P.S- invested

1 Like

Polyplex came out with good q1 fy 21 results as expected… Interim dividend of Rs 32 per share plus final dividend of Rs 6 per share for fy 20 declared.

For those who want to understand the business, the company has given a very detailed investor presentation.

The main highlights for me is very good geographical diversification with revenues spread across the globe, mainly from US, India, Turkey, and other geographies.

The other interesting aspect is that inspite of continuous capex over the years, net cash of 700 crores in a company with market cap of 2450 crores.

Still believe that this company is exposed to vagaries of raw material prices, demand and end product prices. Hence a cyclical.

disc: invested as a short to medium term opportunistic bet.

attached investor presentatin.polyplex q1 fy 21 presentation.pdf (7.2 MB)

11 Likes

Company is operating at near 100% capacity, growth is dependent on incremental capacity which will take time. Current margins not sustainable and a one-off case due to COIVD19 (also confirmed by Uflex), stock looks reasonably valued. Will wait for correction.

2 Likes

Hi Hitesh,

Any particular reason why you exited Polyplex corporation ? Do you see distribution sign or just profit booking as stock has ran up too much in short time…Technically, as such there is no sign of exhaustion/distribution. Company is going ex dividend (Rs 38 dividend) on 25th Aug…

1 Like

Hello. I have received the dividend today. Announcement of interim dividend of Rs 32 less TDS 7.5% has been credited to my account. However, no reflection of the announcement of final dividend of Rs. 6. Does anyone have any further information for the same?

I see 3 yrs since this thread started and nothing changed for the co. on valuation front.

Based on pure numbers perspective, this looks like an undervalued bet. But wat m I missing here as to why the re-rating doesn’t happen for this co. Is it due to - 1) Governance issues ; 2) Commodity product ; 3) Competitive intensity

Can long-term investors throw sm light on this?

1 Like

results of this company of last 3 yrs goes as follows

Revenue 3200 Cr( 2017), 4487Cr ( 2020)

Profits 231( 2017), 282( 2020)

while revenue changed with an average of 13.4% PA, Profit changed with average of only 7.35%, OPM also remained between 14-17%.

Only for Q1 FY 21, company has shown good jump in margins. If it sustains that margin for the year, then re rating may happen.( Reasons for such big jump in margins not clear, except increase in ration of specialty films, which give higher margin)

However Company is running at optimum capacity( as mentioned in presentation)

Company valuation was around 1266 Cr. when this thread started. It is almost double at 2.4K Cr. now. Almost 100% return in less than 3.5 years is a very good investment.

1 Like

The promoter stake increased from 50.03 to 50.97.

Morgon Stanly Singapore enters Ployplex with 1.23 % stake.

2 Likes

@Santosh_Sinha : - The business performance has been much better than the stock price movement and that’s what my concern was - The doubling has been entirely due to Net profit growth. When this happens, one wonders wat is it that is causing multiple to not re-rating. Such thinking helps you avoid confirmation bias.

@Hitesh_Vaghani : - Can u share the source of this plz

Please check here.

https://trendlyne.com/equity/share-holding/1054/POLYPLEX/latest/polyplex-corporation-ltd/

Also, one expansion plan is coming.

http://www.mrcplast.com/news-news_open-377239.html

1 Like

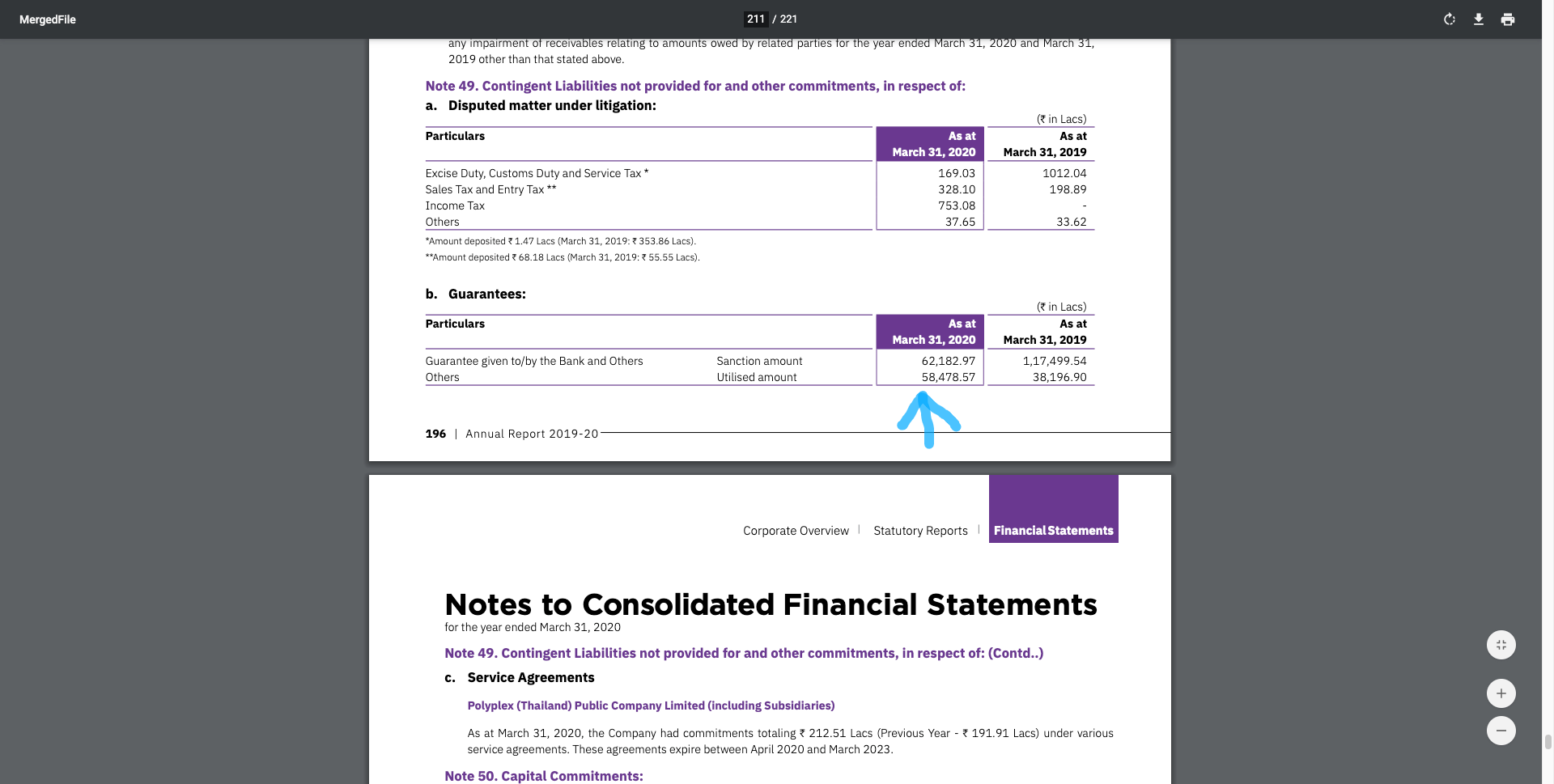

How much is the net contingent liability of Polyplex? Screen.in says 1293 cr.

In 2020 AR (note 49, pg 196) the disputed matter particulars sum up to just 10 cr.

However there is Note 49.b Guarantees section which I didn’t understand what is meant there. Nor there is any explanation to the section. (Maybe it is self explanatory and I am a noob).

The section says “Guarantee given to/by the Bank and Others” jumped from 38,196 Lacs to 58,478 Lacs. A 200 Cr jump in contingent liability.

Can somebody please go through this particular section and explain what exactly do they mean here and if is it something to worry about?

Disc: Tracking, not invested.

Attaching a screenshot of it for quick reference.

1 Like

Group co take borrowing for there respective locations and parent co have to provide guarantee to the banks as a security. This is contingent in nature and hence reported as contingent liability.

2 Likes

Makes sense. That way it is a duplicate entry of increase in consolidated borrowings. Though is there any way to confirm this?

By the way in the above case they are guarantee issued by banks on co’s behalf and not corporate guarantee as I wrote above. Guarantees (both corporate and as well as issued by banks) are not red flag.

2 Likes

Considering the expansion plans ahead one can expect 6500 cr top line on consolidated basis in next two years

1 Like

It’s difficult to digest why the market is so conservative in valuing polyplex with an EV/Ebitda of 1.84 and an ROCE without cash of 25%. On top of this all time low debt and loans and advances and all time high cash eq. Plus its thailand subsidiary has a larger market cap than the parent. Given all the free cash it is generating and the capex its poised for a re-rating in times ahead.

1 Like

I too believe Polyplex looks cheap. Though there are a few points to consider.

The Thailand subsidiary is not a fully owned subsidiary of Polyplex. it is 51% owned.

The risks (raw material, low pricing power…) are significant.

Increasing receivables.

Market cap of thailand subsidiary comes to around INR 5000 cr. Even considering a 60% holding company discount the value comes to 1000 cr. And polyplex has a market cap of 2300 cr. And company has 1115 cr cash equivalent and 600cr debt. I think the margin of safety is huge for a deep value investor even considering the risk of raw material prices and low pricing power. Basically we are not paying for growth.

1 Like

The issue which is never clear is what holds back re-rating of Polyplex in particular, and packaging firms, in general. The business has given good performance over last 3-5 yrs. However, it has always sold in the current multiple range over the entire period. Not sure what holds it back.

Disclosure : - Invested. Tracking position.