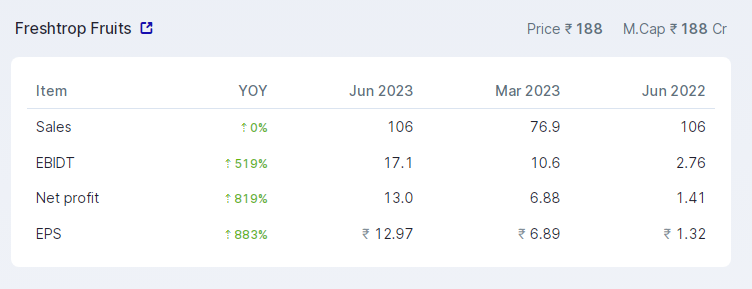

Yes, looks like margins have recovered strongly in Q4 and it seems co will have a good Q1 which their main quarter. Promoters have also increased their stake through company buybacks all the way during the downcycle.

3 Likes

thanks for the clarity

100% delivery volume over a month in this stock, can someone please explain what maybe the possibilities going on here, displaying such strange statistics. Is it accumulation by operators, good or bad scenario

The stock is in ESM-2. No intraday allowed. No margin allowed. You can buy only for delivery. Therefore, delivery will always be 100%.

1 Like

Thanks a lot for providing details and clarity ![]()

Very Interesting developement for this company…

-

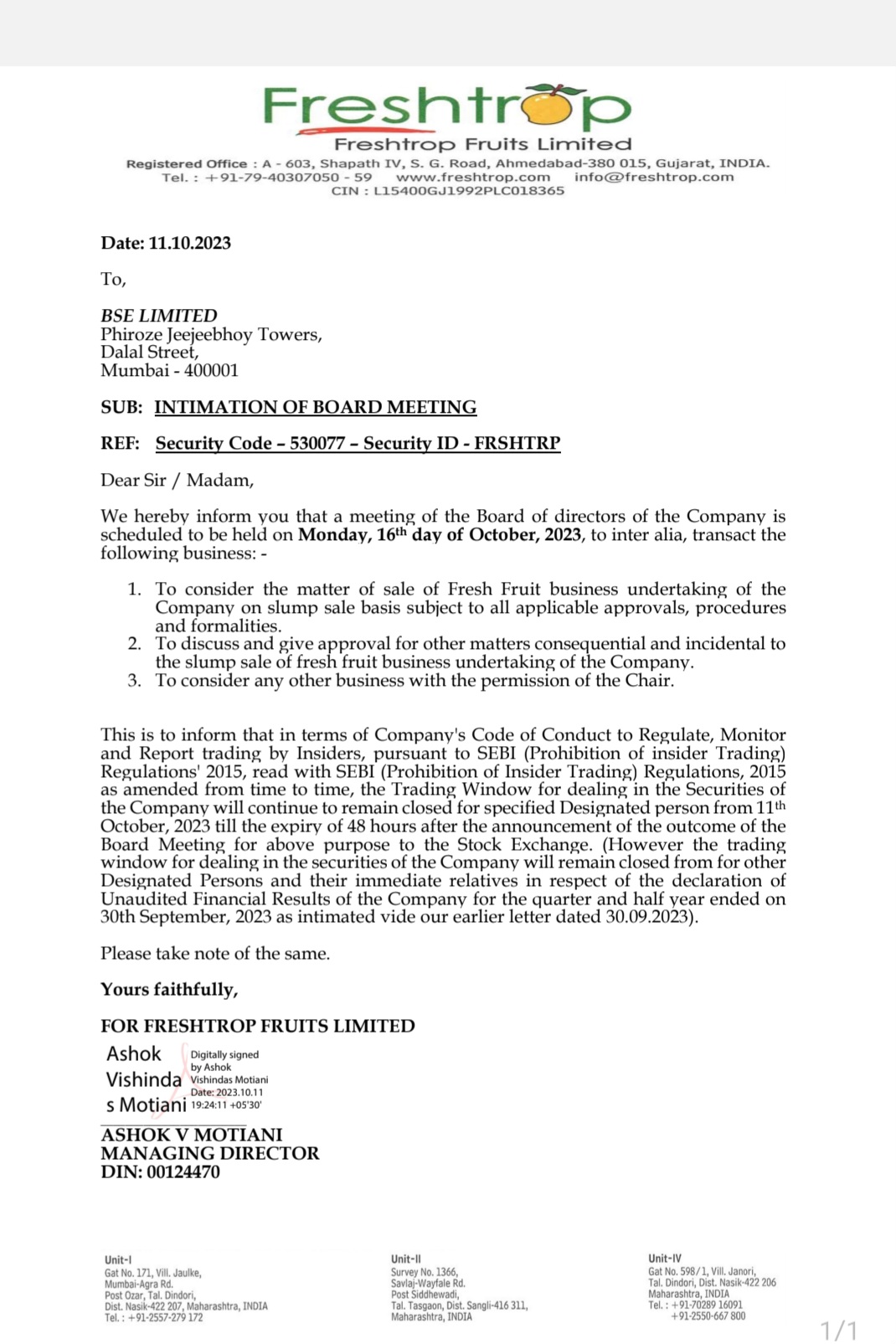

To consider sale of “FRESH FRUIT BUSINESS” on slump sale basis on 16th October…

-

To consider any other business…

Does Company want to focus on their food processing business??

( Last FY growth in food processing segment is 70% ).

Lets see how things pan out on 16th.

Disc: Invested from lower levels.

1 Like

Freshtrop Fruits

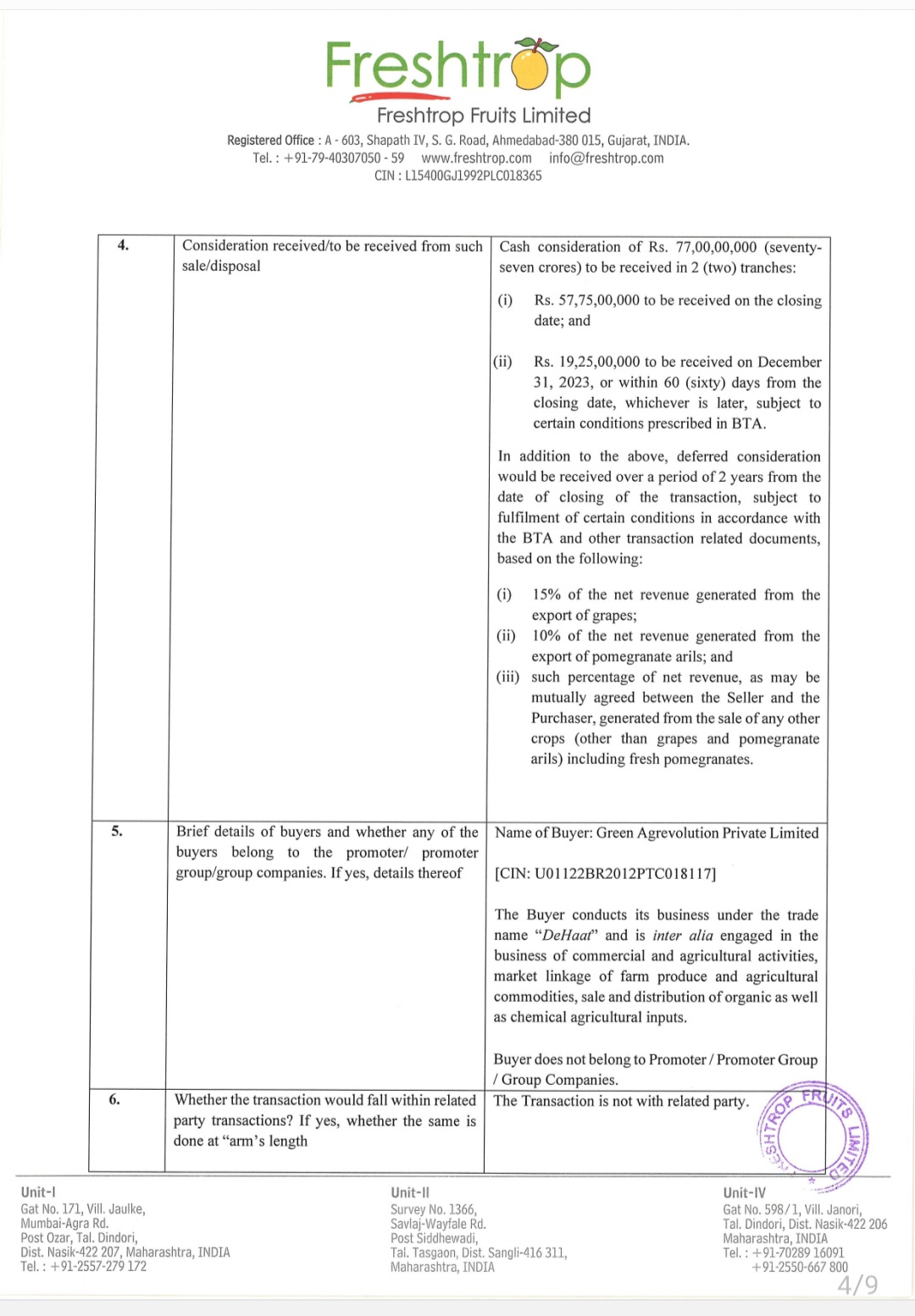

Sells fresh fruit business for 77 Cr + additional deferred consideration for 2 years

It will be used in investment of food processing business & return surplus funds to shareholders

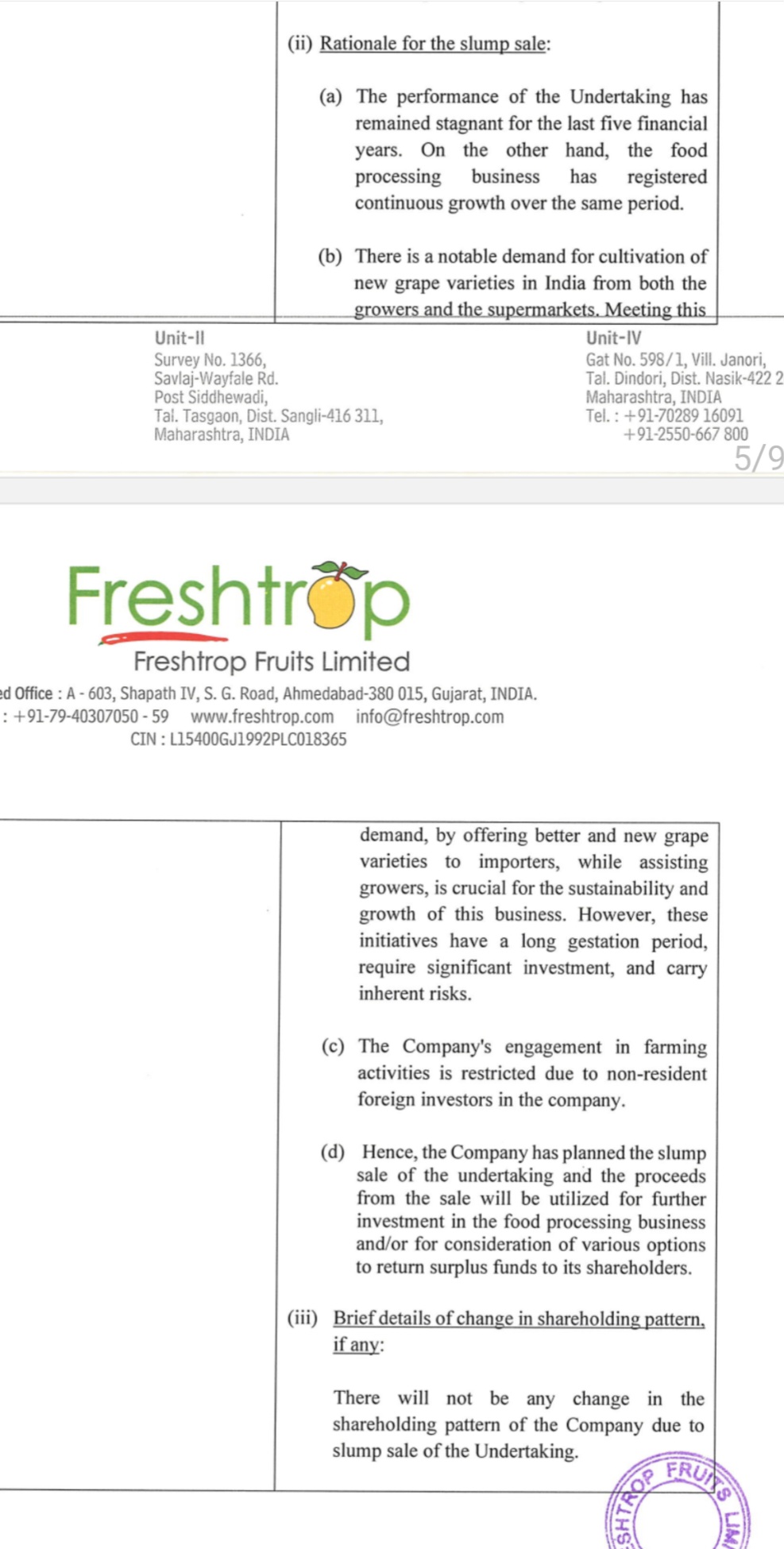

Reason for sell: No growth, high investment & long gestation period, restrictions in farming.

Sell valuation is not very encouraging in my view.

About 100 Cr. ( including deferred revenue ).

However, they sold it out of frustration of poor performance & restrictions and want to improve & focus on food processing business. - In my view, its a Good initiative for a long term growth plan.

Disc: Invested

1 Like

Time to change the forum name to Puretrop as the company got the name change approval

Also now with the discontinued operations of exporting raw fruits to Dehaat (known startup)

The company will be only making the Second Nature juices.

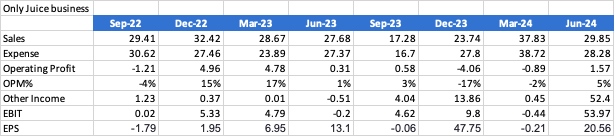

If one looks ar their juice business it is

- Started growing in last two years

- Profitable with decent margins in the June quarter

Only the juice business made 31 cr revenue with 1.7 cr EBIT last quarter, available at 122 cr Mcap - which 1:1 price to sales basis

Not a bad deal

Plus for two years they will get a percentage of raw fruits business that they sold which they will pass on through dividend route moat likely

The problem is OPM% for the juice business is very volatile

2 Likes

Updated the forum title according to name change - https://bsmedia.business-standard.com/_media/bs/data/announcements/bse/19102024/dbdd8944-89e0-45de-8021-c3a31a9f697d.pdf

- ROCE 10Yr 12.4 %

- ROCE 7Yr 8.63 %

- ROCE 5Yr 5.51 %

- ROCE 3Yr 2.94 %

- ROCE - 6.40 %

Why RoCE is Negative