Hello members

I am not able to understand the following

Negatives from my little knowledge iam not an accounting expert.

If PIL has generated a reasonable amount of operating cash flow as seen from the screener.in and they have used it for assets and it is shown as CWIP and suddenly there is write off still even today there is huge amount in CWIP will this be also written off how far this will effect the book value.

Secondly if we see the last 10 years they have taken ECB and after some time instead of repaying they convert the ECB into equity and allot it to the foreign investor and later on the they dump the shares in the open market and the equity of the company is increased the promoter holding goes down does it look like some thing wrong here or is it ok.

Then if watch closing there are some pvt ltd Calcutta registered companies non promoter holdings changing hands often and name changes from PVT ltd to LLP

Continuous pledging and releasing of shares by the promoters to the same entities and promoters increasing there shares by way of issuing warrants to themselves even though they say it is subscribed at higher price now the money is being return of from the books how

POSTIVES

Income tax has given clearance before the NCLT for the demerger after a long delay that means the company records clean.

The ED is dragging the case and promoter is giving always a proper clarification.

The promoters long standing and vast experience and the effort they have put for capacity increase and there belief in the steel segment.

Now thy are giving dividend in both in PPL and PIL

The steel cycle improvement and there ability to withstand even in low period

The left over CWIP is the planned increase in capacity from 1.0m to 1.2m. Dont think this will be written off. Capex was scheduled to be completed long back but as with everything else with the company, this too is being dragged over multiple quarters.

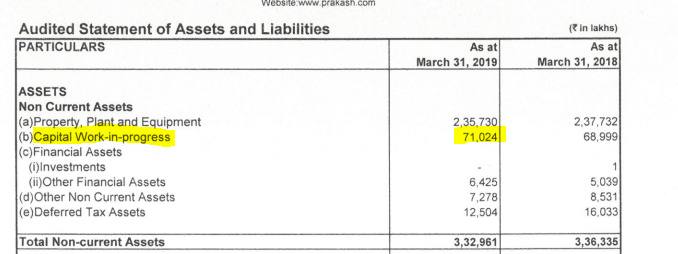

CWIP is still a very big amount…

The company should conduct a conference call for clarifying all such issues. I think those who have already invested should write a mail to the company for the same.

Prakash pipes seems to have reported good nos. in FY19. EBIT has grown only 10% or so but RoE of 26% is quite good and listed at TTM PE of ~7. OCF conversion to PAT Is 71% which seem to be great as well with low leverage balance sheet. All litigation, cyclicality is with steel biz but pipes biz should be free from all that except possible promoter discount.

Accordingly, the Allotment Committee of the Board of Directors in its meeting held on 13th June, 2019 have allotted 79,17,023 Nos. equity shares at a price of Rs.210.18 to the said warrant holder. Consequent upon the aforesaid conversion, the paid up share capital of the Company has increased from Rs.1,63,34,68,300/- to Rs.1,71,26,38,530/-… I am fail to understand why promoter is conversion of warrant at very high price Rs.210.18. when they can buy form open market 60-70 per share? any light in this will be helpful? Thank you

I see this as the fulfilment of soft commitment to the company. They are placing trust in the company and believe that the value of stock is higher than 210. See that pledge is also down to 48% (from 70%+ 6 months back). I feel that Promoters are focusing on market cap appreciation instead of siphoning off money. During last year, after the small cap debacle, fake companies have shown significantly less revenue and PAT, while Prakash has shown consistency! While majority of the stocks that have gone 605+ down are unlikely to make a comeback, but I believe Prakash will be an exception. Only time will tell and there is high probability of me being wrong here!

Just compare the conversion decision with the decision taken by the promoters of Sintex Plastics. You’ll get to know the difference. Having a base business and decent balance sheet is umpteen for a promoter to go ahead with infusing extra 124.8 crores (210.18 * no. of shares * 75%)

No recommendation. A very risky bet! I am holding Prakash Ind.

Thanks for your relay and I quite agree with that one paper everything looks improving for the PIL, But then why there is a huge selling by NBFCs registered with RBI there Shareholding Pattern shows the NDFC holding has been largely reduced in PIL . its has came done from 27% (June 2017) to 0.04% (June 2019). why there is huge continue sale by NBFC and other parties. If fundamentals are improving on paper and promoters are showing confidence by warrant conversion at very high price then NBFC sale is contradicting. also there is no MF interested on this stock even trading at very low PE and PV value? Please the senior members try to put some light on PIL present condition any cloudy reason behind this or their present account book?. The disclosed PAT is not real or what? Disclosure : Holding PIL since Jan 2018.

2dc4c481-0d85-4c6f-83a8-9f9bbfdc0c69.pdf (558.4 KB)

The company has got surface right permission to operate the odisha mine. The iron ore extraction will be begin in 15 days as per the company PR.

When stock price goes down, people specifically search for negatives! below is the screenshot of B/S from company’s filings. Let me know if I am missing anything!

PS: holding shares and will continue to hold at least till next bull run

The tangible asset figure of Rs 3067 Cr in website of Money control is equal to Rs 2357.30Cr +710.24 Cr.

I think they have missed out to bifurcate the same.

But my actual worry is why is there such a large CWIP and what are its component. The Company is generating very good amount of Cash from operations however a mojor portion of it is going for CAPEX. If the CAPEX are real and the company can generate decent return on its assets created then it will be a good investment for us.

But the way the stock prices have fallen, it is really very difficult to figure out the reason. The management is also not helping and no clarification is being given. But i have experienced from market is that stock do not fall 50 to 60 % without any reasons. There are investors who are closer to management and they might be aware of things which we are not privy to.

Disclosure : Invested and forms a substantial part of my investment.

Note 5 of the statement of financial results, in respect of adjustment of liability of Rs. 2,400

lakhs being amount paid ,/to be paid pursuant to a settlement of claim by the Company

through mediation in the court, by withdrawing an equivalent amount from General Reserve.

Had this adjustment not been made, net profit before and after tax and total comp rehensive

after tax for the quarter ended June 30, 2019 would have been lower by Rs. 2,400 lakhs."

Can any body throw light on this settlement matter.

Operating margins have been sucked out due to increase in Raw Material prices and fall in Finished goods prices.