Read the entire thread and found quiet a useful information about the company. Here is how I will value the company.

Lease rental business is earning a post tax profit of 28 Cr as per the quarterly standalone results. This can be capitalized at 7% giving a valuation of 400 Cr. Underlying land is valued at 588 Cr but I am not sure if this was a truly independent valuation. Lease rent is 44 Cr per year and that works out to be 0.75% of the value of the land. Considering prime location of the land, it appears to be low so I think the 588 Cr is on the higher side. It is reasonable to assume that lease rental business is worth 400 Cr or less.

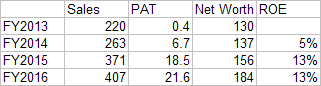

Current market cap of the company is 950 Cr so market is giving a valuation of 550 Cr to the hospital business. This is a 400 odd bed operation generating 400 Cr revenue and 22 Cr profit as of FY16.

ROE of the business is low and as pointed out @ayushmit, it may improve over the next 2-3 years. However, given the trend in the revenue, I think the hospital could be operating at a high occupancy rate so further utilization driven efficiency looks limited.

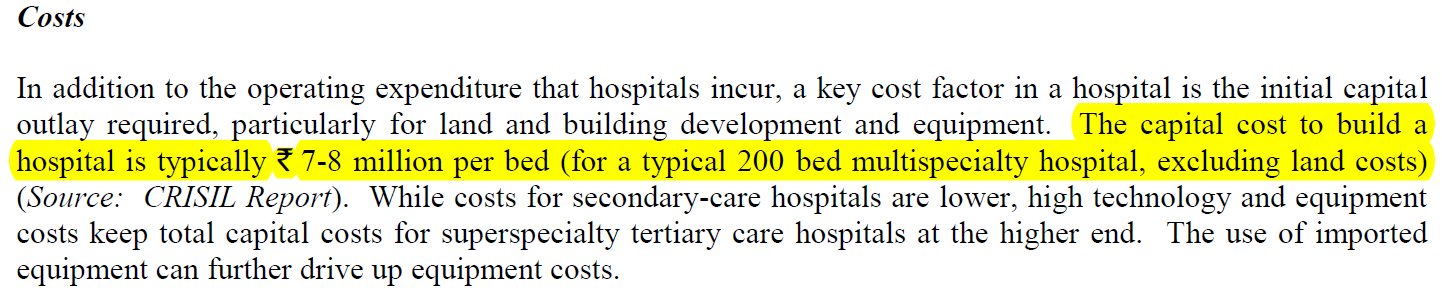

Market is assigning a valuation of 1.25 Cr per bed which looks fairly valued as cost of setting up a new hospital is in that range. Here is a text from Narayana Hrudayalaya IPO prospectus.

Kovai is also planning to set up a 300 bed hospital in Chennai for 300 Cr (including land cost). However this estimate is 3 year old so cost would have gone up now. This is an estimate for a metro similar to NCR/Gurgaon.

Regarding the expansion of 200 beds, I don’t see any capital work in progress so I think it is at a planning stage and not yet reflected in the balance sheet. Company is still paying down the debt so I don’t think they are planning for an immediate expansion. If anyone has some concrete information about the expansion plan please point out.

A 200 bed hospital will also need almost 200 Cr of funds. Given than company earns 22 Cr of PAT in FY2016, they won’t be able to do it without debt and additional equity.

company earns 400 Cr from 400 beds or about 1 Cr per bed per year. Assuming 85% occupancy, it works out to be 32k per day. I am not an expert but this looks a little on the higher side to me. Kovai is less than half of that in a non-metro location.

Given the low ROE and fair valuation I will give it a pass for now. Will wait for a sell off (if any) to enter. Moreover, I am really not interested in the lease rental business. I will rather buy the hospital business after it gets listed.

@Yogesh_s I agree with you -. Have been doing research on this and been contemplating an investment for a while. However I am not comfortable even at these valuations . Generally hospitals that are 5+ years old do EBITDA margin of 20%+, I struggle to understand the reasons for such low margins and how they will improve given the high occupancy rates already. I just feel that there isnt enough margin of safety right now to bet on just one hospital and governance risks here. Also this is a difficult sector which requires a lot of capital infusion continuously.

BTW IIAS report mentions 40cr for additional 200 beds.

Visited the hospital last week and after asking the staff got to know that they are planning 200 beds right now and those can be scaled up to 300 beds. Construction has started in the backyard where once parking space was given. I might be biased but the hospital seems to have recruited new doctors so that once the additional beds get installed the hospital may flow smoothly. Lots of new faces were there in doctors apart from the earlier ones.

Good to know that you are a doctor and your insights will surely help us make better decision.

My submission on the story is that the hospital is expanding it’s capacity in same premise…And the building being constructed is adjecent to existing building. They are giving waiting period to patients, for ex if you have to go for a joint replacement and you have consulted the doctor, he will advise for an operation and direct you to administrator where they will give you a probable date for the operation. Later on that probable date you will get admitted.

Now in such a situation, the hospital gets additional beds and they are equipped with capable staff, I feel the traditional 5-7 years of break even will not apply here.

Hi

I don’t know about this hospital occupancy. I can share my experience in kolkata. Fortis took more than 5 years to establish. And still can’t match apollo. Another hospital Columbia Asia took 8 years to break even. But now it’s minting money. One hospital iris is in total loss. NO occupancy… it depends on the area located. The sales team. Some hot shot doctor who brings in his own patients. But the hospital won’t benefit much from those doctors because doctors will take majority of the profit.

The second point is what facility will be provided in the new beds. ICU make the maximum profit. Depends on department. Rvu. Would be best for transplant and ortho.

The scheduling of the ot is more on doctors than on hospitals. Because most of the hospital ot are vacant in evening. But hot shot doctor may not want to operate in evening.

Medical tourism is going to explode in India, if we look at what Indian pharma companies have done with their cost structure, the hospitals are poised to do better with their even better cost structure.

As per results and board meeting outcome filing,

Lease income of PTL from Kochi land increased from 50 crore to 60 crore PA. With lower expenses and increased other income, Profit is 50% higher. Does any one know when artemis likely to be listed as it is already more than a month after the split.

Of much interest is the Management profile of (most probably Independent Directors on board)

Dr. Sanjay Baru

Dr. Sanjay Baru has doctorate in Economics from Jawaharlal Nehru University, New Delhi. He is director of Geo-economics and strategy at the International Institute of Strategic Studies (IISS), London and is a honorary Senior Fellow and member of Governing Board, Centre for Policy Research, New Delhi. In the past, Dr. Baru was the official spokesman and media advisor of the Prime minister of India and has also served as editor of the Business Standard, Chief Editor of the financial Express and as associate editor of the Economic Times and The Times of India.

Dr. Subbaraman Narayan

He has 4 decade of experience in public service in the state and central governments, in development administration. He was economic advisor to Prime Minister of India in 2003-04 and was responsible for implementation of economic policies of over 30 ministries