Regarding this i have asked AI to give me answer of the two question regarding how much percentage of the revenue come from fixed prices contract and how they are being fixed? for which i got these answers:

Privi has clearly stated in its earnings calls that the majority of its revenues are secured under fixed‐price, long‐term contracts rather than sold on the spot market. Across successive quarters in FY ’25, the company reported the following proportions of contract (i.e. “fixed”) versus spot/domestic revenues:

Q1 FY ’25: 65%–68% of revenues were contract‐based, with the remaining 32%–35% from the spot/domestic market (contracts cover fixed‐price supplies)

Q2 FY ’25: 65%–68% of revenues were contracted, 32%–35% spot/domestic.

Q3 FY ’25: Approximately 70% of revenues were contracted business, with 30% from spot/domestic sales.

Thus, roughly two-thirds of Privi’s revenues are “fixed” under longer‐term contracts, while about one-third is exposed to spot‐market pricing fluctuations.

Fixed-price contracts at Privi are negotiated once a year, on a calendar-year basis, directly with each major customer, and are structured as follows:

Annual negotiations in Q4 (typically October–December) set both selling prices and required volumes for the following calendar year under “fixed-price” contracts

Roughly 65%–70% of Privi’s volumes each year are sold under these contracts; the remaining 30%–35% is spot-market or short-term business.

Privi secures raw materials “back-to-back” for contracted volumes—i.e. it locks in feedstock costs at the same time it fixes selling prices, ensuring stability of gross margin.

Once agreed, contract prices do not change for the full year, regardless of spot-market movements, giving customers budget certainty and Privi predictable cash flow.

I am unable to understand that if raw material is back-to- back the need for 250-300 days of inventory. I thought it might be because they use waste as a rawmaterial, they need to store and use. But I am not convinced myself with this logic. Any thoughts please

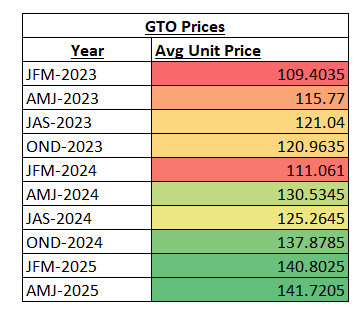

GTO prices have shown a clear upward trend from early 2024 onward.

Since GTO and CST prices are negatively correlated, rising GTO prices make CST relatively cheaper, improving cost advantage for CST-heavy producers like Privi.

5. Strategic Benefit to Privi

Lower raw material cost base (CST) + higher realisation from value-added products = margin expansion.

Rising GTO prices:

Hurt GTO-dependent competitors.

Benefit CST-based producers (Privi has ~70% CST share).

Growing share of specialties & new products in revenue mix shields margins from volatility in rosin/turpentine prices.

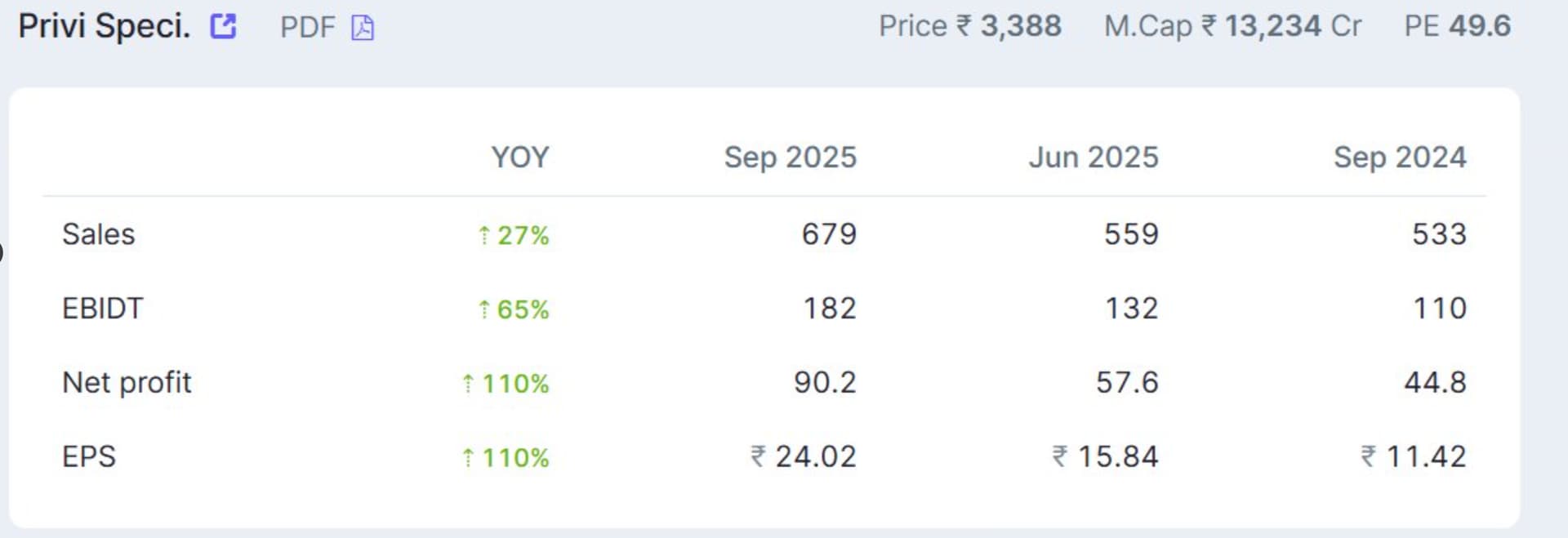

Shift to continuous production paying off. increase in CWIP in line with capex guidance and better absorption of power costs. Very strong and above guided margins.

Q2FY2026

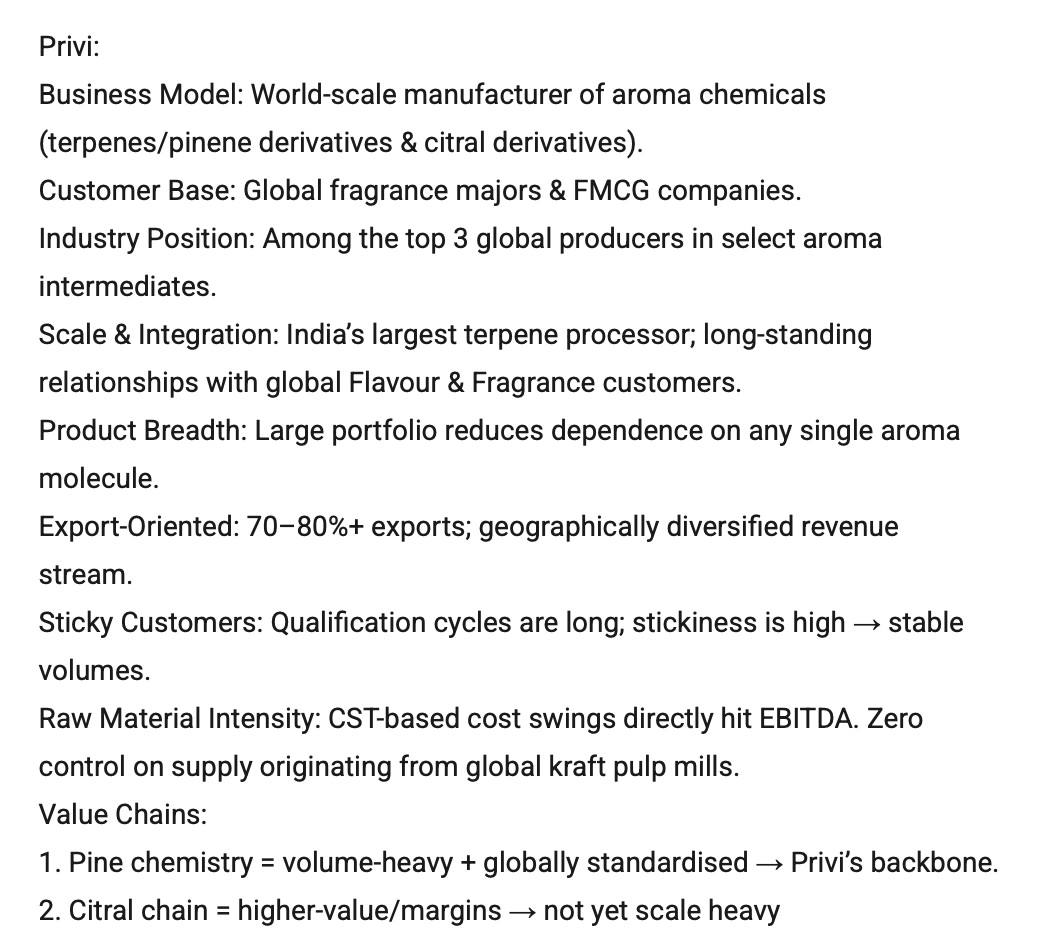

S H Kelkar and Privi Speciality seem to have gone on completely different trajectories.

In a rising input costs environment for aroma chemicals, Privi seems to have benefitted a lot from its backward integration for manufacturing of alpha and beta pinenes using by-products of paper industry.

They are at an advantage of 15-20% compared to players like S H Kelkar, Oriental Aromatics using GTO (gum turpentine oil).

S H Kelkar had guided earlier that their margins should improve from H2.