Here are my notes about the company.

Business:

PNB Gilts is a dealer of government securities in primary and secondary markets. It purchases debt securities directly from government as well as secondary market sellers and sells these securities to buyers of government debt. It holds these securities on its own book while it looks for a buyer. It has a securities portfolio of about 4,327 Cr as of March 2017 funded by short term loans of 3,514 Cr and equity of about 900 Cr.

Analysis of Income Statement.

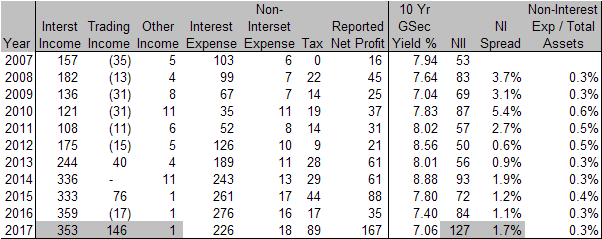

It has two primary sources of income. Net interest income from its securities portfolio and trading income. Table below shows break up of income and expenses for last 10 years.

Source: Capitaline, RBI.

Note: Shaded areas for 2017 are estimates.

As can be seen from the table above, net interest income is stable as it has managed to keep its funding cost below its yield on its portfolio. Trading income is the volatile part of the revenue. When interest rates are rising, its portfolio looses it value before it can be sold to a buyer so company incurs losses. When interest rates are dropping, its portfolio rises in value so it earns a positive trading income.

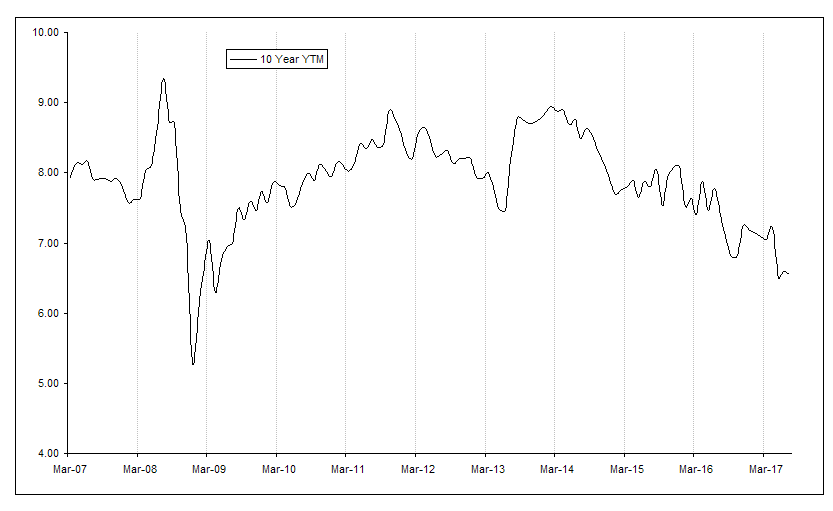

Prior to 2013, company has incurred trading losses even when 10 Year GSec yields were dropping. Since 2013, company has earned trading profits when 10 Year GSec yields were dropping with the exception of 2015-16 when company lost 17 Cr even when benchmark yields dropped from 7.8% to 7.4%. company cited volatile rate environment for the losses. Chart below shows movement of 10 Year GSec yields for last 10 years. Chart does show that yields were volatile during 2015-16.

Source : RBI

Analysis of Balance Sheet.

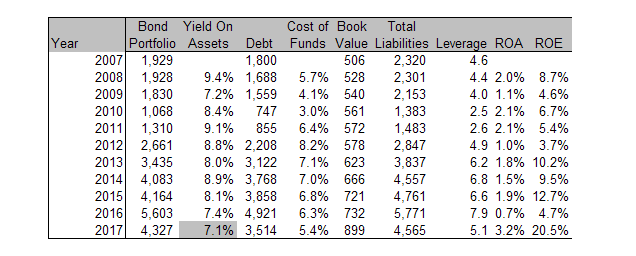

Source: Capitaline.

Assets on the balance sheet consist of government securities so there is no credit risk. Yields on these assets are close to yields on 10 Yr Benchmark Gsec. Assets are funded by short term debt with low funding costs enabling company to earn a spread of about 1.7% in 2016-17. This spread is much lower than banks and NBFCs. This has resulted in low return on assets and low return on equity. Company is also conservatively leveraged with leverage of only 5 as of March 2017.

Valuation

Net Interest Income is the stable part of the income while trading income swings from gains to losses based on interest rate movement. Company’s ROE has averaged about 12% over last 5 years which is much lower than other financial companies. On the plus side, there is no risk of NPAs. Company is getting better at generating trading gains over the years and since RBI is now in an easing cycle, we can expect company to earn some trading profits in next 1 to 2 years. Government deficits are expected to be in check so yields on government debt are unlikely to rise sharply in next 1 to 2 years. Rising book value should enable company to grow its portfolio and increase its NII in future.

Considering all these factors, company should be trading at a small discount (10%) to its current (June 2017) book value of 925 Cr. That works out to be about 46 Rs/share against CMP of 53 Rs/share.

This is also not a typical buy and hold stock. Since it is no longer trading at a big discount to book value, one should invest only as a leveraged play on interest rates.

Disc: No position.