Till date, growth of Praveg was mainly driven by vision and focused approach of Parasbhai. He was visionary and focused for the growth of the luxurious tent business of Praveg compared to Vishnu bhai. Dispute between Parasbhai and Vishnu Bhai started when Vishnu Bhai gone ahead for TV channel and other non-core business activities in spite of displeasure by Paras bhai and he decided to leave the company. Reason given by Vishnu bhai about Paras bhai’s health is not the correct reason!! Twenty years of Paras bhai’s effort might be destroyed by Vishnu bhai going ahead!!

Paras bhai is more focused on brand building and quality of tent business of Praveg. To know his attitude about the same can be seen here https://www.youtube.com/watch?v=x1Lfx1h2LKA

Paras bhai is down to earth and very honest person. He is not running behind money but more focused on ethics and self respects! (this video gives his life’s other part - https://www.youtube.com/watch?v=-svmtM2COAo)

Business update: Praveg Receives Work order for Developing and Operating

Kihim Tent City at Raigad, Maharashtra.

Maharashtra Tourism Development Corporation (MTDC) awarded work order to Praveg Limited.

• 40 eco-friendly luxury resorts with conference hall, restaurant & dining area, indoor & outdoor recreational activities, yoga and ayurvedic therapies, cultural center, medical room, etc. Resort is the first project of Praveg in Maharashtra.

• Contract is for five (5) years with an option to extend for another five (5) years

Please update the valuation metrics too. Thanks for the Google sheet. Very helpful

By the way, check today’s corporate announcement, there is amalgamation between Praveg and Eulogia Inn Pvt led.

Eulogia have 2 hotels in Gujarat. In Google map one hotel has good rating and reviews. Another one is relatively new (Grand Eulogia).

Update the sheet accordingly.

this transaction is bogus guys…Eulogia Inn revenue - INR 0?..Praveg newtworth - 139 cr…? thats it ? 1200 Cr market cap and you are exchanging valuation at 139 cr ?

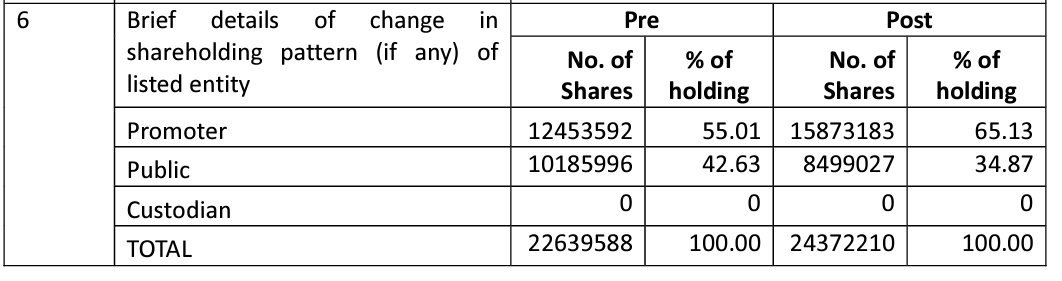

The promoters will magically increase their shareholding from 55.01% to 65.13% from this merger and all investors will be happy to see promoter buying shares😃.

They say it is not related party transaction, I have found only one connection between them.

“Praveg Adalaj Tourism Infrastructure Private Limited’s Corporate Identification Number is (CIN) U45202GJ2022PTC133994 and its registration number is 133994.Its Email address is cs@praveg.com and its registered address is 214, Athena Avenue Near Eulogia Hotel, Gota, Daskroi Ahmedabad Ahmedabad GJ 382481 IN.”

Is this Ethical way to increase the holding from merging Bogus business which is not having any revenue and then sell those share in the open market and look for another bogus business to merge?

If these are management strategy, then we need to be very careful with the business and does not looked to be long term bets.

Happy Investing,

Karthik

Disclosure: Not having any exposure to this counter. Tracking this counter due to high ROCE and also can see short term appreciation from ram mandir Ayodhya opening.

Excatly. That amalgamation notice looks completely bonkers. Revenue of Praveg is 14.9 crores and valuation ~130 crores. Both these numbers are ridiculous. I would like to know what were the board members hooked on when signing that contract. Is there a way I can complain to SEBI. The minority shareholders are being robbed in daylight.

I am still trying to understand the transaction but here are my two cents. The Net worth is not representing ‘Market cap’ but the ‘Book value’ of the company. But I don’t think it makes any difference in this deal. Important point to note is the change in equity holding-

While Promoter holding has gone up by 33 lakh shares, interesting thing is that Public shareholding has gone down by 17 lakh shares too. As per my limited understanding, it should only happen if ‘Transferor’ company already had some shares of Praveg and they are now moved under ‘Promoter’ fold.

In addition, another 17 lakh shares are issued (2.43 cr post against 2.26 cr pre) which translate to an equity dilution worth roughly 90 crores at CMP of 550 INR per share. Based on remarks made by other members, I believe this is the amount Praveg is paying to the ‘Transferor’ company for buying the two properties that they own. The price paid may be high or fair depending on the property size and its location and one may say that (may be) the Promoter made extra profit in the transaction.

I don’t know yet if it is bad corporate governance case though, but it looks like company has not explained the deal in detail and that raises some doubts. But as we know with most small caps, they are not very good in explaining things to shareholders so I am willing to wait for more clarity to emerge.

Exactly my thoughts. Though it is unfortunate that Praveg didn’t communicate well regarding this deal, I would not jump to conclusion that it is a fraudulent management, like some members did in the comments above.

Maybe just biased because I am invested, 11% of my PF.