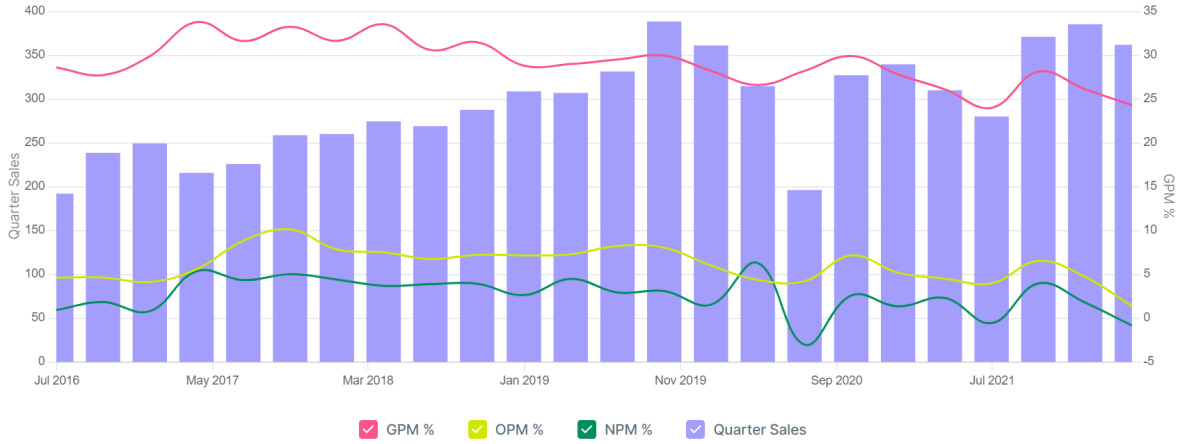

Investing Rationale: The company seems to be extremely undervalued at present price, with the key headwinds of palm oil price and packaging price going away and growth coming back due to reopening of schools. The company can easily have 9% EBITDA margin as it did in FY 18. It becomes more easier with the cost cutting initiatives taken by the company.

My Valuation: So assuming by FY23 company has a revenue of 1500 cr (which assumes a very little growth though company achived high teen growth historically) & 9% EBITDA Margin having an EBITDA of 135 cr by FY 23.

Bear Case Price: 1350 (FY23 EV/EBITDA of 10),

Base Case: 2700 (FY23 EV/EBITDA of 20),

Bull Case: 4050 (FY23 EV/EBITDA of 30)

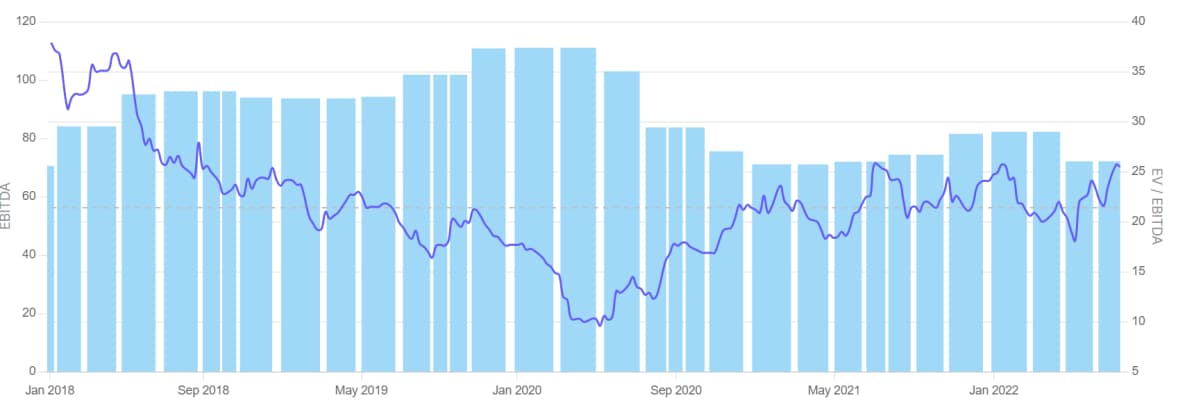

Historical Valuations:

Antithesis: RM headwinds not going away, Decrease in sales due to increased competition, Impacted demand due to closing of schools due to lockdown

Disclosure: Invested