Sorry but I do not belong to this industry so have not used their products and as per their presentation they don’t have much market share in India and that their big revenue comes from export (Middle East nations esp.) probably that could be the reason that people in India are less aware of this brand

The big guy in the market is https://www.gcindiadental.com/ , they are the preferred supplier for dental products, a go to place for every dentist.

3 Likes

Concall Notes

Reasons for being in Jammu - Low power cost and low manpower cost. Its peaceful in Jammu and they did not face any violence in last 20 years except few one off instances. They get many other incentives from state and central govt (but did not specify specifically)

Tax rate - Earlier they paid 20% income tax due to 80IB benefits which are no longer applicable. So it will be 26% (25% + surcharge + )

USFDA approved products - 5 products approved and more in the pipeline. Through recent exhibition in Germany, they got in touch with many international marketing agencies out of which they shortlisted 3 for US. They have sent their products to these agencies and are undergoing customer evaluation, which may get complete by Mar 22. So any US exports would happen only in FY 23.

Revenue projections - FY 22 should be 40 Cr top line (they could do 17 Cr for first half even when first 2 months were in lockdown) So this year topline would grow by 30%. 100Cr revenue in 3-4 years with same ratio of 60:40 Exports to domestic. 20%+ annual growth expected for many years to come. Better prices in exports so better margins.

IPO proceeds utilization - Could not hear properly but their financial advisor mentioned something like 10Cr FA now which will become 16Cr . Asset turn of 2.48 would become 3.57 in next 2-3 years. They are investing heavily in brand promotion , marketing.

Quality - One analyst from Mumbai on the call mentioned that their channel checks with few dentists have provided negative feedback on product quality of the company. Mr. Mody said domestically they are focusing mainly on Tier 1 cities , they have best quality, best packaging, business is growing, nothing to worry. He said they can not satisfy each and every dentist and maybe those dentist did not know how to use their products so they are blaming the product quality (this answer was bit awkward and could have been answered better)

Mr Mody felt dental consumables is 1000-1500 Cr market dominated by MNCs and he is only Indian company manufacturing dental material is India having good product range and quality certifications. MNCs are all traders, they import and sell. On question of succession planning, he clarified that Niharika Mody is working alongside him and will take over at appropriate time. He also mentioned that he is adding lot of professionals in the company. Company is building new R&D centre and building is almost ready. He is hiring PhD in Chemistry etc. Currently company has applied for patent for 1 product. They send new products to dental colleges to test and get feedback

All in all, call was high on positive statements like we are growing 20%+, we are only Indian company in this area, we have good exports etc but was lacking details, specifics most of the times even when analysts asked for specifics. So we need to watch this company more carefully. It was heartening to see 300Cr market cap company putting up investor presentation and doing 1 hr+ concall which was well attended. I am ready to give benefit of doubt at this point in time but would be looking for more details in future. In the meantime, this forum can add more value by more scuttlebutt about their product quality which in my opinion is most important parameter for future growth and hence valuation.

Disclosure - not invested but on watchlist.

26 Likes

Thanks @Marathondreams for putting this summary.

Any comments from the management as to what strategies are in place to increase their market share (currently at 0.5%)? Just wondering, a 2 decade old company was able to manage only 0.5% market share in India. A bit surprising !!

1 Like

I have few questions if anyone has answers ( I attended the call but I didn’t get a chance to ask even after 60 minutes wait in the queue , I was simply listening )

-

What is the share of supplies directly to Institutes that they are tied up with vs Dealers / Hospitals (Since usage is high in the practical labs Academics usually look for non premium products , so understanding this will help us more )

-

Someone asked about the share of each region (South, North, East and West), there is no definite answer

-

Current market structure is dominated very few big distributors like GC dental . Their products on available on Amazon India and UK (Didn’t check other country sites ) along with they have their own ecommerce portal.

-

What is their product mix ? Which products are high value and low volume products

-

In the investor presentation they are doing capex to launch new products , if you look at them there is nothing new in them, gels , mouth wash etc…

-

From the scuttlebutt I understand most of the dental products are imported, I have seen many of them from Japan, did they ever consider to have technical collaboration with players outside of India to build the technical know how ?

-

Are these big suppliers like GC , I understand this company is a global player and they don’t make anything by themselves (this is the understanding I have so far, I may be wrong here ) , they import the products and sell them with their brand (white label )

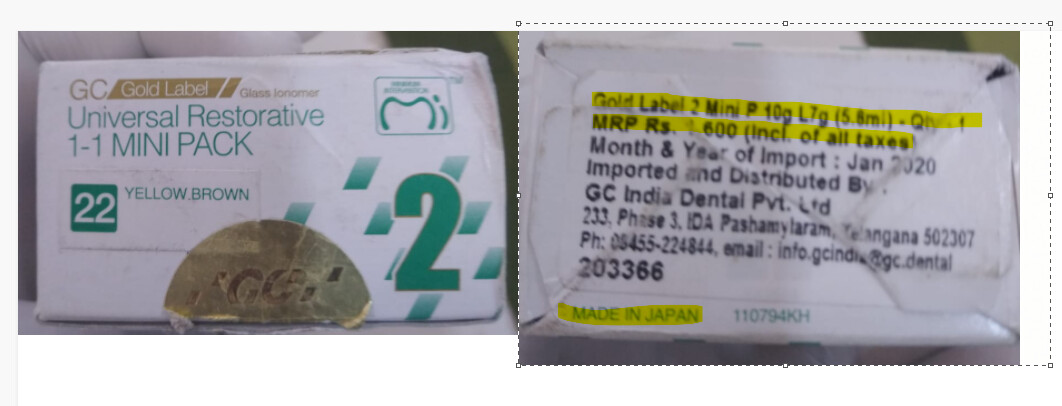

Few pictures shared by my Dentist friend

MRP is 1600 rupees, we have to see the equivalent product and compare the price and most importantly the quality .

-

Do they have tie-ups with big distributors like GC ? Did they find the shelf space with these big distributors who import and sell ?

-

Do they have any product influencers , come across this for their product, if it is paid one or someone just reviewing their product

-

Do they have any plans to expand into neighboring countries like Bangladesh, Nepal and Srilanka ?

-

Gross margins are to the north of 70% , why the material cost is so low ?

From DRHP :

Raw Materials: The main raw materials which are required by us to manufacture dental products includes Zinc Oxide, pumice powder, aluminium chloride, camphor, glycerine, paraffin, zirconium oxide, eugenol, diatomaceous earth, waxes etc. which are procured by us from domestic vendors. Further, certain of raw materials such as Aerosil, Bisphenol A Bis Propyl Ether, Ethoxylated

Bisphenol A Dimethacrylate, Triethylene Glycol Dimethacrylate, Urethane Dimethacrylate, Glass Powders, Sodium Alginate etc. are imported by us from international vendors located in Germany, USA, Korea and China.

9 Likes

Dental products are a highly fragmented market. On Dentalkart.com, I could count more than 100 brands. On prevestdirect.com, I could find more than 100 products listed by the company. In such a scenario,

- Prevest is the only company that manufactures these items in India, selling these products in India and 75 other countries, getting the toughest approvals from various authorities.

- They sell all their products in cash, with very high margin. This is happening for last many years, their sales growing at high rates for many years.

- They have been able to increase margin on higher sales.

Admittedly, it is a very small company and we cannot expect them to maintain detailed statistics product-wise/region-wise.

4 Likes

Can someone please share their investors Presentation as I was not able to find that.

Also, their reply on the question regarding negative feedback was not satisfactory. The way they said that they can’t satisfy each and every dentist leaves a negative image of the promoters. They should aim to have 100 % satisfaction and only then can get 70% satisfaction.

Also cannot deny that they have managed to get difficult approvals. However, I had good thought for the company, but sometimes it feels that the management is rather non chalant.

2 Likes

@rk1771 I am not really sure if they are the only company that manufactures these dental products in India? Randomly I googled and came across a manufacturer https://rident.in/, but could not get deeper to compare their products. May be you can investigate further and provide some insights. Thanks.

May be management meant to say that they are the only manufacturers for their products among the organised players in India? Not sure…

2 Likes

Found the IP

For others ready reference.

Disc: Analysing the company . Not invested yet. As of now very positive about the company but have some doubts with the management casual approaches.

3 Likes

when someone asked specifically, Mr Mody answered that they are the only Indian company manufacturing such wide range of dental material products and having requisite certifications to export. So there could be many small companies making only certain products or not having certifications…

1 Like

I do use a little but in non critical parts of treatment. Products do what they are supposed to but just not as well as ones from 3m or densply sirona. I should have also mentioned that there is a big market for cheaper products and not every patient(hence their dentist) can afford gold standard materials.

edit I am probably biased negatively from my use if their products

10 Likes

Thanks @Dr_Anuj_Mewada for first-hand information.

Of course many large brands are there in such products. They may even be of superior qualititavely.

However, we are examining a company having a 0.5% market share. They may not be present in more than 10% of the outlets. 90% of dentists may not be aware of them. It is understandable.

The best thing about the company is that they are able to sell their products at very good margins. Further, even on increasing sales, their margin is intact or even improving. If the products are not of good quality, margins cannot be maintained. Certainly, they have been able to create a good business.

This business has been created by a first-generation entrepreneur. Except for some exceptions, real wealth is created by first-generation entrepreneurs only.

In any business, first crore or first 10 crores is most difficult milestone. They are a 20 odd years old company. It took 15 years to reach 10 crores sales mark [11.47 Cr. topline in 2015-16]. Now they are reaching 40 crores in current financial year and talking of 100 crores in next 3-4 years.

As an investor, the real question is- can they sustain the momentum?

11 Likes

Thanks for the write-up,

I have few questions,

- Does management has a capable person to handle such a huge capex?

- How do they differentiate themselves from their competitors or What competitive advantages they have over competition?

Thanks

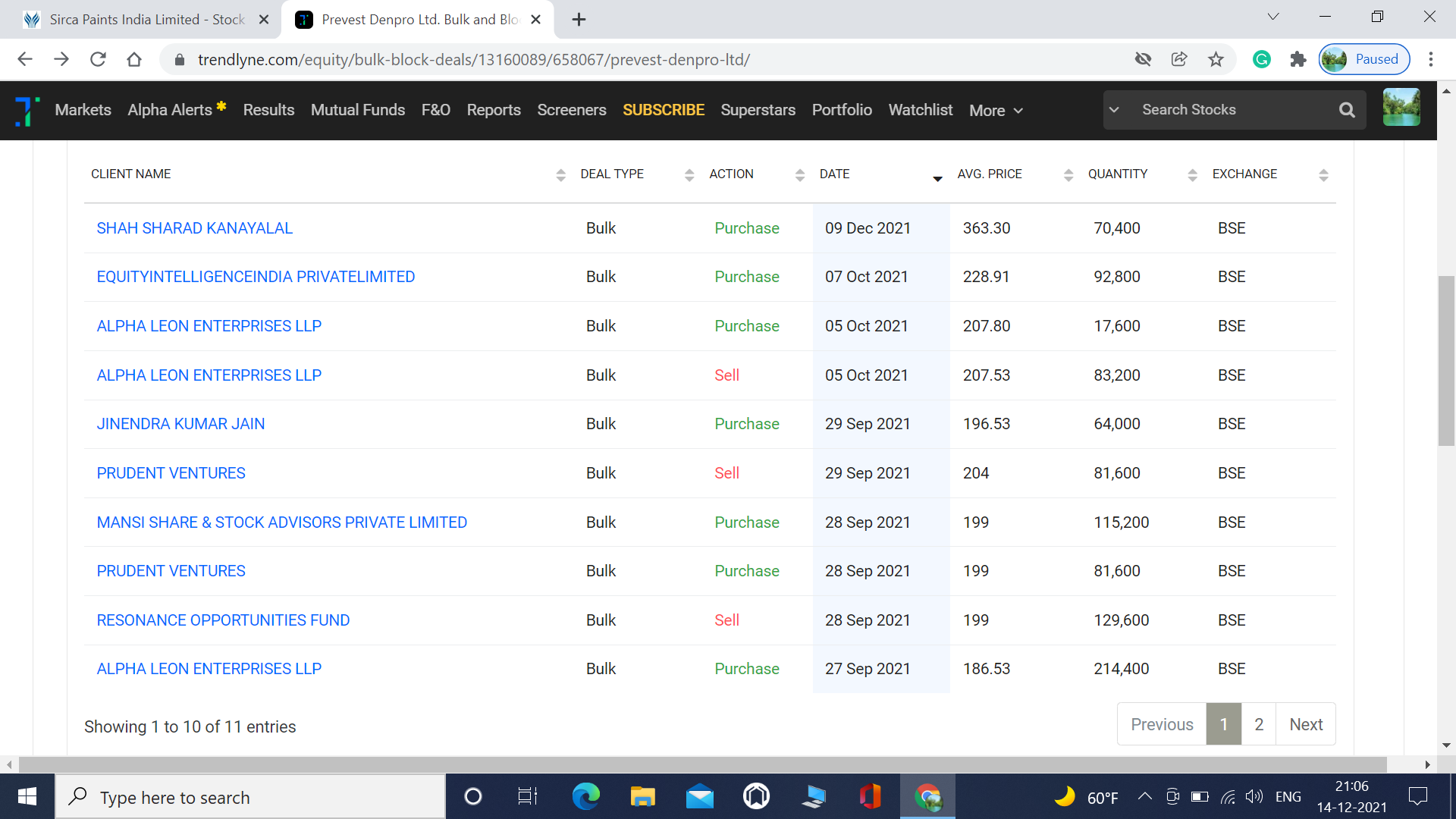

Som good bulk deals are happening on the counter. Though most of the bulk deals are trading, looks like Sharad Shah Kanayalal has taken a position.

4 Likes

The only advantage they have over competitors (MNCs) is the low cost of production, which will erode to a certain extent as the company scales up and sets manufacturing units in different parts of India/World.

In my opinion, currently, the company is having peak margins, which will soon normalize.

I am waiting for the company to provide a product-wise revenue breakdown, to confirm my thesis.

4 Likes

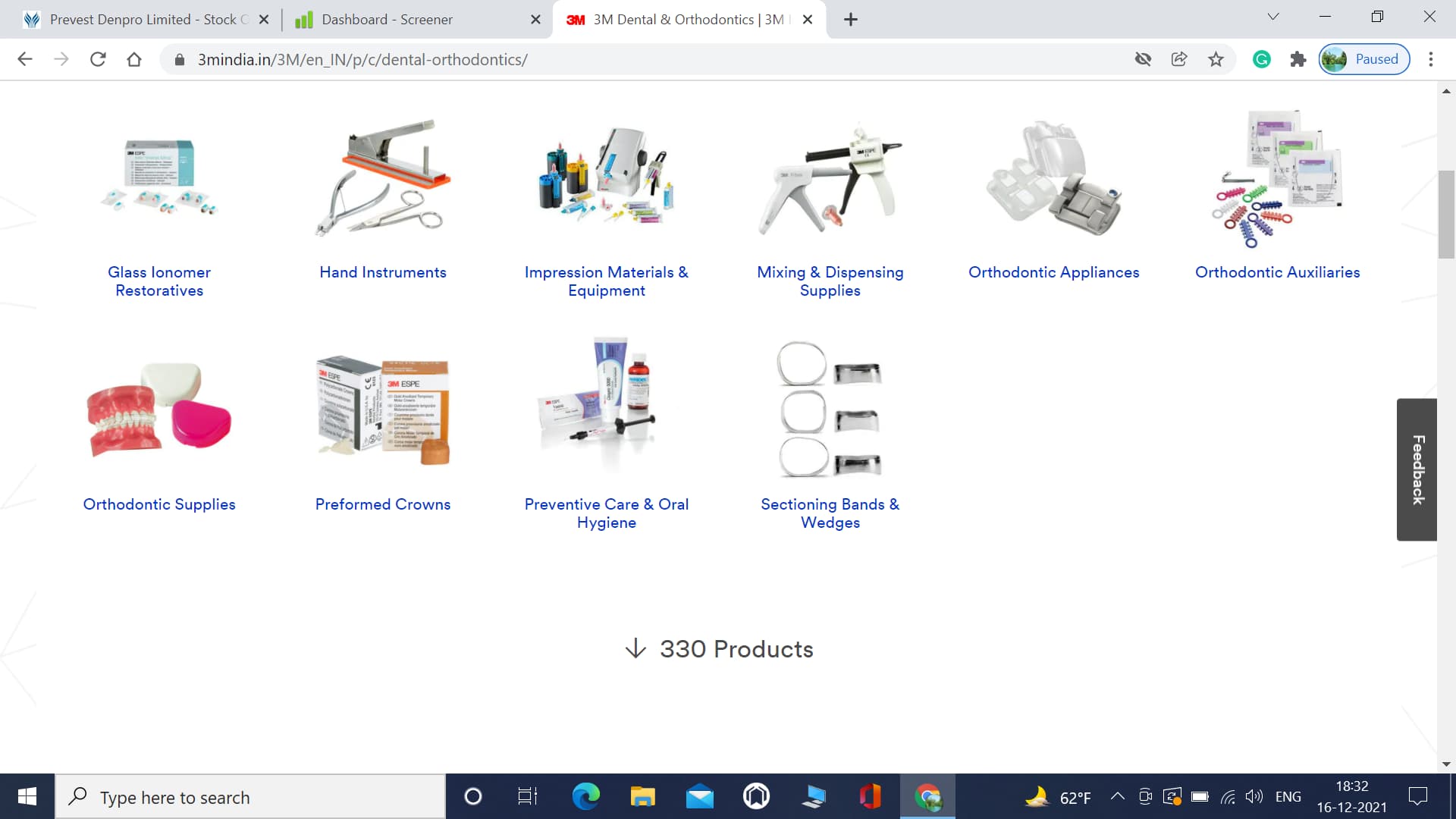

I think they can sustain the margin. The primary benefit is sheer number of products- it is more than 100. Every product has a small amount of sale, but in aggregate it becomes decent. The model is something like 3M model, where they sell numerous products with a decent margin. In fact 3M is also in dental products- 330 products are listed on 3M India website in this category.

As there are numerous products commanding small sales, high automation is not possible. This is the primary competitive advantage of the company.

10 Likes

Hi Rajesh,

If you look at 3M, Dentsply Sirona, and all the other major competitors, these are primarily dental equipment manufacturers who sell dental materials which makes a comparison to Prevest Denpro unfair.

My main question is that why does Prevest has only a 0.5% market share in the Indian dental materials industry when products from 3M and Dentsply Sirona are 2-3x pricier, even if we assume the quality of the products to be at par.

The only explanation I can give is that these MNCs have the opportunity to cross-sell materials through the sale of equipment and that dental materials as a portion of the total dental expense are not too significant, therefore pricing is irrelevant.

And I would make the argument that a company manufacturing good quality equipment and some materials have a vast and more significant offering rather than an only all dental materials manufacturer.

Also, the company has not given a product-wise revenue breakdown, so we can’t say for sure if sales are from a few products or equally distributed.

7 Likes

Am I grossly missing something here? A 2 decade old Indian company, with over 100 products, relatively cheaper compared to MNCs could not manage a market share of not more than 0.5%? Why dentists are not betting on their products?

How this will change ? say over a period of next 5 to 10 years as the company seems to be still majority managed by 2 Modis in terms of the growth strategy whilst the market is in tight grip of MNCs.

4 Likes

As a general rule of economics, demand reduces if price increases and vice versa. However, it may not happen if the product is sold on third-party suggestions. The pricier the product, the greater is the incentive of the third party to suggest the product. It happens in medicine, medical equipment, paint and hardware- products suggested by somebody but paid for by somebody else. Dental products fall in the same category, and it is easier for dentists to suggest pricier imported products with well-known brand names.

So, how does a lesser price will create an advantage? Well, not everybody can afford pricier products. With the passage of time, even the middle and lower-middle class have started using the services of dentists, who are forced to suggest cost-effective products as their clients cannot afford pricier products. Why do same medicines are sold at different prices? Because doctors understand the affordability of their clients.

Look at what happened in Stent market-

It is not that Indian stents were of inferior quality, or not substantially cheaper than imported products; still, Indian manufacturers were not able to sell the products. Reason- Moral hazard of third-party suggestion. So-called experts suggest products for their own benefit, even if it is pricier.

I am not suggesting that any price cap will come here, I have merely referred to the article to explain the point as to why they are not able to take market share even when their product is of similar quality and less pricy.

Their advantage is simple- services of dentists are no more availed only by rich and hence cost-effective products are required in the market. As more and more persons from less affluent sections of society will use dentists’ services, the market size of their product will keep on increasing. In fact, even in the export market including export to USA and EU; the market needs cost-effective products as not everybody in those countries is rich.

8 Likes

On first glance, it seems like a promising company with a bright future. However, if we have not done our home work properly in terms of understanding the business the current valuations do not provide much margin of safety for such a small business.

I attended the company’s concall on 1 Dec. While the information provided was good and gave some insights into the future growth, it was a strange concall where select few analysts got the opportunity to ask questions - hardly 7-8 analysts were allowed to ask questions over a 75 min call. I was in the question queue throughout and waa abruptly cut-off at the end. At the end of the call, I emailed the management some questions which were not answered on the call or seemed unclear to me - have not received any response in 15 days.

-

EBITDA margins of the company have grown exponentially from 13% in FY16 to 43% in H1FY22. What is the driver of such excellent margins for the company - is it very very low cost of operations, operating leverage with higher capacity utilization or high pricing power? As the revenues grow beyond 100 cr in next 3-4 years, what is the sustainable EBITDA margin over the long term?

-

I understand the company has received US FDA approval for 5 products. In the presentation, you’ve mentioned company has also applied for ISO 13485 (MDSAP Certification), which is essential to enter in the markets of USA ,Canada, Brazil and Australia. So specifically for US market - I don’t understand whether we can enter the market with the US FDA approval or we also need the MDSAP Certification?

-

On the call, it was mentioned FY22 revenue projection is approx. 40 crores and there were 2 months in H1FY22 which were washed out due to Covid lockdown so if I calculate on a monthly basis it’s almost 4cr+ per month of revenue. If I extrapolate that - in a normal year without Covid we could have done 50 cr revenue in FY22. Now this will be a 90% growth over last year FY21. If I look at the revenue growth in last 6 years since FY15, company has never had such high growth in any year (best growth of 20-30% over last 5-6 years). So what is driving such high growth for the company this year? Is it because of new innovative products? Also can you confirm if this 40 crore revenue will include any revenues from US market or US market revenues will only commence next year?

-

On the call it was also mentioned that you’re looking to professionalize the management and hire more professionals for senior positions. Is there any timeline you have in mind by when this exercise will be complete?

Disc: Exited after concall due to valuation concerns, now on watchlist till I have clarity on competitive advantage for such high margins and US market entry / growth.

24 Likes