If you skip 1G ethanol, everything else is pretty much in line with what is happening globally. They are doing things right in plotting opportunities (2nd Gen ethanol for instance). Globally, material science innovations are also at R&D/Pilot, at best. Very few companies are advanced enough to scale up. The reason is that decarbonisation is a relatively new theme and competing technologies with possibly newer techs coming in that will not be entirely linear.

For instance, last year there was a validated research for lignocellulosic feedstock (2nd Gen ethanol) in which a CRISPR modified yeast with genes for toxin tolerance as well as aldehyde to alcohol conversion (ligno feedstock has this issue of aldehyde generation on pretreatment… which the modifications helped to convert to alcohol).

This catapulted lignin feedstock yield to at part with 1st gen (glucose). Which means higher RoIs as there was no mention of special equipment as disruption is perceived to be non-linear…. that is, by modifying the biological systems (yeast). Repurposing by otherwise waste material to create potential fuel. This would also help in the food vs fuel debate. Save precious resources as well.

So, there’s immense value to be tapped but everybody is on a stealth more right now as the space is still evolving and it will take time for definite patterns to emerge.

In short, to find “value” in Praj at this level, one has to be incredibly patient. Virtuous cycle of ethanol-blending volumes will give them sufficient cash when they need it going forward to work or partner with biotechs or to do their own pilots. But no other company in India is better placed to benefit from a broad-based bio-economy push. Which would take a quite a few years though.

10 Likes

Thanks for your comment. I understand the immense possibilities of industrial biotech research and I understand that Praj is scientifically and technologically best placed in India to take the industrial bio-economy forward. The only reason I track Praj is because of these immense optionalities.

The issue is I am not able to see a smooth bridge from 1G ethanol and EBP 20 to revenues from CBG/Diesel blending/RCM/hi-purity water etc and I am also not able to project revenues from these breakthrough technologies. As far as I can understand Praj will run out of 1G ethanol projects in FY25 and from now until FY25 it may do another 5000Cr of 1G Ethanol related revenues in India and abroad. What happens after that? There is no visibility to project Praj’s revenue streams post FY25 -

- Will CBG scale up sufficiently by then? What’s the revenue potential from setting up CBG plants in India?

- Will India sanction diesel blending for static/automotive engines by FY25? Have there been successful diesel blending programs in Brazil or rest of the world at scale? What’s the likely % of Ethanol blending in diesel?

- What’s the potential of fermentation and hi-purity by FY25? Revenues are de-growing/stagnant as of now.

- What’s the potential for SAF by FY25? As per Management comments it doesn’t seem like ethanol based SAF will get commercialised by then.

- What is the potential for RCM by FY25?

There are no answers to these questions so far. And my biggest problem with Praj is in spite of their high science capabilities, almost all of these revenue streams (maybe except hi-purity) are capex revenue streams which involve setting up Plants for clients. There is no pathway demonstrated by Management yet that would lead to opex revenues. A capex business might bring in large revenues for a period of time like Ethanol 1G did, but will it move the needle on profitability and free cash generation? What’s the kind of FCF that Praj will generate at 8% EBITDA levels? Being restricted purely to capex revenues makes Praj orders of magnitude less attractive as a company than if it had a growing component of opex revenues. As on date, Praj’s service revenues are 5-6% of its total revenues and that too are mostly Plant related O&M revenues.

Under these assumptions, if I run a 10Y DCF on Praj, with a generous terminal growth rate of 5% and 10Y exit FCF of 500Cr, I will still probably arrive at an MCap which is about 50% of today’s MCap.

I hope you now appreciate where my dilemma lies with Praj’s valuations. I don’t doubt the science, I doubt two things

- The timelines of the conversion of that science into revenues and profits

- The capex nature of revenues vs opex from those exciting new biotech streams

Would appreciate if you or anybody else can leverage your knowledge of the science to help fill these valuation gaps for me!

8 Likes

Firstly, I don’t share a different opinion in terms of valuation as to what you said. That’s why I mentioned one has to be incredibly patient. By the magnitude of patience, I probably would take a longer view than 5-7 years. Of course there are opportunity costs attached. But beyond the definite cash generating bit, the other business is still in stealth mode. And it’ll be while before anything meaningful happens. I say that because that’s where we are globally. R&D money flowing in but yet to reach scale up in these newer techs.

For eg, I track a European company in bioeconomy space. They have been working on a product with a multi-billion dollar replacement potential. Have been doing it for many years. And they are yet to scale up. All at the cost of equity infusions, grants and pledges by customers who want to decarbonise. So this space is hard to value but I would want to keep my one leg in.

On the opex revenues bit, I don’t have a reason to believe the expectations should be very high until the newer gen scales. Secondly, another source for it would be where Praj has a product or systems IP. Which it could out-license. It’s not gonna happen any time soon.

The competency in Biopharma and Fermentation API synthesis is quite different. Their expertise will be more towards the API synthesis side because of their legacy of working with microbial fermentation.

I have actually asked them in the past of their right to win in Biopharma competing with global leaders such as Thermo and Sartorius. And they hinted that their expertise is in Hi-purity water systems. So, reading more into it, I would argue that it won’t be worth betting them getting very deep into Biologics value chain. Because the global giants offer much more than just equipment. These are entire platforms along with cell lines and media. So there’s difference in expression systems, media, fermenters as well as monitoring tools and software.

So, I would at least from where we stand right now, put Biomaterials or positives on the fuel side much above the rest. Because that’s where their competencies lie. When enquired about CBG on the call, they had indicated about being cautious because these are gas-based systems and Praj has had liquid-based expertise. So, there’s no definitive over there as well.

But I think there would be enough opportunities in the biomaterials space going forward such as 2G space because of a very beneficial use of ligno-waste. Rest is wait and watch.

6 Likes

But I think there would be enough opportunities in the biomaterials space going forward such as 2G space because of a very beneficial use of ligno-waste. Rest is wait and watch.

This maybe true but demand for 2G is constrained by EBP 20 and the need for flex fuel engines. Without SIAM buying into flex fuel engines, the automotive industry may not demand so much Ethanol beyond EBP20. With EV powertrain development already a drag on OEM resources, I am not sure how much appetite OEMs will have for developing flex fuel engines. The global scenario on flex fuels isn’t very encouraging is it?

1 Like

Biomaterials have plastics value chain as well. It’s not limited to fuel. But 2G is what’s in sight right now. Flexi-fuel could have Brazil like model because of starchy feedstock availability beyond Sugar. EVs coming in and scaling appreciably will take time. Then the problem becomes whether to further reduce reliance on fossil fuel, blend more and repurpose the fossil fuel chain into making downstream petrochemicals. Because to support our GDP, we will be heavily reliant on petrochemicals going forward.

For eg, plastics value chain globally is very low on even mechanical recycling right now. More advanced recycling is yet to practically start if you take the overall scale. By 2030, 80-85% reliance globally would be still on virgin polymer.

So, value addition wise, we would benefit better to repurpose fossil-fuel for applications other that fuel. At the same time, green-plastic, green-fuel, Algae derived fuel, etc. will have their time to shine. There’s a whole lot going on in the biomaterials space with these very same microbial systems!

2 Likes

Here it says that the enzyme needed to convert raw materials to sugar is not produced in India…so some company who gets into this enzyme manufacturing or already doing it at smaller scale might have a bumper opportunity.

4 Likes

Future will have systems. The enzyme provider, the engineered microbe provider, the equipment provider as well as the systems designer will have to work together to make a solution that works and lasts for a many years. That’s why you’ll more often find JVs or technical collaborations on such kind of projects. It’s one thing doing something on a lab scale and a totally different game on a large scale from resource and efficiency perspective. So Praj’s know-how and experience will be as important to the microbe provider as it will be the other way round.

The possibility for scalable solutions could come by out-licensing arrangements. If suppose the 2G project succeeds, it would make sense for all the parties to collaborate and make that a “system” which can be replicated again.

2 Likes

If anybody has access to this Business Standard article, please share the key insights.

Will delete this post.

The following are mentioned in the article

- India is a water-stressed nation, same is the case with the land. So ethanol production via excess sugar cane will not a viable option for India (1kg sugar cane use up to 2500Liters of water)

- Compared to the world’s biggest biofuel producers, ie US and Brazil, Both of them have low to medium water stress, and they entered this niche way before India. India is late to the party, late by 20yrs when petrol is losing ground to EVs.

- By moving to Ethanol, India will only be saving $ 4 billion/ year. This is trivial for a nation soon to be a $5Trillion economy. Further Incentives and price guarantees given by Govt may result in the overproduction of sugarcanes and will further stress the Underground water table.

- Where the excess ethanol will go if EVs gain traction, or how viable will ethanol be if crude, currently over $75 a barrel, falls to $50. This may force govt to subsidise oil companies to lift ethanol.

6 Likes

Response in line to above comments:

- India is a water-stressed nation, same is the case with the land. So ethanol production via excess sugar cane will not a viable option for India (1kg sugar cane use up to 2500Liters of water)

Not only sugarcane but now even on wheat husks, broken rice, corn covers are used because it is understood that sugarcane cannot satisfy the requirement. Just few days back ,the 1st plant using wheat husks as feed got started by IOC.

- By moving to Ethanol, India will only be saving $ 4 billion/ year. This is trivial for a nation soon to be a $5Trillion economy. Further Incentives and price guarantees given by Govt may result in the overproduction of sugarcanes and will further stress the Underground water table.

This is wrong figure, since by stopping farmers to burn fields and taking the waste at cheap price to make ethanol ,saves environment from pollution, gives farmers additional income ( Chhatisgarh government is buying urine and dung for biogas) and economy a cheaper oil.

- Where the excess ethanol will go if EVs gain traction, or how viable will ethanol be if crude, currently over $75 a barrel, falls to $50. This may force govt to subsidise oil companies to lift ethanol.

Due to Ukraine-Russia war, all european countries are now buying from middle east at higher price, which is our traditional buying route, so we are forced to buy from Russia…

So in such VUCA environment it makes 100% sense to have least fuel dependency

6 Likes

Prabhudas Lilladhar initiated coverage on Praj Industries today.

Target price : 507 which is a massive upside in a stock which has so much going on.

Moreover PL IC helps us to study the stock in a much better way.

1 Like

For those who wanna read the coverage from Prabhudas Lilladhar :

Praj Industries26Aug22 (plindia.com)

Ps: Its a really good read

3 Likes

Looks like the Market has immediately taken notice of this

Hope they are able to utilise this for their future growth projects.

2 Likes

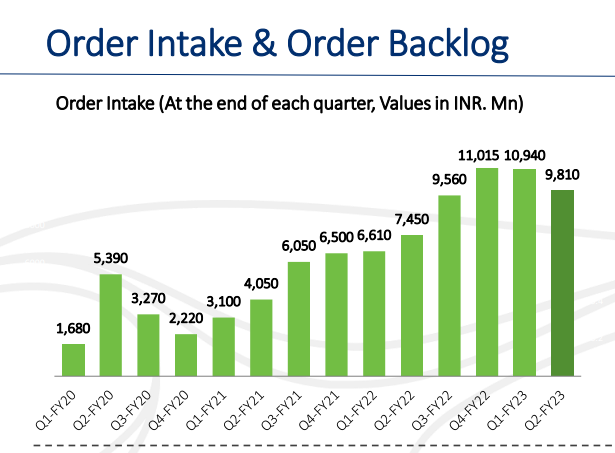

Has the order inflow peaked ?

3 Likes

Opportunity basket increases for PRAJ

2 Likes