One of the key unknowns about this co is how the induction furnace route has been performing over the years. Whether the capacities are growing or not? Is induction furnace dying or growing?

Luckily. there seems to be an association for induction furnaces called:

https://www.aaiifa.org/

They publish a monthly newsletter. news letters are accessible here:

https://www.aaiifa.org/newsletter-2022.php

Few key takeaways from 2022 news letters that i read:

- Induction Furnace industry has been contributing very significantly in the overall production of steel in

the country, both in quantitative terms and as percentage of total steel production. - Crude steel production through induction Furnace route has been continuously increasing from about 4.3 MT (16%) to 22.6 MT (32%) in 2010-11 and finally to 33 MT (30%) in 2019-20.

- Contribution of the Induction Furnace sector is likely to be significant in years to come in making available quality steel at competitive price to the consumers in different geographical locations in

the country. - Since, it has a number of advantages such as low investment cost, land intensive as compared to

integrated steel producer, agility to produce various profiles of steel within a short time span, low operating Cost, providing greater opportunity of employment in rural areas to prevent unnecessary migration of people towards Metropolitan city etc., Moreover, the main advantage of the

induction furnace is a clean, energy-efficient and well-controllable melting process compared to

most other means of metal melting. Only air pollution occurs and no water or noise pollution

takes place in induction furnace, therefore, a special thrust is required to be given to look in to the barriers - Unlike other large steel producers, the Indian steel industry is also characterized by the presence of a large number of small and medium steel producers who utilize sponge iron, melting scrap and non-coking coal (EAF/IF route) for steelmaking. There are 285 sponge iron producers that use iron ore/ pellets and non-coking coal/gas providing feedstock for steel production; 39 electric arc furnaces & 858 induction furnaces that use sponge iron and/or melting scrap to produce semi-finished steel

- It is estimated that present demand for scrap is around 30MT which translates to roughly 20-25%

scrap usage overall. Since about 55% steel is produced through EAF and IF, this usage is low. The scrap usage is low due to no availability of quality scrap and high-power tariff because of which some

hot metal is used in EAF also. The scrap requirement as worked out is 65MT in 2030-31. This will work out to 22% scrap usage overall. Scrap arising within steel industry (domestic scrap) could be around 25MT. Hence, 40MT has to be made available through collection and recycling and imports.

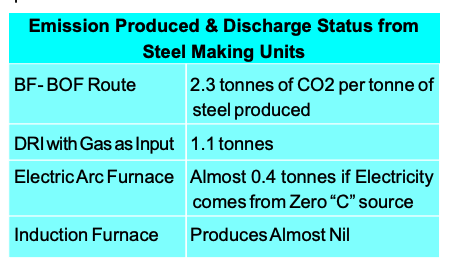

This clearly shows us the better environmental nature of IF & EAF steel making route.

8. The iron and steel industry is responsible for 11% of global carbon dioxide (CO2) emissions and will need to change rapidly to align with the world’s climate goals Steel production from induction furnace saves about 62% of the energy compared to the conventional steel making units significantly reducing carbon dioxide emissions.

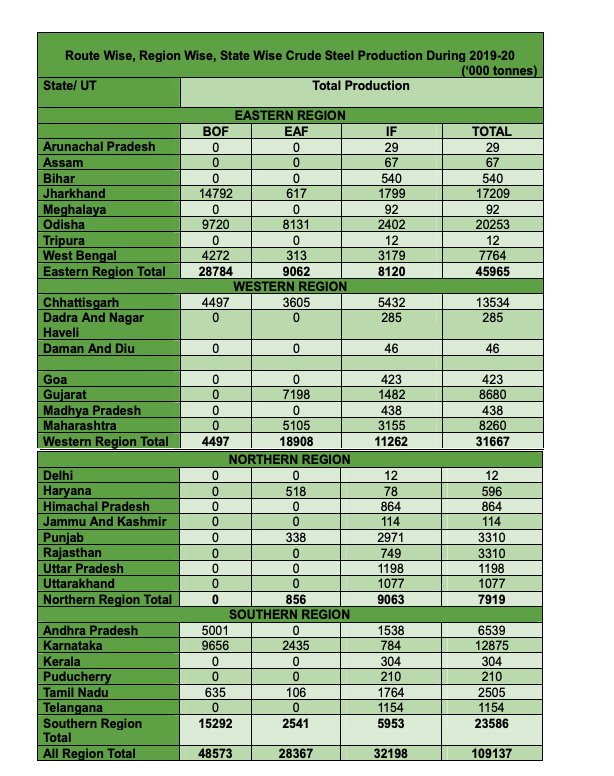

9. Detailed breakdown of IF steel production by region & state:

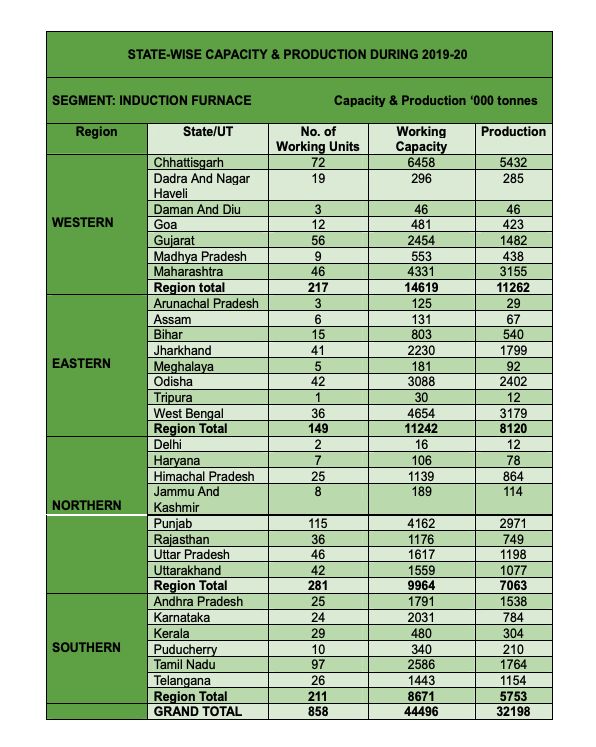

10. Detailed IF capacity utilisation:

Here are some other interesting stats from ficci steel report:

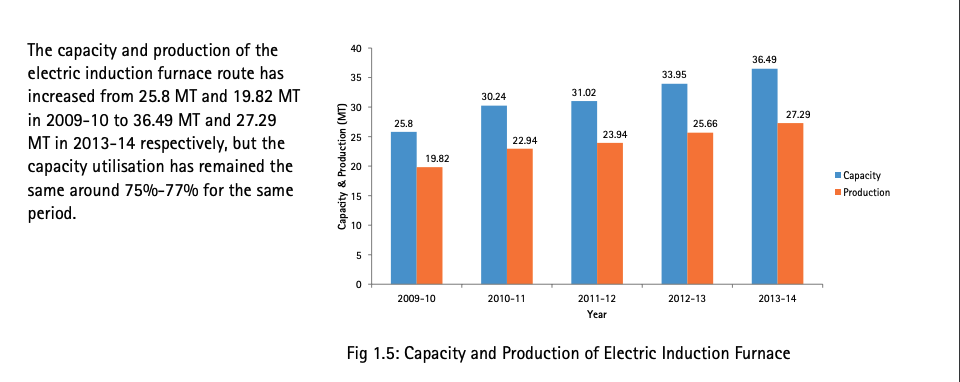

- Electric induction furnace capacity & production:

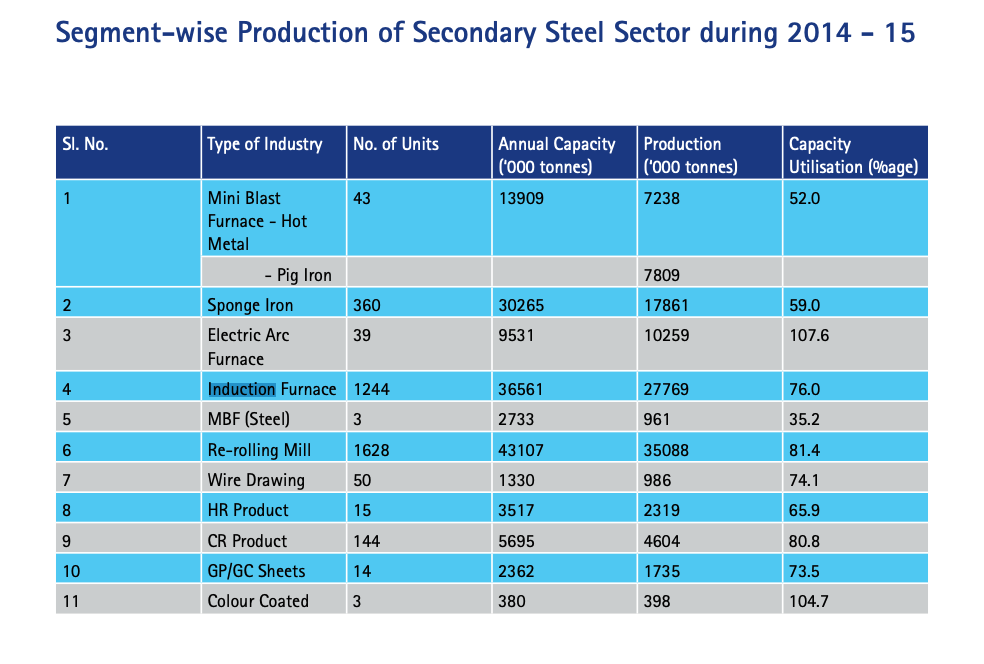

- capacity & production in FY15 (so that we can contrast with 2020 numbers in table above)

One can watch this 4 hour annual national conference of all indian induction furnace association as well if one is so inclined:

Disc: Invested, biased