One more incidence of poor Corporate Governance.

Disclosure: Invested

One more incidence of poor Corporate Governance.

Disclosure: Invested

Significant quantity of shares have been bought by the promoters in last one week. Buying worth ~4.5 Cr. just in one week

Disc: Invested

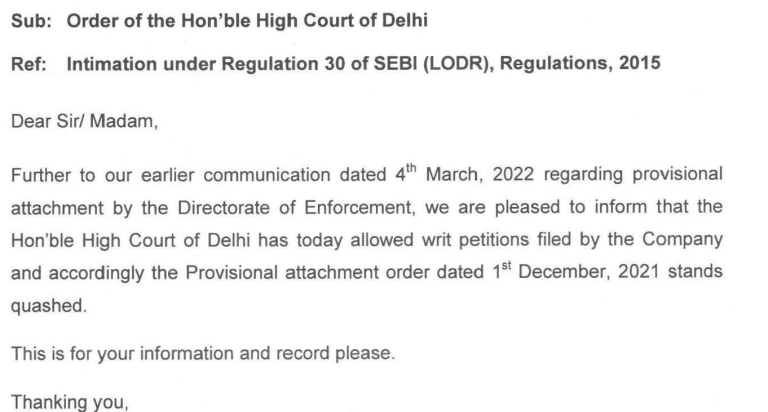

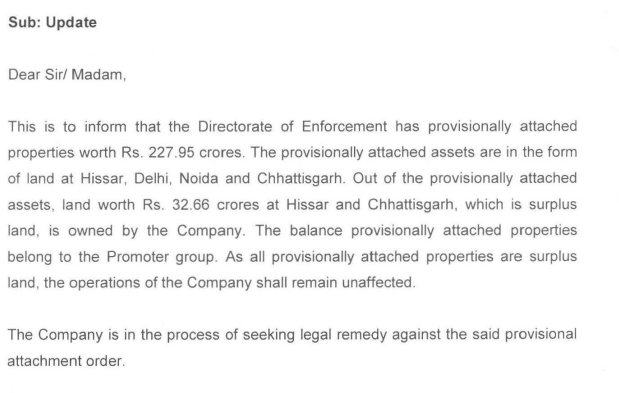

Some respite on ED attaching the property. This is a funny business, worth a case study. ![]() Promoter group just cant get rid of the news headlines for investigations…

Promoter group just cant get rid of the news headlines for investigations…

The below was the original update in Dec’21 about ED attaching the property

Disc - Invested as a hope that the assets(captive coal block & iron ore mine) will play out in 1-2 yrs.

It’s completely miror image of what India is facing.

We all r moving from old congress era to completely transparent modi era.

Promoting family also facing same transformation but Purani aadte badalne me der to lagti he!!

It’s high asset company promoting family know how much it worth that’s why they r buying from Market.

Disc. I don’t own any shares

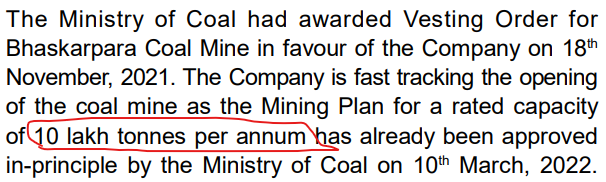

I am not sure if I am doing the math correctly. Prakash says in annual report(also in press release few quarters ago) that 10 Lakh ton per annum coal would be available to it. Let me consider the current price per ton for Coal is - $260/- (I have no knowledge about it and my guestimate might be very very wrong). That gives the additional revenue of ~2,000 Cr. to Prakash Ind assuming all the coal is sold in open market. Off course, they will use majority of this coal for making Steel. Despite that they will be left with some coal from 10 lakh ton per year to sell in open market. Even if I assume on 50% benefit, the potential benefit of about 1,000/- cr. once the coal mine becomes operational. There will be rise in expenses to mine and transport the coal, royalty etc. I tend to think, there is a meaningful upside to the earnings some time next financial year due to getting the coal mine operational.

Just wondering is I am missing or miss-calculating something?

Realisation will depend on the Coal grade which has not been shared by the Company . Also Iron Ore grade is not known…

Can any body with good hands on accounting advises as to why the Tax Paid by the Company is almost Nil:

YEAR 11 12 13 14 15 16 17 18 19 20 21 22

PBT 274 276 167 204 9 23 88 388 553 118 95 169

PAT 267 268 165 173 9 23 81 386 539 118 95 169

TAX%2% 3% 1% 15% 0% 0% 8% 1% 2% 0% 0% 0%

As per Anual report:

“The Company has outstanding FCCB of US$ 10.80 mn, which are convertible into shares on the exercise of the conversion option by the bondholders. The FCCB have maturity date of 15th January, 2023 and carry interest @5.95% p.a subject to condition in the subscription agreement. Interest of 2,103 lakh is outstanding on account of non furnishing of correct bank account details by the bondholders. The Company has complied with all the financial covenants and undertakings with respect to the outstanding FCCB.”

As the bonds have not been converted, it would have been paid on 15/01/2023. The debt of the Company would have been reduced by around Rs 110 Cr (Principal + Int).

Its good that there is no dilution.

Valuations of the Company are cheap, however Corporate governance issues are making a huge dent. But its good that there have not been any new issues during last 3 to 4 years.

The new generation seems to much sensible and hope that things will gradually improve. The Company and present stock price has huge potential to become a 3 to 4 bagger from here, which will still be lower from the highs of 2018…

New generation is Vikram Agrawal.

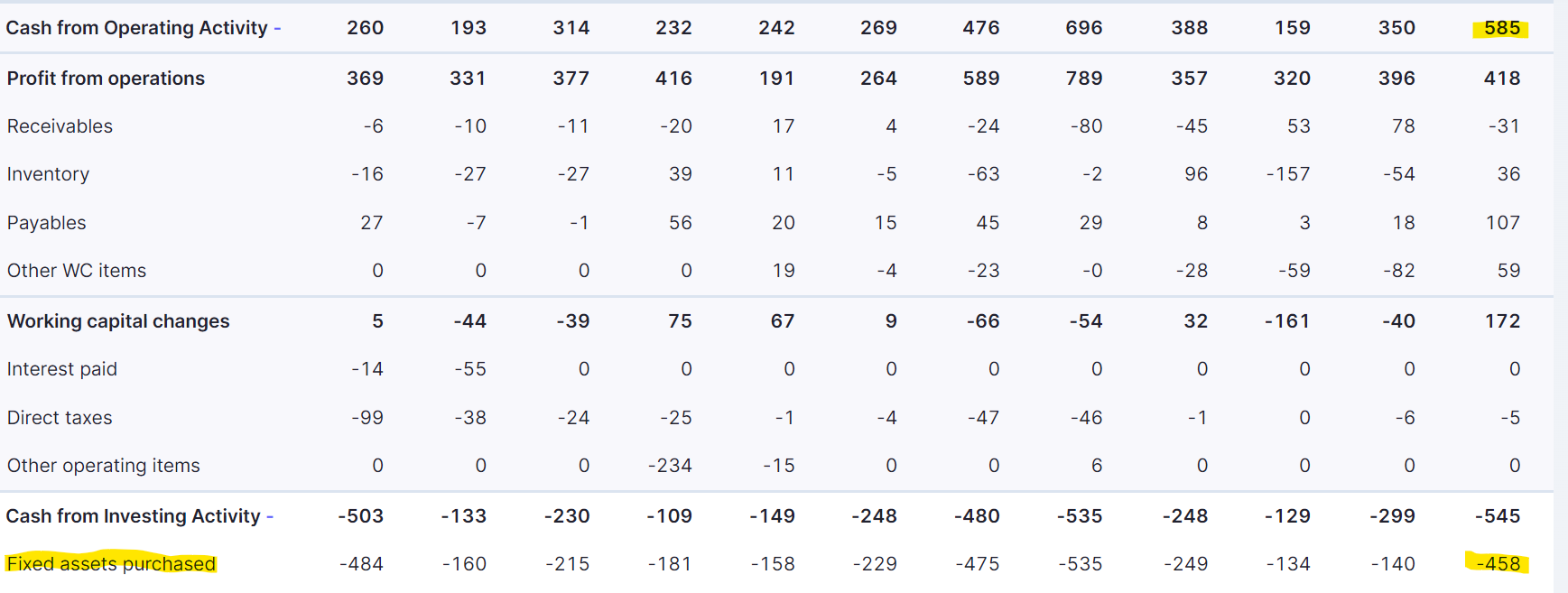

Prakash has come up with Q4 results. One thing worth calling out is the robust cash flow of over 500 Cr. (While market cap is around 1,100 Cr.)

What surprises me is - They have purchased fixed assets worth - 458 Cr. during last FY. Which is three times the fixed assets purchased during FY previous to it. But they have not mentioned anything apart from Coal mine approval in the press release. Is there a royalty they might have to already be paying to Govt for Coal mine and Iron ore mine?

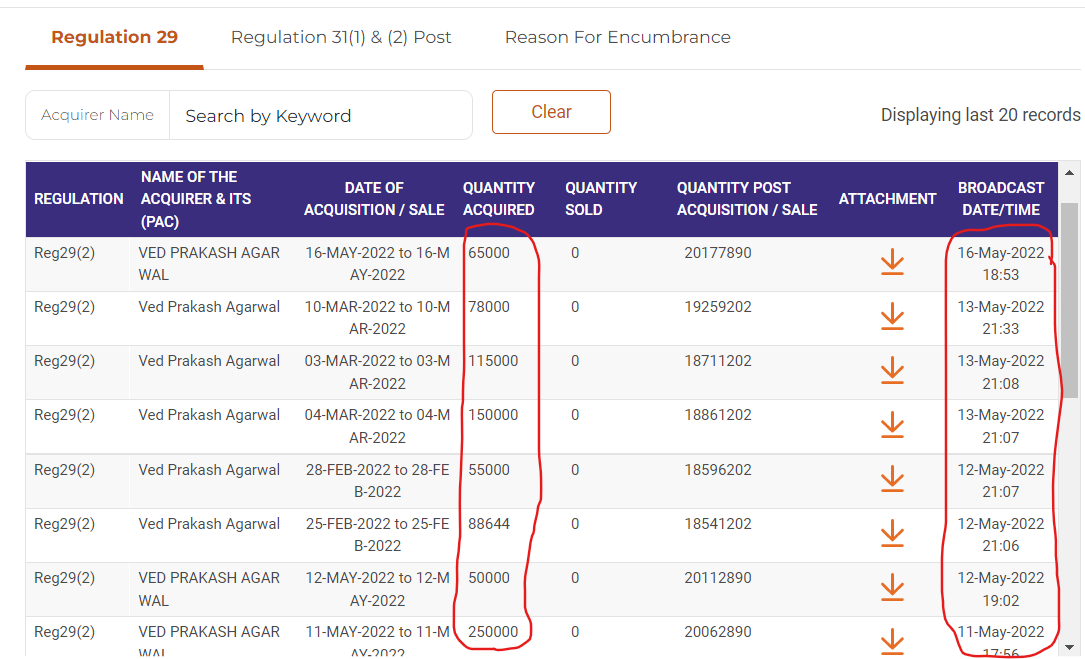

Btw, Ved Prakash ji is purchasing about 20,000 shares per day for last 3 days…

Promoter continuously buying from market

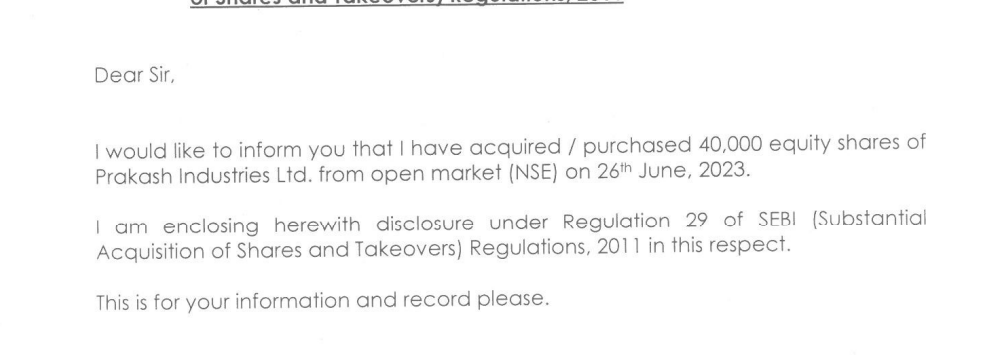

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 29/05/2023 | ACQ | Market | 130000 | 0.07 | 20821784 | 11.62 | 11.62 | 29(2) | 29 May 2023 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 26/05/2023 | ACQ | Market | 115000 | 0.06 | 20691784 | 11.55 | 11.55 | 29(2) | 26 May 2023 |

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 25/05/2023 | ACQ | Market | 60000 | 0.03 | 20576784 | 11.49 | 11.49 | 29(2) | 25 May 2023 |

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 24/05/2023 | ACQ | Market | 19254 | 0.01 | 20516784 | 11.45 | 11.45 | 29(2) | 24 May 2023 |

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 23/05/2023 | ACQ | Market | 23873 | 0.01 | 20497530 | 11.44 | 11.44 | 29(2) | 23 May 2023 |

| 506022 | PRAKASH INDUSTRIES LTD. | Ved Prakash Agarwal | Yes | 19/05/2023 - 22/05/2023 | ACQ | Market | 22585 | 0.01 | 20473657 | 11.43 | 11.43 | 29(2) | 22 May 2023 |

Now we know why promoter was buying relentlessly in past couple of month.

Results - https://www.bseindia.com/xml-data/corpfiling/AttachLive/375c6740-d854-4e5c-be91-b782cfd44ee0.pdf

Press Release - https://www.bseindia.com/xml-data/corpfiling/AttachLive/327718a2-002b-4ecf-bc51-1fe733355491.pdf

The EBITA increase is impressive. From Q3 the coal mine commences. That can only improve the EBITA margins. The steel prices scenario looks decent in domestic market. The cash flow from Prakash is very good. If they want, they can repay the entire debt of ~550 Cr in just a matter of 18 months. The cash flow is expected to increase even further with the coal mine production commencement.

Core business performing better, Debt repayment and Coal Mine production are key drivers for next 12 months.

Disc - Invested. increased my exposure while promoter was buying between Rs. 57 - 65.

Positive developments are being seen in the Company. Performance improving, promoter increasing their stake, Depledging of shares and last but not the leat… no negative news during last 12 months.

The stock seems under valued at current valuation and may run up in the current bull run…

Disclosure: Invested…

Most of the unicorn struggling to get outof loss. And such companies which r delivering profit since last 10yr are trading at PE of 5 or 6 how pathetic.

It’s completely backward integrated steel company. Having own iron ore mines , captive Power plant, own coal mines.

Why promotors are not coming out of old era, today u can’t sifonig of money, u have only legal route available which is pay taxes and take dividend.

Market will reward u much more than black money route.

Mr.Jhunjhunwala invested long before it means the company must had some real large assets base, but he failed because of wrong mindset of promotors.

But now the time change and I hope promotors will realise what is demand of time.

Disc. Invested

Discl

Hai investors I have had holding in this company believing in all the good things written in 2018 period and even have posted postive things ( confirmation bias) earlier. Sold all my holdings in loss and hence I may have negative bias.

First I did a scuttle butt to chamba one time when I was nearby and I can tell you yes there is a factory and people are working and producing

But the promoter has a very unique talent of siphoning money through various avenues ECB conversion of ECB and only companies which does not pay interest on ECB because they don’t have the investor information

Second they will use security premium account method based on a old court order for non payment of income tax

Third there sales is 60/70 concentrated to particular suppliers

They demerged one entity prakash pipes and trying out to be clean in that even there habit has started

They have all sort pending legal cases with DRI and ED under various allegations but non has been come to final so until proven not guilty

If u guys closely look at the balance sheet cash flow and promoter holding pledging method and how they convert ECB to shares how they issue conversion warrants and the equity dilution have happened and how the selling pattern happens when the market is in good mood it will give a more whole picture

I may be negative biased as stated in beginning so please do your proper checking before investing in such companies

Prakash has got the final environment clearance for operating the coal mine. As per my reading of the press release, the coal will be available to them from the given mine during Q4’24 OR Q1’25. Please correct if my reading is incorrect

For me biggest question in my mind is - On what fixed assets they spent 458 Cr (which is about 22% of current market cap) from the cash of ~585 Cr they earned in FY23. And is that amount going to be required to be spent on-going basis?

Disc - Recently have sold out the holdings due to sharp run up. Will keep an eye on the counter though. I am most interested to understand - What quantity of coal they are able to sell in the open market.

Hello Everyone , is anyone Fundamentally Tracking Prakash Inds cmp 141

as per SHP announced today SEPT 2023 posting below as per Screener

looks like things are changing here soon for good

September 2023 SHP , for the 1st time

Mukul Agarwal Name appears with 25 Lk Sh or 1.4 % Eq &

Dolly Khanna 18 Lk Sh or 1 % Eq

FII holding now 6.35 % Eq from 3.57 % Eq in June 23

Promoter Keeps Adding …

since most have given up here

Number of Share Holders is Coming Down ( good sign ) ![]()

PRAKASH INDUSTRIES LIMITED

Bhaskarpara Commercial Coal Mine Update The Company is pleased to inform that today it has made payment of Rs. 32.62 Crores to the Forest Department towards Non-Forestry use of forest land and Wild-Life Conservation Plan for its Bhaskarpara Commercial Coal Mine in Chhattisgarh.

As informed earlier, the Company has already received Permission to Establish from the Chhattisgarh Environment Conservation Board and paid Rs. 23.25 crores towards Net Present Value (NPV) of diverted forest land and Rs. 35.12 crores for compensatory afforestation with respect to Bhaskarpara Commercial Coal Mine

Significant reduction in pledged shares. No pledging observed in last 1 year.

There is a rating agency report

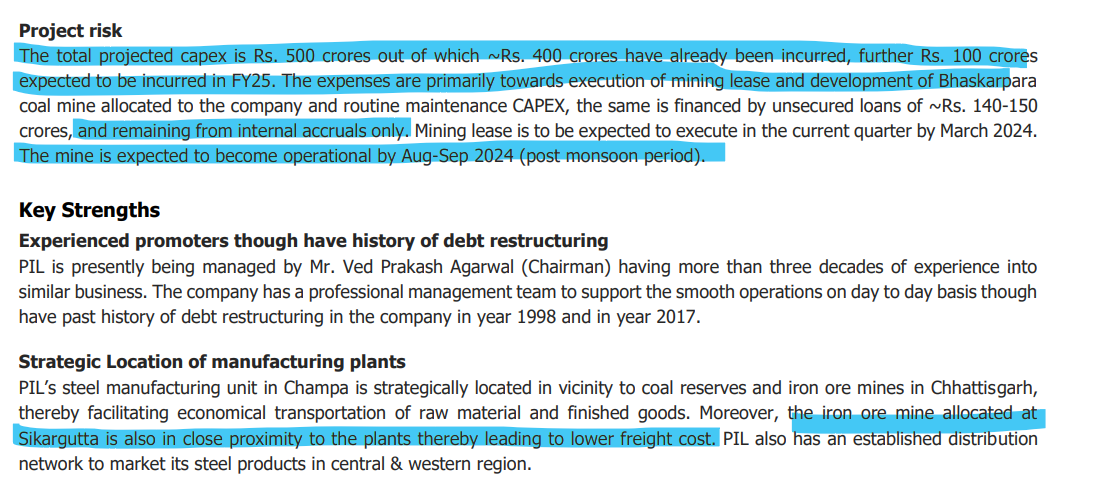

What is re-confirms is that investment in developing the coal mine are about 500 Cr. and out of which ~350 Cr. are from internal accruals. The report is also reconfirming that mining lease will execute in about 7-8 weeks from now. operations will commence from ~ Q2’FY25. Additional revenue will start coming in.

What would be very interesting to know is the potential revenue/cost savings that the company is hoping for on account of this coal mine. @Rakesh_Arora sir, would you be able to share some views.

Link to report update report - https://www.careratings.com/upload/CompanyFiles/PR/202402130231_Prakash_Industries_Limited.pdf