish on this stock. Company has a good future with upcoming capex.

Dis: Invested from very low level. View are biased

I agree to your views that just rising price or falling price cant define whether the underlying business is good or bad. But such UC rise and LC falls clearly indicates either its too illiquid, operator driven or Robinhood investors getting in and out. This is extremely volatile and doesnot give investing confidence. Last year I saw Adani Green behaving like this.

Disc: Tracking but not invested.

I agree with these views as well.

Company appears really solid. Amazing results + appears to be monopolistic business with really good moat.

However, LC and UC does not inspire confidence. But I am willing to take risks.

I did entered earlier around 1700. Once this LC settles down for a day or two, I am going to buy more (same quantity) - whatever the price is (hopefully around 1700).