What I learned after reading the PolicyBazaar (PB Fintech) Q1FY25 Earnings Call.

Industry-level

The ability to pass on increased costs to customers is a positive sign of pricing power. However, the reliance on modular products and new designs to absorb price hikes raises some concerns.

Sustainable pricing power should stem from a strong brand, value proposition, and customer loyalty.

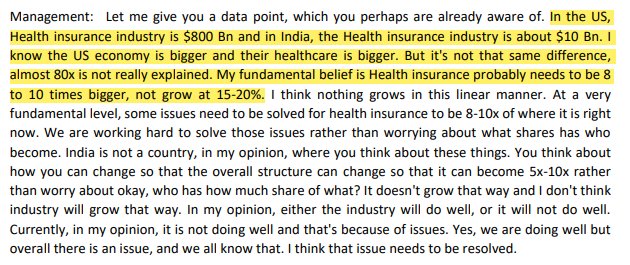

For me, this statement is both encouraging and challenging. On one hand, it demonstrates a strong conviction in the industry’s growth prospects. On the other hand, it raises questions about the specific actions the company is taking to address the identified issues and drive the necessary change.

There is significant room for growth and expansion for players like PB Fintech but it will need to differentiate itself and execute effectively to capitalize on the growth potential.

Company-level

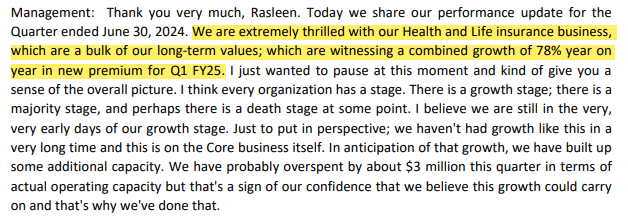

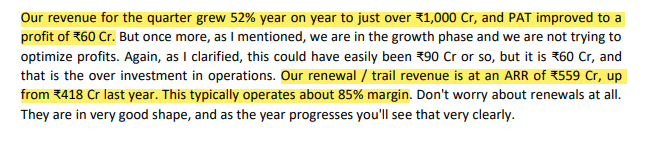

The comparison to organizational stages is interesting. Positioning the company in the ‘very early days of growth’ is a bold statement, but it’s backed by the impressive numbers. The decision to overspend by $3 million on capacity building is a strategic move that indicates strong confidence in sustained growth. Can the company maintain this momentum in the coming quarters? That remains to be seen.

The company is prioritizing investment in operations over short-term profits. This is a common strategy for companies in the early stages of growth, aiming to build a strong market position and customer base. Whether it can convert growth into sustainable profits, that remains to be seen.

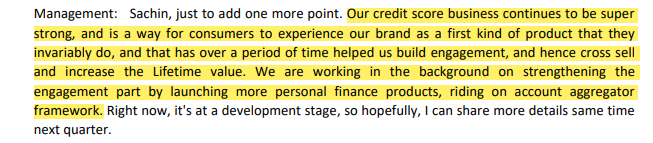

The management’s emphasis on the credit score business as a foundational element for customer acquisition and engagement is a strategic move. If PB Fintech can effectively leverage its credit score business to drive customer acquisition and engagement, it could significantly enhance its long-term growth prospects.

Management’s dismissive response to the query about revenue comparison is concerning. As an analyst, I would be skeptical of the management’s claims.The rapid growth in PoSP premiums warrants further investigation.

I’m new to valuations and investing. I came across this stock with a P/E ratio of 764(Screenr). From what I’ve learned so far, this seems extremely overvalued. Can a valuation expert help me understand this better?

here it will not be right to look on the basis of PE . Basis of valuation of any company is it’s future cash flow discounted to present time . and market expecting good cash flow and operating leverage with time . Thats why PE is not the right valuation parameter here . Although I am new to investing and not a expert of valuation but this is what my understanding says.

Thank you for answering my doubt. Just a follow up question:

PB’s current mcap is 79K and since it’s expected to deliver 600cr in fy25, it’s forward PE comes around 130. Now my doubt is, isn’t 139 a high pe still? Sorry for a newbie question!

@joinjp2003@amit151190 and others what’s your take on Star Health. They have highest market share in Retail health insurance space and have been churning good PAT with guidance of 3x PAT in next 4 years with doubling of Premium.

How shall we compare the PB fintech with a traditional insurance company like Star Health from the valuation perspective?

Health Insurance sector shall explode in India in coming time (the process has already begun). This is the accumulation stage of the long term story thats still panning out.

Being an Insurance and Banking analyst, In my views insurance is a cyclical and commoditized business , people look for cheapest insurance policy and many a times they don’t even know the name of their insurer. Most of the insurance companies would be having combined ratio more than 100 and the profits come to them through investment income. In case of commodities like steel and iron during the upcycle it takes time for fresh supply to come in so the price would be high for at least few years, while in insurance the supply can be added immediately by an insurer ready to offer lower price. Overall in my views insurance is a tough business and heard some bad news about Star Health in Gujrat where hospital denied accepting Star policies. I would stick to insurance broker rather than directly buying a manufacturer.

Disclosure: views can be biased and may be proven wrong

insurance business is a slow growth business in India. particularly in recession frustrated investors will not buy insurance. company’s credit business is also slowing due to tightening of norms by RBI on unsecured loan and POSP business is of thin margin . so company does not deserve 250 PE ratio. everyone is aware about HIGH PE ratio in recession so FIIs selling and stock is crashing . I think we should wait to add or buy freshly this stock. friends what is your opinion ?

From where can I find bifurcation of premium between new business premium and renewal premium. In their investor presentation they have bifurcated it into core online business and new initiatives. Thank you!!

I don’t think looking at the P/E ratio right now is a good way to analyse Policybaazar. It has recently turned profitable in the last few quarters after years of cash burn and continuous market share. The way their business model works, the P/E will keep decreasing every quarter upto a certain point as they continue increasing the profits (which has a lower base) in a few years. It has a 30% QoQ growth, so hardly a slow growth business. It’s the ever-increasing premium collection YoY and their outlook that makes the stock valued at what it is. Not saying it is fairly valued, but the metrics you mentioned dont really apply in this case.