He might have got better opportunity elsewhere , but the thesis remains same, and due to interest rate hikes the growth is stalled by two years to compensate for the increase of interest payments.

4 Likes

I guess the reason why he is selling is when prices of aluminum, CPC, CTP OCP skyrocketed subsequently company posted best ever results in 2022 with highest ever Net profits and all but still the stock didn’t gave any meaningful returns like 2017 cycle I think market wasn’t rerating what Mr Pabhrai has assumed he might not be sure that what best could have happened than this so he is trying to take profits off the table. Also, I’m studying this business for a while all the triggers mentioned in above thread haven’t worked or if it have, The stock hasn’t rerated with that. I think the TAG of a “Commodity Company” and the “Debt” is the main reason why the stock isn’t performing or allowing it to rerate I personally believe that until the management takes on the charge to aggressively reduce the debt along with some triggers playing out as per the expectations, The stock will always remain undervalued or fairly valued. This might be thinking of MR. Market.

Disc- No holding till 18-1-24

4 Likes

Seems Like Mr. Pabrai is selling heavily, holding down from peak 9.99% to now 3.96% till today not sure if he further sells and take a complete exit, Usually when these big sharks take exits they know a lot more than a retail investor. Until the Picture gets clear to retail investor, it’s too late.

Stock is up 10% today but doesn’t influence me to see the business in a optimistic way than a rational way. However, I’m still studying this company quite deeply but trying to think of second order thinking, trying to play devil’s advocate.

Disc:- No holdings till date

To be honest, Monish Pabrai’s returns in India have been DISMAL to say the least. Every tom, dick & harry investor has beaten Pabrai between 2018 to 2024.

To me it seems like he has given up trying to go CONCENTRATED in India.

Initially be bought Repco, Kolte-Patil, Sunteck & Rain.

He sold Repco (Price shot up 2x)

he sold Kolte-Patil (Price went up 3x since)

He started Selling Rain around 150 (time will tell)

The biggest problem with RAIN is the DEBT LEVEL. MR MARKET is always scared of BANKRUPTCY levels and chances.

As soon as Jagan reduces the debt levels, we will see a definitive re-rating of this company. Until then, it’s anyone’s guess.

Technically speaking, the RAIN Chart is making Cup n Handle Formation. I add heavy positions around 150 after Pabrai Exited some. (Reverse Pabrai works)

5 Likes

he is closing his India funds due to SEBI rules plus he says India valuations are super hot. he is not able to find value.

1 Like

In which interview did he say that?

1 Like

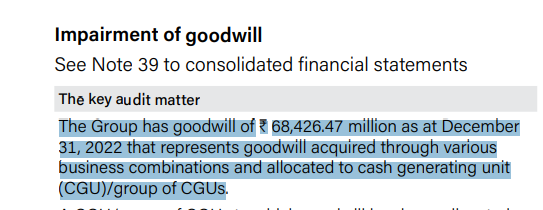

I was just checking balance sheet where I can see Goodwill as % to Networth (82%) is really very high, Any big headwinds in overseas business can result in Impairment of goodwill, this could be the reason of Low P/B, Mr. Market is quite smart to value the business mostly.

Any thoughts on this?

3 Likes

Pls can you share the snapshot of this for easy reference… I believe factories should be major part of networth.

1 Like

please find the attachment and let me know your thoughts.

Are they trying to create panic and give easy entry to HNI at lower levels?

Disclaimer - Very closely tracking & not invested

May be Pabrai want to reenter after tax loss harvesting, since in US they need to wait 30 days to do that… its my wild guess since the confidence he had on Jagan… however Pabrai has become more like a trader these days.

Disclaimer: Heavily invested and Rain makes 35% of my portfolio, but sold 25% of my rain holding at 185 today and not intended to sell further. My Buying avg now stands at 163.

3 Likes

Seems like they are trying to caution the investors (who have high expectations after peer companies results) to keep the rational expectations that is just after recent surge in stock prices also, one more thing I feel like is there are lot more headwinds and for a prolonged period than one is expecting at this moment, this might be the reason why Pabrai has sold his stakes.

Disc: recently added between 150-160 levels

Any specific reason that shook your thesis for the company? or what made you to book that profits, curious to know as you seem to be a hardcore “Rain industries” Investor. Curious to know your thoughts going forward

Due to interest rate hikes the last 2 year waiting for all investors here have gone to drain, its like a fresh start now. I have taken 25% out which is like I got an FD return on my investment of last 2 year. Pabrai kind investors are like stamp on ethics of owners. but since now he himself have sold 50% due to whatever reasons I took decision to shave off my holding by 25%.

2 Likes

Agreed! But don’t you think the prices has just taken the reversal and early sign of big bull run in this stock even fundamentals I believe the company has gone through a really rough patch, end of a long capex cycle due to all this company will be now forced to repay its debt in staggered manner as most capex has already been done, considering that most of cash flow then will be used to repay their debts also, once the debt level goes down meaningfully they could possibly think of listing their subsidiary in US exchange (as they will get a better valuations ONLY if debt is lower) which could potentially fuel in debt reduction even further as that is the only way of bringing the business back from this situation.

I may be biased as I just bought the stock right before the recent surge in the prices.

After the recent announcement by the management, I wonder if there is any impairment of goodwill in the cards in this year annual reports as goodwill as % to networth is very high (81-82%). so this can put more selling pressure on the stock in coming few days OR another way of looking to this is that Market has already priced in this factor/news/event by assigning a low PE/PB multiple to this company so it may not fall further.

market has already assumed this in last two quarters. unless the upcycle of this market happens, they may require at least 2+ years to make any meaningful debt reduction. capex cycle got over but capacity utilization must improve as I said earlier everything is linked to commercial production of ACP pellets which has higher margin. The downside risk is really less…

3 Likes

Pabrai might want to reenter but as far as i know the management, they would hardly care weather he exits completely or re-enters.

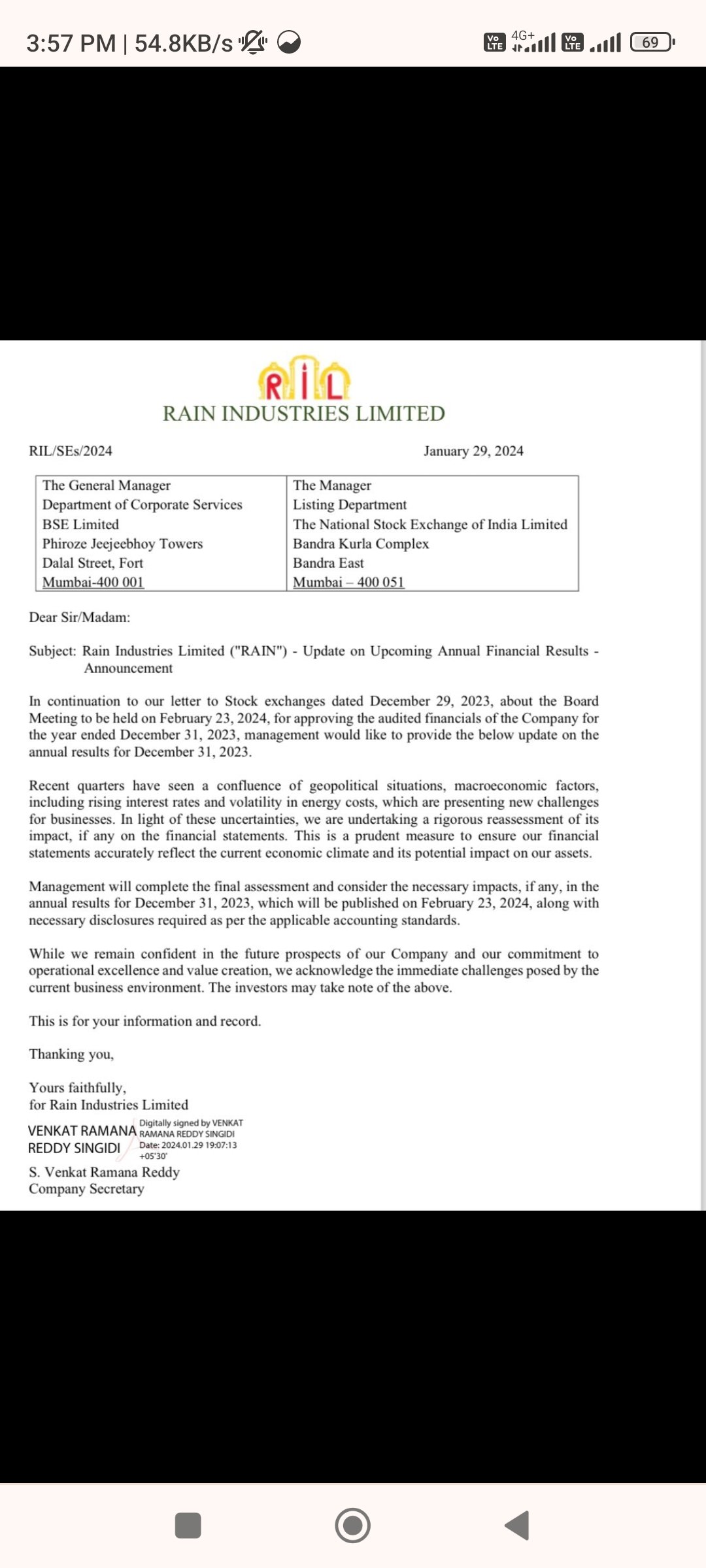

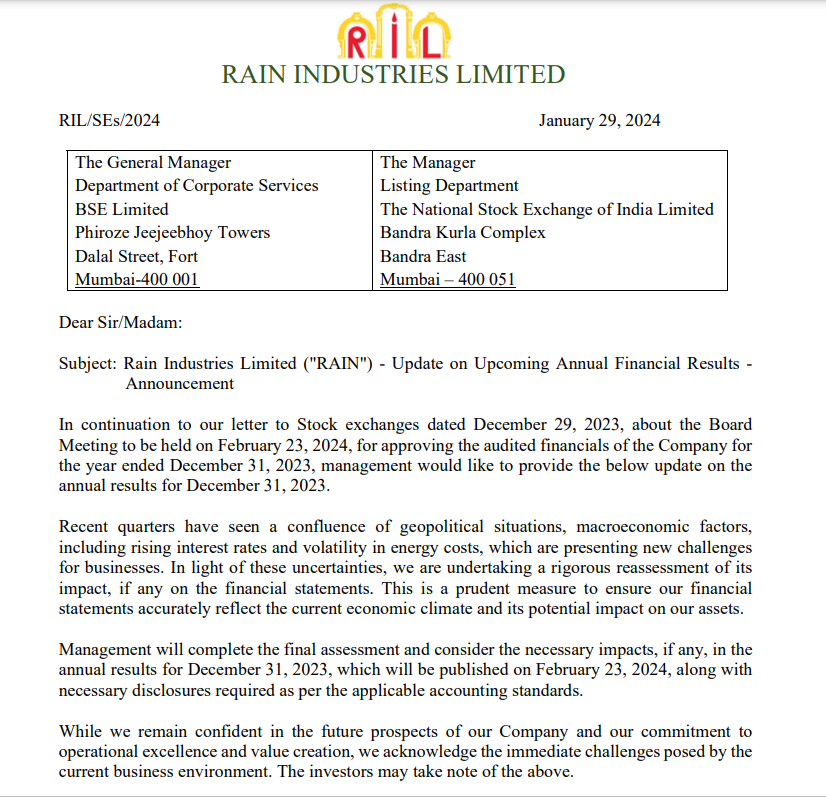

In the past also management had disclosed about the short term downturns in the business but this time the announcement looked vague.

I plan to remain invested and might add more around 156 levels , 142 levels, 125 levels, 97 levels.

4 Likes

Some fresh buying from these fund houses

Quant small cap fund : 0.13% of Fund

Icici Prudential multicap fund : 0.03% of fund

Source : https://twitter.com/Akhkr/status/1757031698129416423

Verified the same by checking the above funds current holding and month to month change in trendlyne

4 Likes