0.2%. Quite small to have any material effect…

the pledge you are saying is non promoter

the promoter has further released the pledge nearly 40 lacs shares released in three months

from 4.3 cr share pledge now 3.89 cr shares is the pledge

anti dumping duty on steel products concluded investigations recommends imposing anti dumping for imports from china will this have any bearing on this stock

http://www.dgtr.gov.in/sites/default/files/Bars_Rods_FF_NCV_5_9_18.pdf

q2 result looks good and consistent but if somebody could explian the segment results about why the steel segment profit is shown less or why it varies from the previous qtr it will be helpful.

1 Like

See YOY I mean September quater is always the weakest ones U won`t be surprise seeing the yoy Increase in raw material prices and weak demand always affect this qtr I see no negative in result In-fact its good result if we know how steel industries works I am from steel bckgrnd. For overall we need to see power sector and pvc They are strong as firm Plus new venture is doing great”

except for the rise in receivables from 98 crores to 192 crores

3 Likes

I am unable to justify the fall in Prakash Industries prices. Anybody have any idea then please enlighten. Apart from receivables going up (double) … nothing seems to be horribly wrong. Posted Half yearly EPS of 18. The dubious past of promoter is already know … is that a primary reason?

Global sentiments sir! check how commodities fell in China today. Even Indian steel prices seem to have started softening as I mentioned in the Sarda energy thread. Previous quarter nos are backward looking. No doubt the stock is cheap but so are larger caps where funds should flow initially.

1 Like

There may be something which we are not aware of.

Receivables rise is not significant.

I am also surprised…

May be irrationality of market or any thing else

Any thoughts in this article please…

1 Like

Got the following whatsapp fwd

STEEL SECTOR: CHINA STEEL PRICE CORRECTING MAKING IMPORTS VIABLE | INDIAN STEEL STOCKS AT RISK!

Steel stocks looks vulnerable given the sharp correction in steel prices in China, steel imports have become viable

** Landed cost of HRC Imports from China is ~INR 42000/ tonn v/s Domestic price of INR 46000/ tonne. Whereas the anti-dumping duty price threshold is INR 35000/ tonne.

-

*One can expect prices to correct by INR3000-4000/ tonne over next 2 months. This will trigger earnings downgrade cycle for Indian Steel stocks

-

*Tata steel, SAIL, JSPL appears most at risk For every INR 1000/t correction in EBIDTA the target price of Tata Steel reduces by INR 80/ Share

1 Like

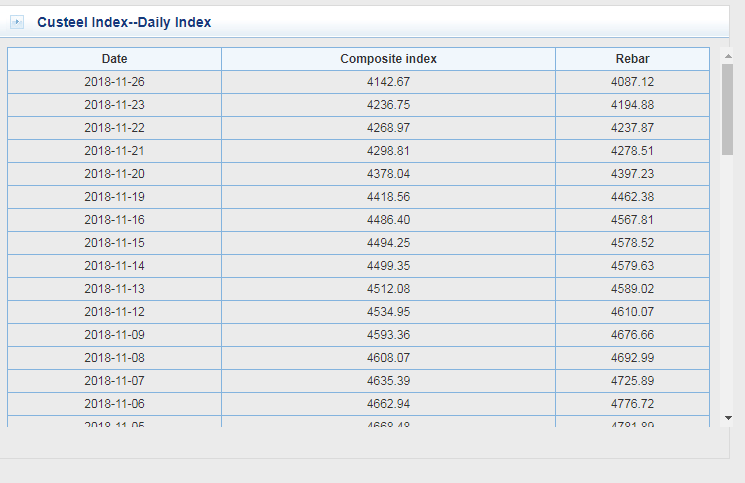

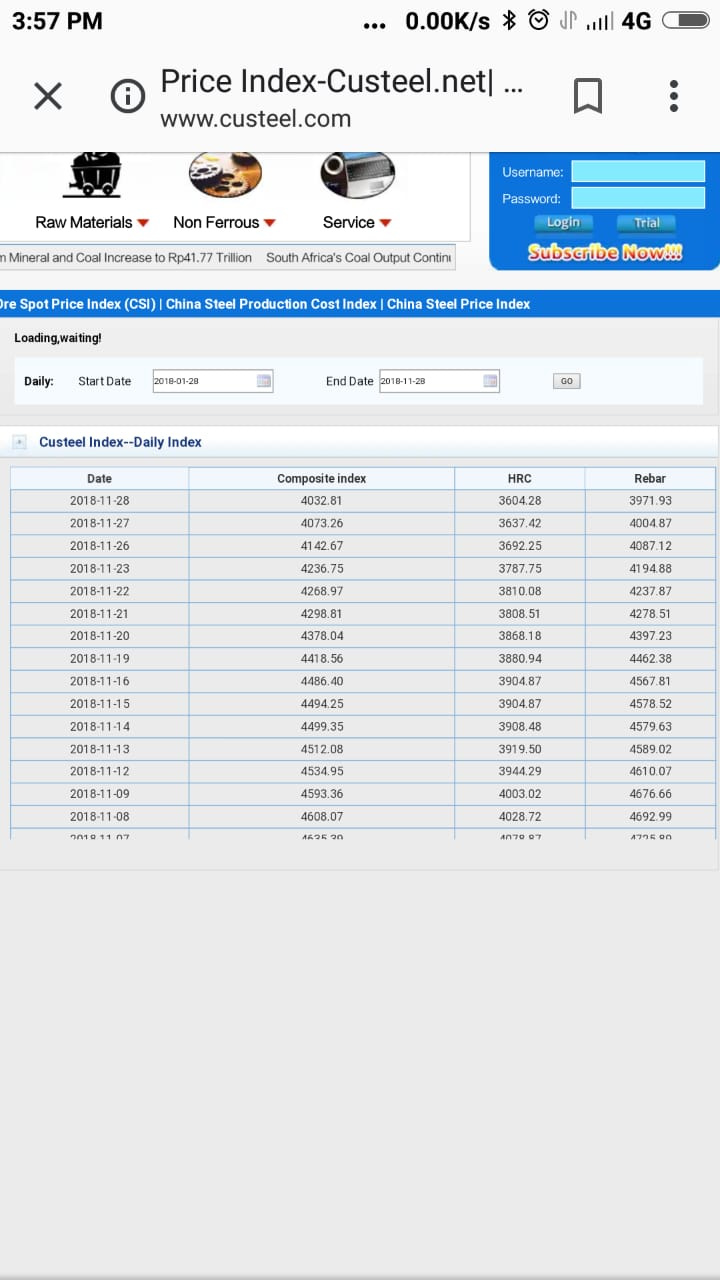

I have doubt on this message. It says Landed HRC prices from China comes to 42000/ton. I read various articles on net and also referred a site for prices of HRC in China. It mentions that HRC prices is 3400 yuan. If we convert it into rupees with 10.16 rupee per yuan then we get 3400 X 10.16 = 34544. Now add import duty (10 % import duty, 12% CVD-Countervailing Duty & Spl. CVD of 4%). Then the total price is 34544 X 1.26 (26% import duty) 43525. I have not even added the transport cost. To have the 42000/ton of total import cost the HRC prices should have been 3000-3200 yuan per ton.

Most of the online articles mentions that prices have crashed to 3400-3500 yuan. That said the prices might have crashed more till today but the maths does not match up when I do the calculations.

Also if I refer the site www.custeel.com/en/prices.jsp then the price of steel is 4032 yuan, HRC is 3604 yuan, Rebars is 3971 yuan. Obviously the prices will differ region to region but these number (HRC) prices does not matches with the message of landing cost of 42000/ton. According to my calculations the landed cost is 44000 to 45000 per ton if we consider HRC prices of 3400/ton. I haven’t considered the transport and logistic costs in this.

Snapshot of Chinese prices of steel, HRC and rebars from custeel.com ![]()

It is clearly evident of steel price correction in Indian market. When I refer the steelmint site the latest prices of Rebars (Ex Delhi) is 38600.

All in all I think the landed cost is between 44000 to 45000 for HRC and even more for Rebars. The import duty structure is 10-12-4 which still makes import non-viable if HRC is at 3400 range. It should go to 3000-3100 range to be import viable. Note: I haven’t added the transport cost (Shipping logistic cost from China to India) in my calculations.

5 Likes

One thing to add is HRC is flat product, where as prakash deals in long products.

1 Like

Yes, as I mentioned Rebars landed cost is even higher than HRC. Given Rebars is good 400-500 yuan costlier than HRC. Rebars is at least 50K per ton if imported from China. Logistic cost not included (because I dont know the actual shipping cost).

1 Like

1 Like

I am not defending Prakash here and believe this ED move is really a bad news for Prakash at least in short term or till the dust settles

But this ED move is against which CoalBlock case? The coal blocks which were cancelled by supreme courts? or is it a fresh issue? Asking because I never tracked these cases.

If it is old issue then whats going to come out of is really a question… I believe a case was filed against it in 2013-14 and nothing came out then… Is this case reopened on the fact that Supreme courts have pressed the investigating agencies on the issue or is there any substantial evidence found?

Nothing is known clearly today

3 Likes

-During Q3FY2019, the Company has achieved Net Sales of Rs.1026 Crores and EBITDA of Rs.206 Crores, reflecting growth of 41 % and 35% respectively over the corresponding

quarter of the last financial year

- PAT growth of 40 % , 140 cr vs 100 cr last year

-The increase in the profitability is due to higher production volumes and operational efficiencies.

1 Like

Prakash Industries …

11 year FCF = - 324 crores(Negative cash flow)

11 year profit = 2174 crores…

where is the money invested ? company generated 2174 crores in net profit and invested around 2500 crores , ?

where is the return on capital

Company has never paid dividend

Company has never buyback its shares

Share capital increased from 108 to 163 crores .

5 Likes

Prakash Industries announced that the hearing of the scheme of arrangement between Prakash Industries and Prakash Pipes (demerger scheme of PVC pipes undertaking) was listed on 10 January 2019 before Hon’ble National Company Law Tribunal, Chandigarh.After the hearing , the order has been reserved by the Hon’ble bench.

1 Like