I am not a big fan of acquisitions, so it is just a relief that the market has taken a benign view of Pricol’s acquisition of Sundaram Auto Components Ltd.’s (SACL) injection moulding business. As has been captured in this thread earlier, SACL makes a wide hotchpotch of plastic products for TVS Motors and a bunch of other auto OEMs and Tier I suppliers. Its product profile is largely powertrain agnostic, with the company counting EV makers like Ather as one of its longtime customers. In the past, SACL also sold two wheelers for TVS – a trading business that was transferred to another group company in 2018 after the introduction of GST. Much before that, SACL was also into rubber parts but that business too was sold off.

Pricol will pay Rs.215 crore for a gross block of Rs.370 crore and a business which earned Rs.764 crore as revenue in FY24. SACL’s capacity utilization is not known but it has projected a growth of 10 % for FY25. This business earns about 30 % gross margins, roughly the same as Pricol’ existing business. SACL’s employee costs are also in line with Pricol, at around 11 % of revenues. So far, so good.

But despite this, SACL lags way behind Pricol in overall profitability.

The difference between Pricol’s existing business and SACL lies in the unit economics. Injection moulding is inherently a heavy fixed cost business and requires high volumes. SACL makes hundreds (perhaps, thousands) of heterogenous parts for a large number of customers. And it is spread thin across 6 manufacturing locations. All this leads to diseconomies of scale. At the net level therefore, SACL is hardly breaking even, with PBT margins of just about 3 % in the last two years.

Injection moulding requires tooling costs for each product produced, which can then be recovered only when significant volumes are generated. A new component will need a new mould to be made. And since making these involves no rocket science, vendors do not have bargaining power to demand better pricing. SACL claims it has also developed competency in the alternative technologies such as In-Mould Decoration (IMD), Physical Vapor Deposition (PVD) and so on. These might be higher value additive than basic injection moulding, but how much of the current business comes from such products is not known.

The primary raw material SACL uses is Acrylonitrile Butadiene Styrene (ABS), a polymer largely imported in the country though there are a couple of domestic manufacturers as well. The acquisition thus does not help Pricol reduce its import vulnerability. SACL has said it has a pass through on RM prices with a lag of a quarter with TVS, and I hope the arrangement is the same with other customers as well. The six widely dispersed plants are required in order to be closer to the customer, but create diseconomies in operational overheads. For example. Pricol spent Rs.24 crores on Power & Fuel in FY24 to earn a revenue of Rs.2272 crores but SACL’s power costs were Rs.25 crores for a revenue of just Rs.764 crore. Similarly, Pricol’s freight costs were 1.25 % of revenues while SACL’s spent more than double of that on freight.

With no scope of gross margin improvement and the necessity to maintain the six plants, what Pricol can do to improve margins (that TVS couldn’t) is a question I have.

Interestingly, despite TVS’s parentage and strong own growth, SACL’s sales to TVS have not grown, and I wonder why.

Moreover, Pricol’s press release does not mention any long-term supply agreement with TVS. I suppose given the existing relationship between Pricol and TVS, this business will at least remain where it is for the long term even if it doesn’t grow.

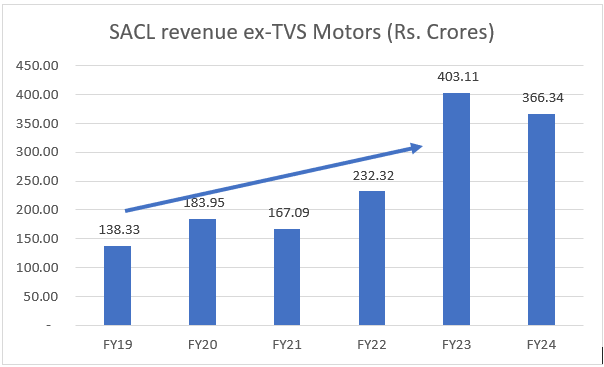

Thankfully, SACL’s third party sales have shown decent growth, growing at more than 20 % CAGR from Rs.138 crore in FY19 to Rs.366 crore in FY24.

The market has been cool to the acquisition. It not only adds to Pricol’s topline but gives it a wider geographical footprint and an entry point to a wide range of new customers. But to get the most out of it, Pricol will not only need to grow this business, but grow it more profitably. How it plans to do that remains to be understood.

(Disc.: Invested)