In my view, the equity value of pharma business should be higher than 15,000 crs. By valuing at 15,000 crs, we would be valuing it lower than what Carlyle paid.

Carlyle valued the 20% equity stake in pharma business at 3500 crs (total equity value 17,500 crs) in June 2020. This was 15 months back when the overall market valuations were lower, Pharma business revenues were lower than what they are now and more importantly Piramal was in distress. All 3 factors are favourable now.

Valuations are hugely affected by demand and supply of capital, The valuation of most companies from that point in time, cannot be considered as fair/correct/wrong, as almost all of them have doubled from those levels, except ofcourse ITC

For example, consider this - Carlyle bought Sequent also @86 Rs per share around the same time (within a month), was that Valuation correct? Given that since then Sequent has gone to 330+ & then back to ~220 Levels from there, still ~3X from Carlyle’s acquisition price.

With the sale to carlyle PEL was looking to increase the Cash position and be ready for the any uncertainties associated with further COVID lockdown, just 2-3 months into it.

For PPL let’s consider the 3 verticals and all of them should be differently valued.

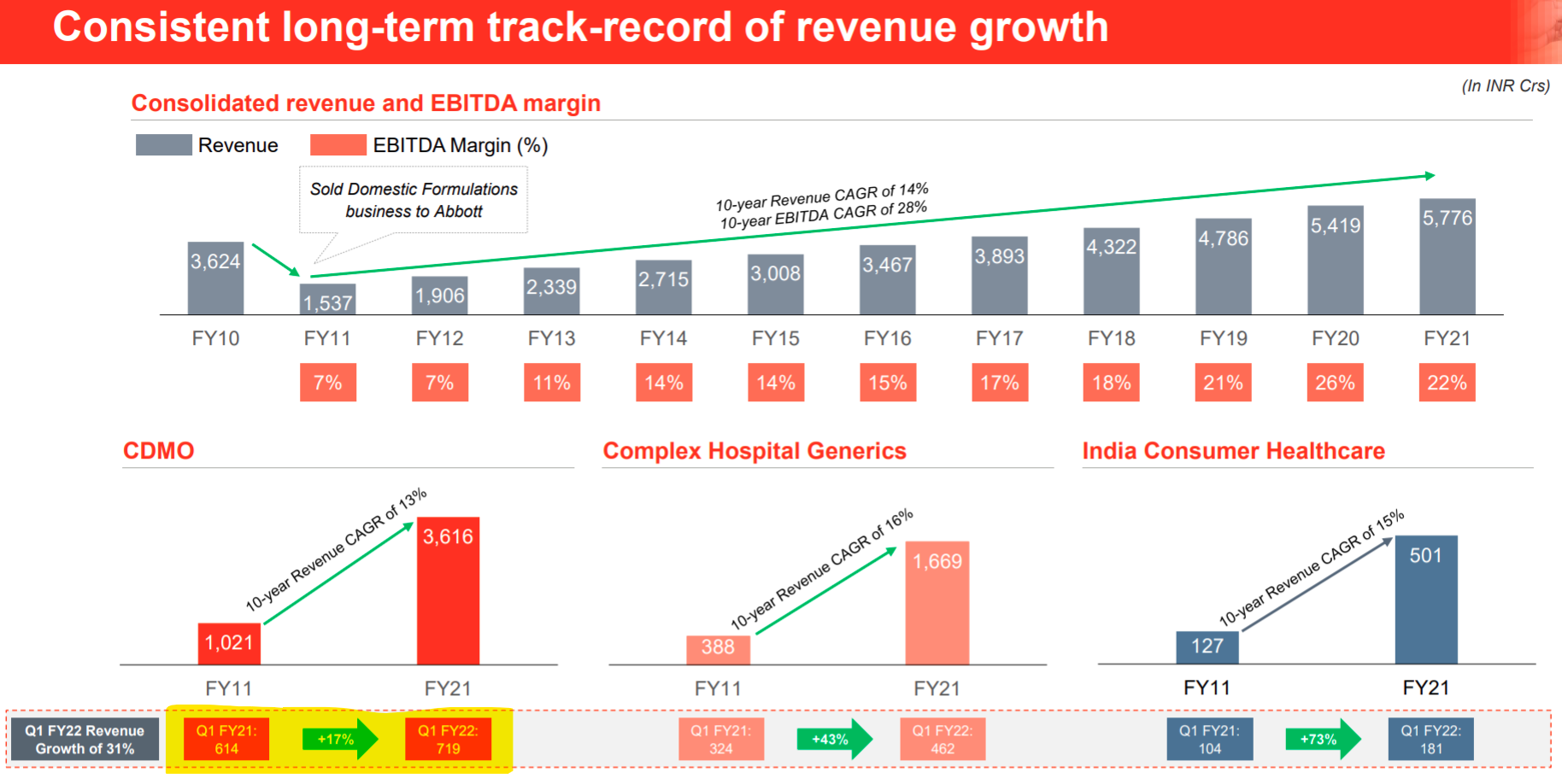

CDMO 62% of PPL - The CDMO business can be very closely equated Syngene (Diverse client set) and Suven Pharma (Mostly NCE clients) and is the best of the lot due to excellent industry structure, pricing, capability, etc.

Syngene at 30%+ OP% Trades at 32X EV/EBIDTA and 10X Sales

Suven Pharma at sector leading OP% of 44% trades at 27X EV/EBIDTA and 14X Sales

PPL, assuming the 62% CDMO business gets at industry level margins, 8X sales conservatively for 3.6 K Crs should be about 29 K Crs

Complex Hospital generics 29% of PPL with (assuming) average margins and Consumer healthcare 9% of PPL with (assuming decent margins) should be additional ~5 K Crs atleast, taking at 2.5X sales

This will gives us 65-67 K Crs M CAP which is the almost similar to the current Market Cap. There are quite a few upsides which will add to these like the hemmo and specialty chem balance acquisition, recovery in Hospital generics and consumer health division, JV with Allergan, etc

OfCourse I may be completely wrong about the above conservative valuations but Market will price the businesses as per their growth and profitability. Once we have the Q2 numbers, there will be more clarity on each business, their performance and consequent valuations.

I expect at-least 20% per year growth in PEL consolidated bottom-line even from current levels with the growth levers & capable management in place for this decade.

Pharma business might have more valuation, but I have judged it purely from nos. perspective which were avlbl on latest concall & Carlyle deal : -

Carlyle deal happened at EV of 20,300 crs. with Debt of 4k, so comes the mkt cap of 16k at which Carlyle bought.

The debt now is 3k crores on pharma & the stake is 80%. So 20k - 3k = 17k & its 80% = 13.6k with some MOS. Now plz bear in mind that I maybe anchored at undervaluing it bcoz of 3 factors :-

My positn buildup started whn mkt cap was 38k & it was more of a demerger arbitrage which now seems to be a case of getting a good business at fair price. So, my consideration here is on averaging up frm my mkt cap of 41k crs as of now to how mch extra considering I’m expanding my holding period for the same.

I come from old school whr 10X PE was the norm & not 10X sales

The subjective valuation part is very lopsided towards pharma - dont know why bt the same act is repeated by that moneylife article & @Rishu1202. No offences to thr understanding but suppose I carry the same subjective analysis to PEL. Then, altogether it will become a different ball-game ( nd I’m going to do that in next thread)

Ur views invited both on above conservative valuation & my subjective case for PEL in next thread.

Its good that u brought up competitors’ valuation analysis & Pharma industry insights for ur valuation case. Now, allow me to do the same for PEL NBFC part. The starting point is the Book values : -

For comparison, I choose a similar business - Bajaj Finserv. How these are similar : -

Parent co. of a franchise nbfc - Bajaj Fin vis-a-vis DHFL ( The consumer franchise is estd. & the reason why Piramal bought)

Finserv’s Holding in insurance Biz, Small Housing Finance biz, Some windmills, etc. vs. Piramal’s stake in Shriram cos., DHFL’s Pramerica insurance biz, Alt investmnt biz & other loans biz.

Bajaj Finserv sells at 4.6X Book value, so PEL should, in dat case conservatively be valued at 3.5X Book = 98000 crs. Add to that ur PPL valuation & this is a super duper undervalued stock.

This exercise is taken up by me just to showcase how narratives can stretch the valuations. Not sure wat’s the antidote for it. The best I do is to practice conservatism & make mistakes of omission for now…

Market is valuing today 65000 crs with demerger known from March 20 and in a bull market. How far valuation can be stretched by demerger and other themes. This 65k includes pharma business also. Who bought in lower circuit makes sense to hold now who wants to buy on these stories it is their decision. I would rather wait for a market drawdown to add more.

OfCourse, Valuations are just opinions and narratives and it all depends on the market mood and sentiments, With the kind of bull market we have now, you may even end up getting more than 98 K Crs for PEL or may not even get 27 K Crs if thers is a big drawdown. PE of 10 also is quite high for some hugely profitable PSUs but less at 250+ PE for D-Mart where people are still buying, (I don’t even want to mention the IPOs of the last few months ).

I have also been accumulating PEL since sub 1600 levels just for the CDMO piece and am hopeful about the PPL valuations to play out and increase much further as its one among the top and best players in CDMO in India and globally. Thus, I am comfortable to assign a valuation multiple as per that industry to PPL. There are other global players also in CDMO which trade at much higher valuation range which I do not want to mention. I am certain about the valuations assigned and hope it will trade in that valuation range and more once it starts to trade separately, given the pedigree, industry tailwinds, track record etc. I may be wrong in my valuations but I think this narrative is the reason for having a Pharma lopsided valuation even in the moneylife article.

Although, I can’t say the same about the industry leading position in PEL considering the pending Post merger integration with DHFL, the real book quality, expected recoveries from the written off part (which @AmitContrarianpointed out) etc as I am not an expert in that area. There are too many moving parts in PEL and being a novice, I won’t be comfortable in assigning a high valuation multiple yet and I may sell out PEL once separated, since I would also be conservative where I am not sure about the Industry or the valuations.

But I am also aware that the whole pond is rising and it’s not just me so who knows, maybe your undervaluation narrative of PEL plays out when it starts to trade separately, since we have aligned interests.

I agree, the current valuations are far-fetched and I would wait for a drawdown to add more else will wait for it to start trading as PPL to add more in future.

U’ve pretty much summarized the whole thing perfectly. Nothing much to add there.

To each his own, my story goes like this - Plain serendipity led me to buy PEL at cheap valuation - the world seemed ending at that time & most cos. were avlbl as cheap bets including Piramal. I bought them as a bunch. By the time I came back to review, this became a demerger arbitrage & I held accordingly. And now, the valuations seem past conservative SOTP values too. So now 2 options I am considering

(a) whether to average up & hold - which vl be the case of only buy-and-hold & let business grow in strength & value - This is a tough art which takes time & understanding to develop

(b) Book profits - cash out & leave value at the table & begin search\wait for other undervalued bets - which is a luxury in these times

Is there a way to figure out what prices both the businesses going to list ?

i guess for every 1 share of PEL we will get 4 shares of PPL but how listing price will be decided ?

going by consensus today ideally PEL should list at Mcap 30,000 cr and pharma should list about same price 30,000 Cr

I.e, PEL stock price going to be 1/2 of roughly whats its today : Rs 1300 - 1400 and

PPL will be around - Rs 30,000 cr / ( 23cr shares * 4 ) = around 326 per share.

PEL equity value is approx 30K cr , even at 1X book it should command mcap of 30K cr if not more , like wise say at 1.5X it can be 45K cr.

pls do let me know if this isnt right way to look at it

Shriram group companys reorg. Although Shriram group is denying these reports, it is nevertheless interesting. If the events turn up as per the story, PEL might get few thousand crore sometimes in next year or two as these activities take time.

As per the article

“RBI’s discomfort about listed shadow banks owning stakes of over 50% in insurance businesses and was one of the reasons why the Shriram merger plan was called off last year”. Going by the same logic PEL will eventually dispose off DHFL’s insurance business sooner or later.

Yes but i think this has grown in value -

Shriram Capital is being valued at Rs 25,000 -28,000 crore = 20% of it = 5600 Cr + 1446 (Shriram City Union Finance Ltd * 10%) = Rs 7046 Cr

but i think there are other investments too, somewhere they mentioned 11000 Cr of investments i remember but can’t recall the source.

).

).