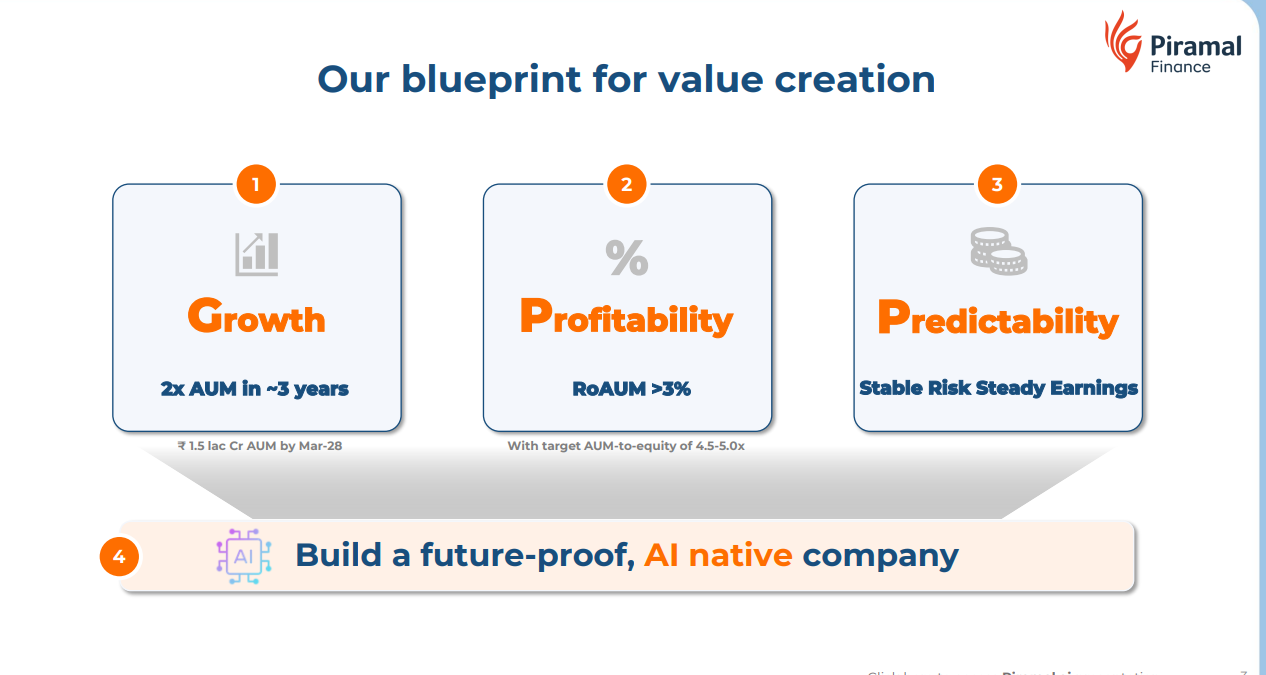

Today company sent investor PPT in which they are talking about PAT of 4500 (9X over FY25) cr by FY-28.

1 Like

When PEL announced name changes to Piramal Finance, they also announced following. Has anyone received this in their demat account?

As per the scheme of merger, for every 1 equity share of Piramal Enterprises, its shareholders will get 1 equity share of PFL and 1 NCRPS (non-convertible non-cumulative non-participating redeemable preference shares) of ₹67 of PFL (subject to approval by the Reserve Bank of India).

1 Like

per my understanding the NCRPS component was dropped as regulators (not sure if it was RBI or SEBI) objected and modified the merger scheme to just 1:1 share issuance.

2 Likes

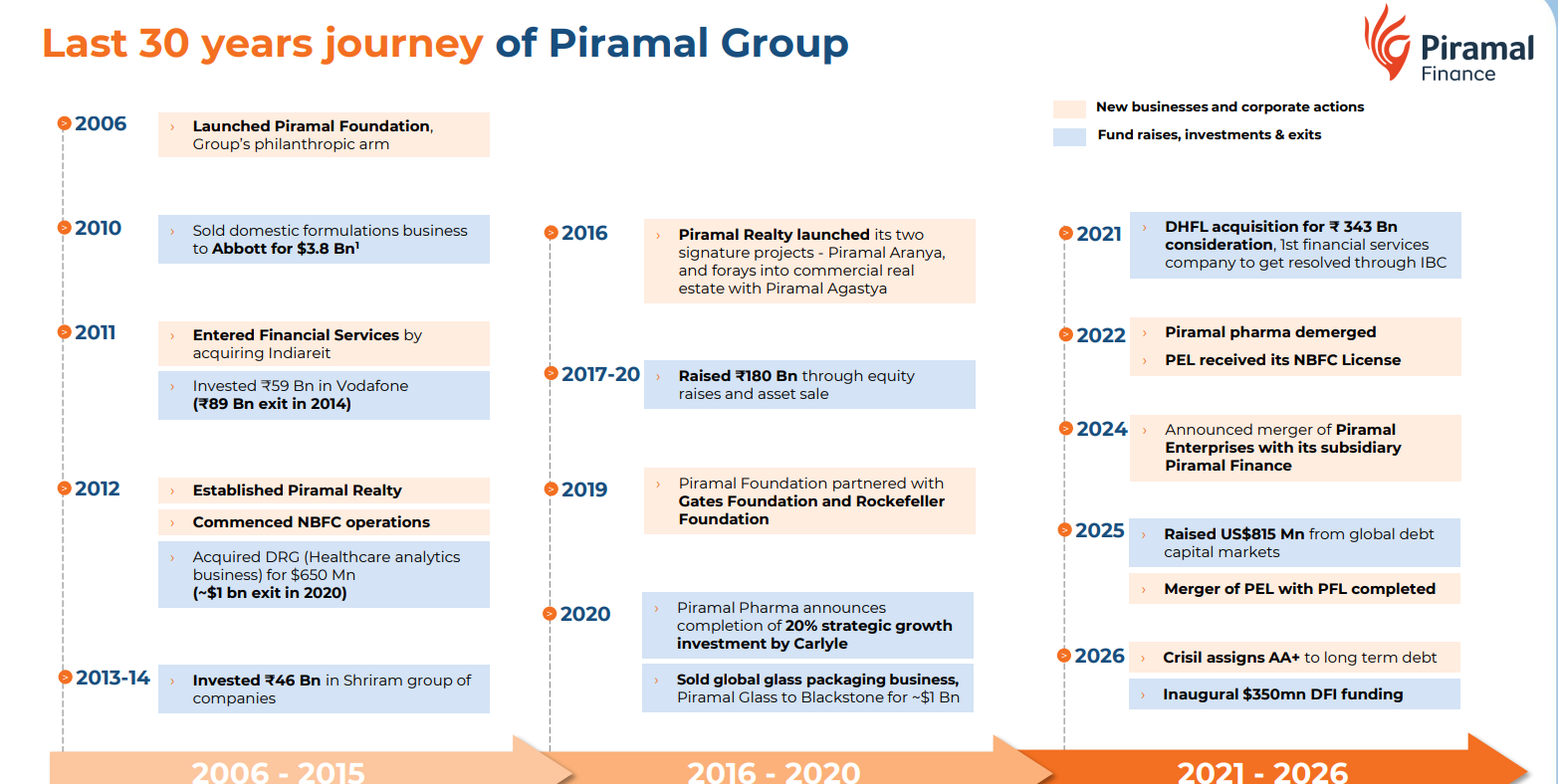

Piramal Finance is a story of a corporate which started big, got entangled in a storm and then course corrected to come back to a new path.

-

Piramal Finance, the NBFC arm of Ajay Piramal group, started their NBFC operations in 2012 along with Piramal realty.

-

By 2019, they were already a gaint with approx Rs. 50,000 cr AUM with a RoE upwards of 19%- they were the tier-1 wholesale real eastate financer financing large corporates.

-

The storm of IL&FS crisis hit them as they funded their books through short-term borrowings like other NBFCs which was eventually followed by GST, RERA and Covid.

-

They took a huge write-off of approx. Rs. 1800 cr in FY20, raised approx Rs. 18,000 cr between FY19-FY21,monitised some of their investments worth approx Rs. 9500 cr (sold the Healthcare Insights & Analytics business (DRG) for ~ 6,950 crores) and exited their stake in Shriram Transport for Rs.2,300 crores) and changed their mangement.

-

The turning point started with the acquistion of DHFL in September 2021, which helped them transtition smoothly from a wholesale NBFC to a retail-lending one, from serving India to serving Bharat with 300+ branches in 24 states and UTs and 1 million + customers and staffs well-equipped to do retail business.

-

Slowly, the share of retail business grew from 12% in FY21 to 36% in FY22 and then 50% in FY23, helping to earn better yield and increasing profitability.

-

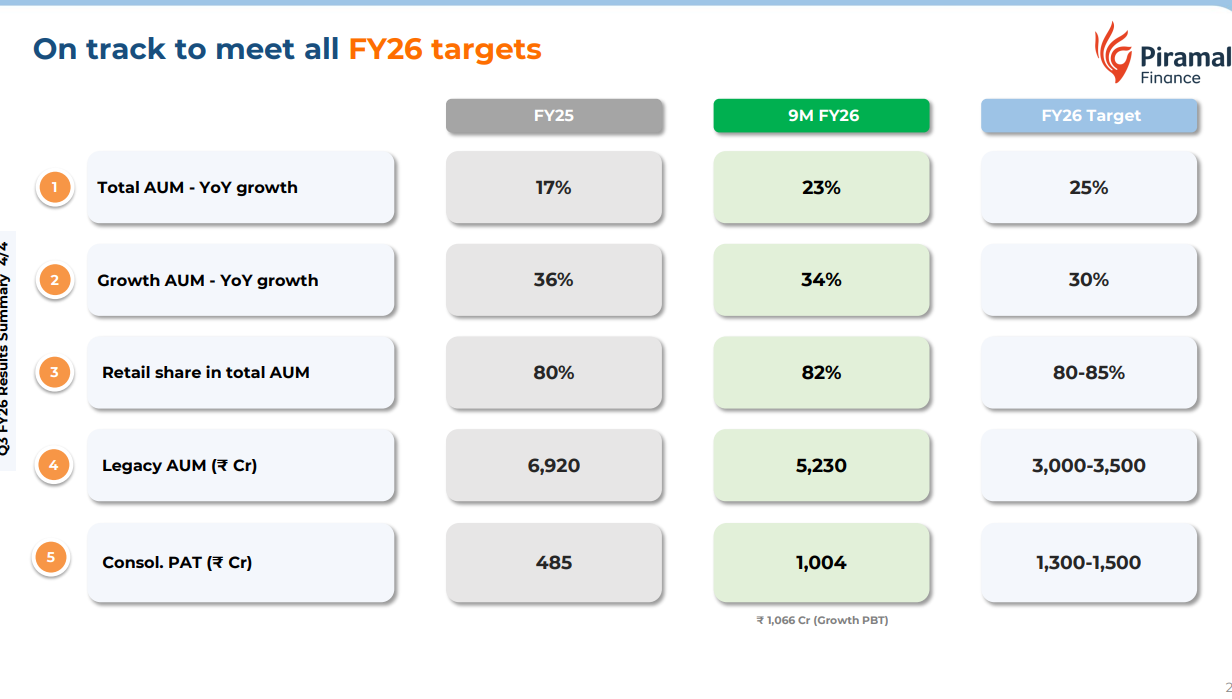

In the mean time they are winding up their legacy book exponentially from Rs.43,175 cr in FY22 to Rs.6920 cr in FY25 and guiding to bring it down to Rs.3500 cr by FY26 end.

-

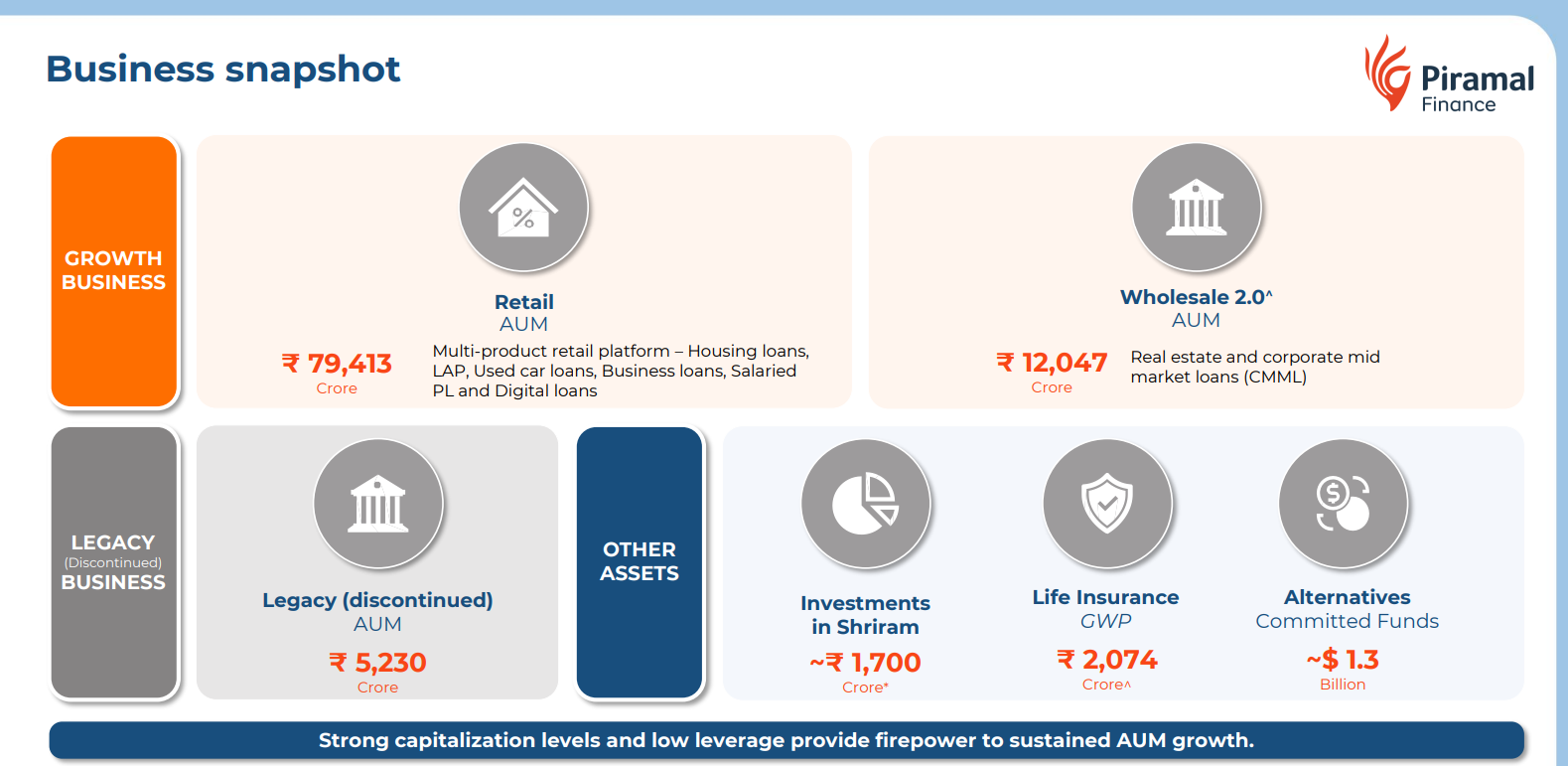

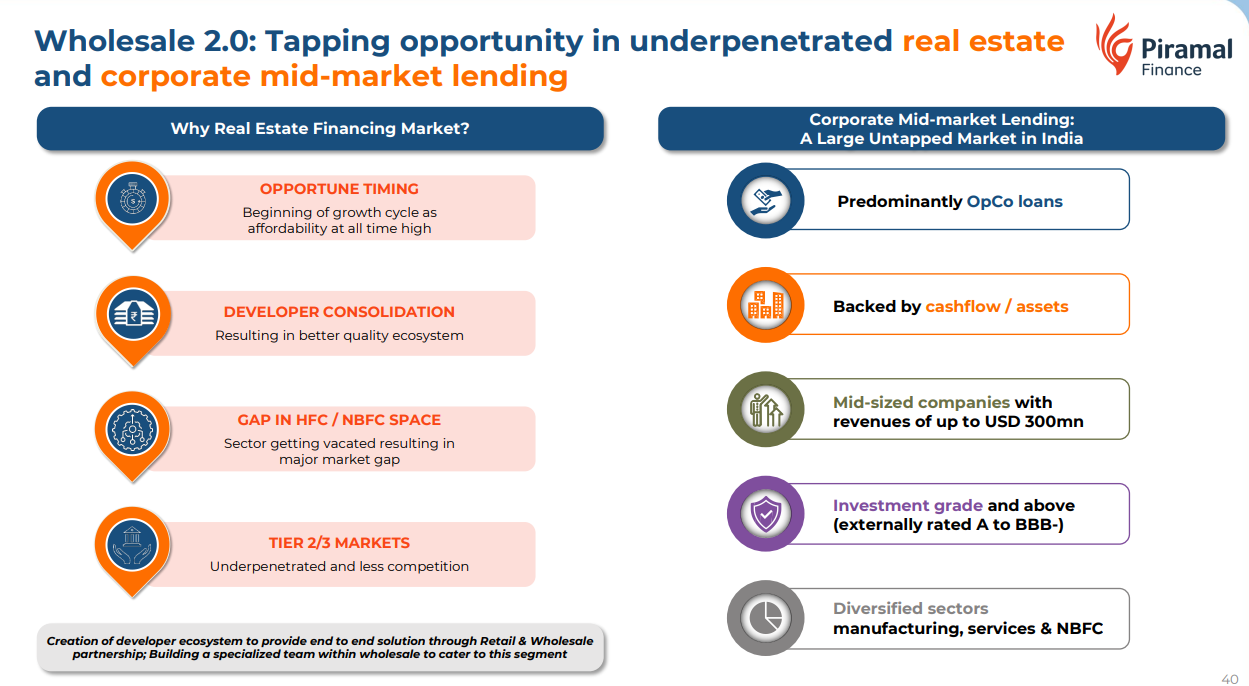

Along with the focus towards retail, they have also started wholesale 2.0 where they do late stage real estate financing to small developers and financing small-mid corporates.

-

The leagacy book: growth book has already gone below 5% with the retail portion of the growth book being more than 85%.

Merger of Piramal Enterprises with Piramal Finance:

-

PFL is classified as an “upper-layer” NBFC, which carries a mandatory Reserve Bank of India (RBI) requirement to be listed by September 2025. The merger achieves this listing by folding PEL into PFL, creating a single, compliant listed entity.

-

Upon completion, the combined entity will benefit from a significant tax shield of ~₹14,500 crore in assessed carry-forward losses. This is expected to provide a substantial boost to profitability by aligning Profit Before Tax (PBT) and Profit After Tax (PAT) for several years.

Way ahead:

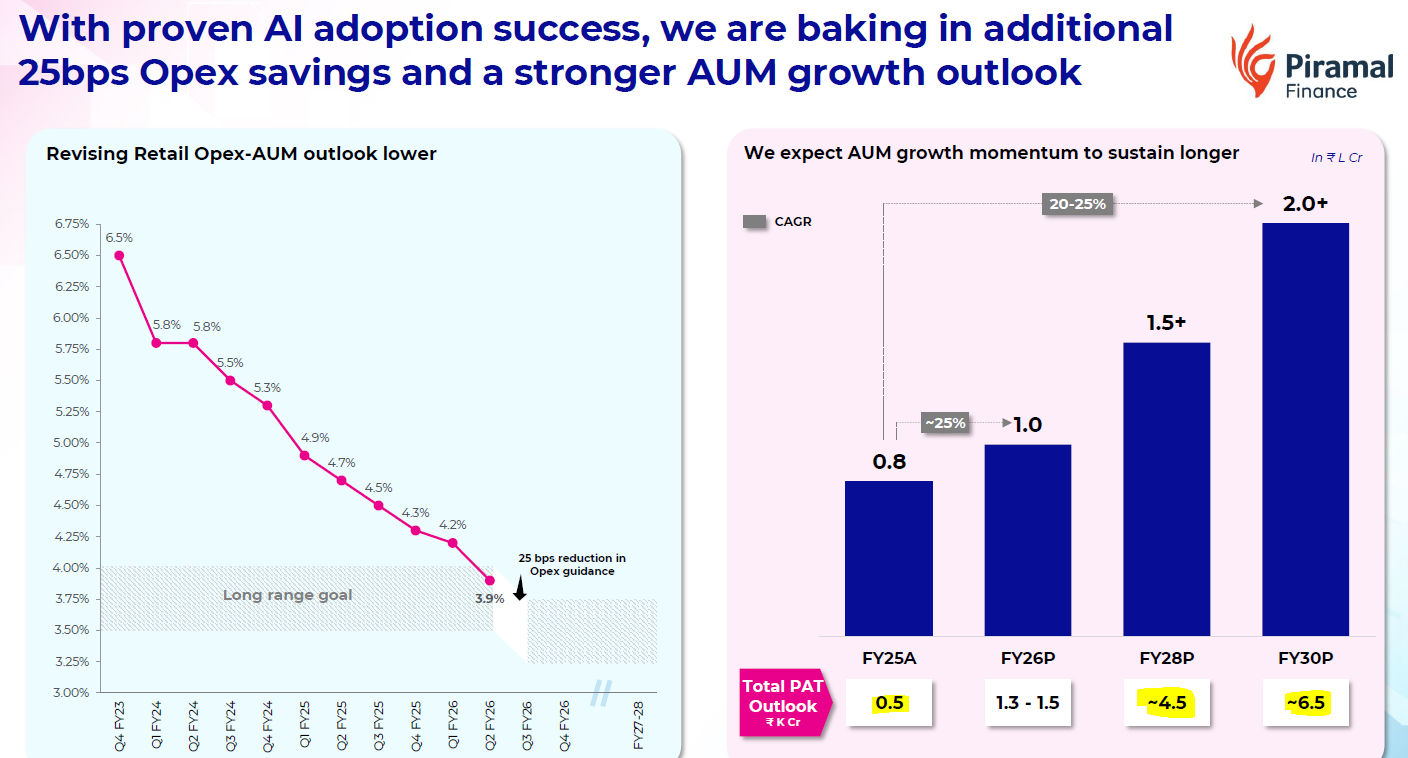

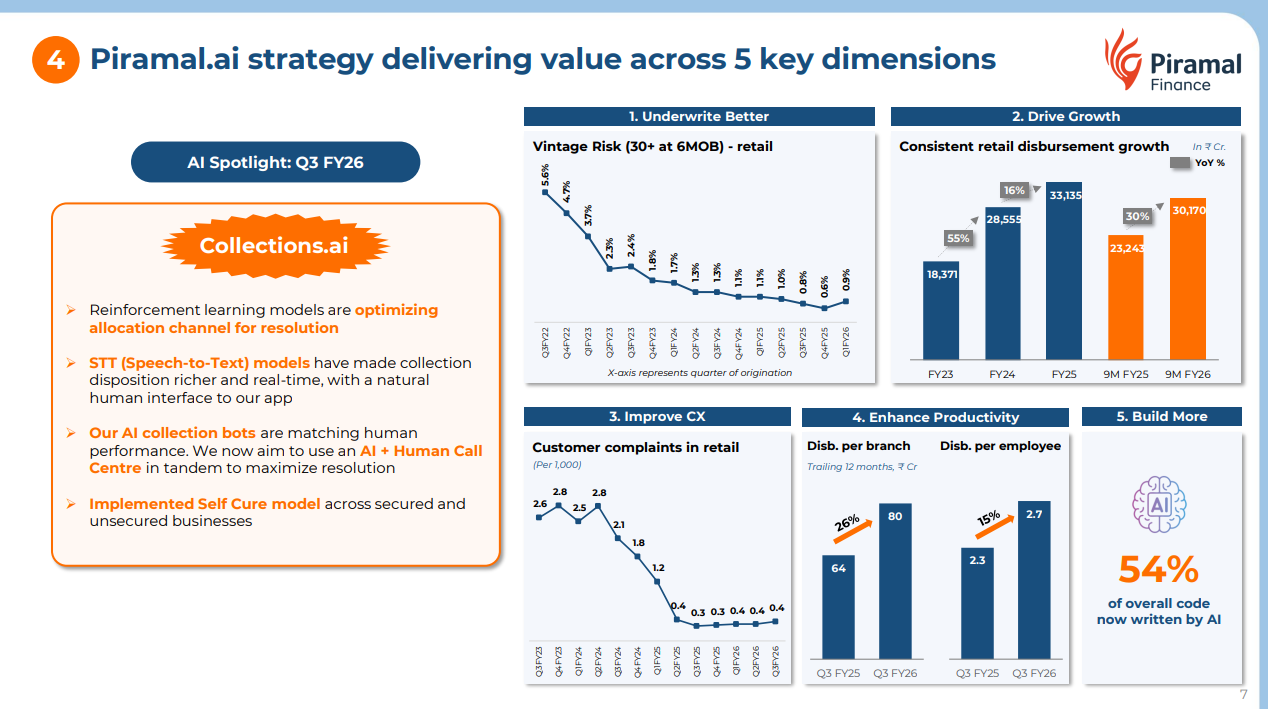

- Their inhouse AI piramal.ai helping them underwrite better, bringing new businesses, reducing complaint, enchancing productvity.

-

In Jan’26, Crisil assigns AA+ to long term debt, which signifies thier journey from the write-off saga.

-

The merger will create synergy with unified focus and a tax shield which will help the bottomline.

-

They are on track with their all parameters- be it growth, growth in high yielding retail busniess, winding down legacy AUM.

- Although they have course corrected in the wholesale 2.0 by catering to different mix and brining down avg. ticket size, we still have to keep an eye out to the part.

- Whether they are being more aggresive and compromising the customer quality in the way.

Guidance:

**Invested and baised and hence avoided doing valuations. DYOR.

5 Likes

For folks who are considering Investing, All the turnaround related story is fine- Ask yourself:

- Are you okay with a struggling finance business paying *Royalty* to it’s promoter ?

- What is the Royalty being paid for ? Any *IP* capitalised at promoter level or is it just promoter greed ?

- What are the other respectable Non-MNC companies that pay *Royalty* to it’s promoters?

Promoters prioritising their own interests before the company’s is a clear sign of Family Business mindset. Just glad that this is being done transparently or Maybe not :P .

Been tracking this story for more than 5 years now, over time there are many hooks to this story- with DHFL acquisition, Mention of Jio partnership, Management change, Retailisation of loan book, Demerger, Non-core exits , Defining ROA targets etc. after all these, i feel this story is not worth participating in.

Views are personal- take it with a pinch of salt and please DYOD.

6 Likes

Even Tata Group takes royalty from its companies for using the Tata name which is like a brand.

If you remove the Piramal name then it’s quite likely that this co may not be able to get the rating it gets and thereby the relatively lower cost of funds…also the other benefits like attracting talent due to Piramal name.

Pls explain what’s wrong with the points you have listed…would help understand your decision better..thx

4 Likes

Although, Piramal name has helped the business survive and move forward. In finance, trust matters, and the brand surely helps with ratings, lenders and even hiring people. My concern is more about timing. This is still a company that went through a tough phase and is trying to stabilise. As shareholders, we have already seen dilution and many changes. At this stage, I would personally prefer cash to stay inside the business and help improve returns, rather than flow out as royalty. Not saying brand royalty is wrong. we just want to see clear benefits in numbers — like lower cost of funds or better ROA — before feeling comfortable with it.This is simply how I look at turnaround stories. Others may see it differently, and that’s okay. Happy to be proved wrong.

2 Likes

- Comparing Tata’s “Brand Fee” arrangement to Piramal’s Royality arrangement is upto one’s own judgement. Personally, I don’t see them to be similar.

- Rating & subsequent lower cost of funds argument might be true. Maybe top tier NBFC’s like Bajaj Fin should also do the same- but they aren’t, that’s where the difference is.

Maybe i’ll add couple of points

-

This publicly listed finance company used to own ship ,helicopter on books. The numbers might be small but the clarity of intent is big.

-

In Lending business, the scope of things that can go wrong is way too high.

-

Most investors tracking this story from the beginning should ask themselves- where did all the provisions on legacy book go ? what were the valuations at which the provisioned book were downsold ? there used to be hardly 200 accounts to which piramal had 50k exposure few years ago and these are secured assets with multiple times collateral with promoter guarantees. The degree of LGD “Loss given default” post default is supposed to be less but that’s not the case here.

As a retail investor, there is no point in digging deep and beating our heads on such points.There are no dearth of opportunities in the listed space. It is better to be safe than sorry.

Investing thesis is usually individual specific, same facts can be interpreted by different people differently. My interpretation is this org is a family business for others it might be different and it’s okay.

6 Likes

Sir…now you have listed an entirely different set of points…my question was - pls highlight the issues with the points you listed earlier:

Requesting you to pls clarify these…thx

- DHFL: Another highly reputed Howard Marks company Oaktree with 200b assets was in the fray. On what basis are you casting doubts on this acquisition?

- Mention of Jio partnership: When and where did Piramal mention this? Wasnt this just media speculation?

- Demerger: What is wrong with the demerger? All explanations were given in detail in the rationale…pls highlight which ones are dubious?

- Non-core exits: Which ones? Shriram’s? Isnt it public knowledge on what happened right from the time Ajay invested in Shriram? Pls highlight specifically what is wrong?

- Defining ROA targets: What’s wrong in this? Are you saying all companies which give target are not worthy of investment?

On provisions/LGDs: Many builder loans led to npa’s for many companies…including the big banks…if PFL did something wrong like siphoned off funds, etc or are you saying they are paying bribes to their auditors/rating agencies who are not highlighting anything…and all the institutional/debt/ncd/stock investors are also unaware of where the loans have vanished…i request u to pls highlight what everyone has missed ie exact facts and figures.

Ships, helicopter: just owning something (which appears expensive) isnt bad in itself unless you know the whole truth…maybe they got a got a good deal like a steal…if he bought an asset worth 10cr for 2-3cr or maybe it came as part of some promoter cashing out…and now if he is using it to save time it’s good for the biz…Angel One promoter owns many flashy cars…doesnt mean he hasnt run his biz well!!!

PFL isnt an NBFC but a Family biz: If this forum starts allowing people to share their “personal feeling” then this forum wud become a joke….pls dont drive it in that direction…

Lastly, if Tatas start charging royalty from their comapnies after having estd their brand over decades….then are you saying it wud be ok for Piramals to do the same in 2040/50 and not now??

FYI…Havells used to do the same ie promoters used to charge royalty from the co…they stopped in 2016…and the stock price went up by 4-5% the next day…means royalty value was part of the company valuation.

All of the above, your doubts/investor’s doubt and concerns on governance issues, biz quality, numbers and their sustainability…everything is in the price/valuation….u cud say 40k isnt the valuation as per your calculation…but from the way you put it, it seems like PFL isnt investment worthy…which is far from the truth.

You have been casting aspersions on Piramal one after the other…thats the easy part…anyone can do that…if you really want to help the community here then pls share something real, factual…and with data….and if you dont have answers to the above in detail and with specifics then I humbly request you to delete your above msgs….it isnt good to paint someone bad without any basis.

Pls dont go by the tone of my language…i dont know polished english…pls pardon me for that…but pls do share real facts and figures…its really important…just feelings, narrative and impressions dont help at all…thx much

10 Likes

Response to previous post,

Sure, I think you misread my post. Never said they are wrong/Bad. Sharing Chat-gpt screenshot for your understanding.

Not privy to any such information. You are asking for answers in a territory which retail investors does’t have access to- If you do, please share the positive feedback that you have from Auditors, Rating agencies, institutional debt holders.

I am questioning how any large NBFC having “Secured book” with real estate receivables that have high recovery potential post default operate at near 0% ROE for 5 years? - As i mentioned earlier, No point in digging deep as a retail investor.

This is music to ears for any promoter :). Sure.

With all due respect, everything you shared here is “your” personal opinion as well. Not many know what’s really happening in the company.

Sharing a “view” with a tag as “Personal opinion“ meant to be a responsible way of sharing information & not to hurt folks who are holding the bag. Seems like it happened anyway.

I reiterate my view on this.

Seems like you are pro-royalty for the Piramal family. Royalty by nature is not wrong & is regulated. Tatas charge it due to a massive amount of spending on brand building globally(also IPLs ![]() ). My questions on royalty are more from a ethical standpoint especially when the house is not in order.

). My questions on royalty are more from a ethical standpoint especially when the house is not in order.

Thanks for sharing good to know.

“Havells promoters stopped taking royality because of whatever reason”- let’s celebrate that.

On valuation, I never valued the company here. I am not saying that it is above or below fair value. I come from a school of thought that when something doesn’t smell right, don’t bother not worth valuing.

One might feel that low P/B is a good bet. My 2 cents coming from a NBFC background,

In NBFCs wealth is created from two variables 1. ROE 2. Dilution at high P/B.

Strangely highly valued companies with good governance, clear growth path tend to create more wealth than others across cycles. even more in bad times.

Respectfully declining the ask to delete the post.

This forum is not just for cheerleading companies one owns. my posts are intended to help out fellow investor.

Have tracked for years, invested, exited the company- I remember the disappointment after every quarterly results, many broken promises by the management. If most people don’t find value in it, let the community decide and downvote the post :)

No further explanations or debates from my side on topics that are already covered. Happy investing :)

6 Likes

When it comes to Royalty piramals charges on Piramal Finance and Pharma are absolute loot. They don’t deserve this royalty. They didn’t build any niche like Tatas. No customer considers Piramal as a valuable brand while taking loans to be deserving royalty. They are not building any wealth to investors from several years. They infact destroyed enough of wealth in the last 7–8 years. Still happily charging royalty for the experiments they are doing in the company.

4 Likes

Here is Tata’s SEC filing. It says they charge upto .25% of revenue but this amount shall not exceed 5% of Annual Profit before Tax. Am I reading it correctly?

AUM Book - How the clean up happened in last 5 years

Risk recognition:

Chairman says:

Middle East tensions, energy disruptions, higher input costs, liquidity tightening and credit risks remain concerns.

CEO says:

Global events since March raise an important question mark on where credit costs might head in FY27. We are not sure credit quality remains this benign.

Mgmt guiding 25% growth in FY27 & 28. Very ambitious

Current:

AUM = ₹1,01,230 Cr

Target FY28:

₹1.5 lakh Cr

Impact of AI:

-

300 engineers

-

200 AI scientists

Lead to

-

Disbursement per branch increased ₹66 Cr → ₹79 Cr ( despite increase in brach count)

-

Disbursement per employee ₹2.4 Cr → ₹2.7 Cr

-

Customer complaints reduced

-

by achieving through Customer proof analysis, Fraud detection, Collection priority listing, and many more such nuances are improved either by time mgmt and risk reduction. Efficiency is good.

-

Given their AUM target, Equity raise is needed by FY28 to meet the CAR. Piramal is known for rights issue to reward shareholders. Lets hope, we get rights.

-

Tax Losses:

-

Piramal says:

We have accumulated unabsorbed tax losses of ₹24,281 crore

-

It translates to

-

Potential tax shield: ₹6,112 Cr

Recognized DTA: ₹2,136 Cr

Unrecognized DTA still available: ~₹3,976 Cr equivalent tax benefit potential.

-

Mgmt recognized these in a calculative manner. It says " only the portion they believe can be utilized through future profits". Very good governance indeed.

1 Like