@BudFox & others :- This was in the resolution doc published in Jan after approval. While m not able to find entire pdf now, pasting below related articles and the VP post link where the screenshot was pasted:-

I am unable to find an official plan document approved by the Committee of Creditors. As per some media reports, there were a few proposals on which voting was conducted. We don’t know which one got voted as successful. Is it possible that the snapshot you shared is a plan and not the plan ?

Media reports mention Piramal’s bid for DHFL to be 37,250 crs. However, Piramal’s Dec 20 presentation mentions the acquisition price to be 34,250 crs. Which one of them is correct?

Small FD & NCD holders would be paid additional amount to the extent of 2% of the resolution plan amount. If the plan amount is 34,250 crs, then only 685 crs would be paid additional. If the value of FDs/NCDs held by small holders is larger, then this amount may not be sufficient to pay all the small holders to the extent of 100%. In that case, all small holders will get proportionate amount which would be lesser than 100%.

NCDs to be issued by Piramal would be of 10 years maturity. At 10% yield, the NCDs should be valued (present value) at 80% of their face value. Hence, the recovery in present value terms would be smaller by that extent.

Is it possible that additional payment is paid only to those holders who were holding NCDs when the company went into IBC ?

If too many people start doing this trade, can the trade become counter-intuitive since the additional payment is capped at 685 crs ?

Lastly, the time delay and legal risk. This is the first case of IBC of a financial company. We don’t know what we don’t know.

I can confirm to a few of ur points whereas on others, I admit that this was a cloned idea for me and bcoz thr wasn’t a significant portfolio sum to be bet upon, my due diligence wasn’t upto this level.

Anyways, to answer some of ur questions : -

The NCDs will be settled as per a record date, that’s the reason why they’re traded currently. At a decided date, the trading will stop, much like equity bt here the eventual holders will have a claim & a dues payoff(hopefully)

The trade becomes crowded - Yes this will happen as the resolution nears & the discount will close accordingly. Those who bought @ 70-80% discount can then take a call eventually depending on hoe much time has passed

Yes, there are delays & legal risk. But thr are motivated parties who want to settle the issue at the earliest - IMO, Piramal will also prefer to go for demerger post takeover only. So, it all comes down to IRR. a 2.5X in 2 yrs isn’t a bad return in my view.

All-in-all the idea of default bonds, however enticing, wasnt a scalable one, hence the reason I diverted attention to investment into Piramal equity.

For further clarifications, I have DM’d you the source frm where I cloned this idea. He has the details regarding the plan & will hopefully be better able to clarify your concerns.

I appreciate your point that since the idea was not scalable, you decided not to spend a lot of time on it. The reasons I decided to dig deeper were (1) it was an interesting problem to think about (2) One never knows. If one digs deep enough, something interesting might come up and the idea could then become scalable (3) settlement of bonds through a bankruptcy process in India is happening for the first time. Following it and doing in depth work may add to the knowledge repository and possibly be handy in future.

To your points I would say this

I agree that NCDs would be settled as per a record date. My question is about the additional payment (to the extent of 100%) to the small bondholders. Would only the small bondholders that were bondholders before DHFL went into bankruptcy get the additional benefit or people who buy it even now ? Thinking about it from a rational point of view, the people who suffered pain should ideally benefit from the additional payment. There has been a case precedent (not exactly same but on similar lines).

RayBan India was bought by Luxottica. An open offer was announced at a particular price. SEBI disagreed with the price and directed the acquirer to revise the open offer price upwards. The matter went to SAT and then to the Supreme Court. Took a long period of time for the matter to be decided. Finally, the open offer price was revised upwards and the acquirer was also directed to pay 10% compound interest on the revised open offer price to the shareholders. However, the Supreme Court directed that delayed interest ( which had become quite substantial and almost equal to the open offer price) would be paid only to the those shareholders who held the shares on the date of the original offer and continued to hold the shares till the matter was decided.

If the returns were 2.5x in 2 years, of course it would be a wonderful idea and there wouldn’t be a reason for any concern. My point is that 2.5x in 2 years is just one of the possibilities. And we should think in terms of probability. We would all agree that it’s not a 100% probability, nothing is. My sense at this point of time is that the probability of the small bondholders getting 100% of their principal is way lesser than 100%. It doesn’t mean it can’t happen. It’s just that the chances seem lower in the light of the available information or rather the lack of it. We should think in terms of weighted expected realization and then see if the trade looks attractive.

@BudFox ; Without going further astray, I’ve taken note of ur (1) above & vl keep a lookout for further info regarding this.

Regarding (2) which I’ve factored in my calculation & extending this to bring focus back to Piramal - my view is that on one hand Piramal mgmt vl prefer to separate the 2 businesses as early as possible, more so with Carlyle in the picture. However, on the other hand, they vl also prefer to list the NBFC business post merger of DHFL. So, all in all, the DHFL settlement & Piramal demerger shouldn’t take more than next 2-2.5 yrs.

I also invite others’ views on Pharma valuation with reference to that moneylife article. Although the valuation view point mentioned thr was bit extreme, with comparable cos. valued at 7-10x revenues. Basically, the question is wat’s the impact on valuation of Pharma business in last year post Carlyle stake sale.

Expect this to complete in the next couple of months for NCLT. May take 2 months or more than that, depending on NCLT process.

Once this happens, PEL can give more clarity on demerger.

Financial Service:

GNPA increase due to movement from stage 2 to stage 3. And due to reduced loan book size.

Two of this account will be resolving in Q1. One of the account we have fully recovered.

3000 cr of provisions in Fy 21. Only used 10% of it and 90% of provision is intact. (Not sure what it means)

NII- yields on the whole sale is less than retail.

Even if we have grown at 25 CAGR in the next 3/4 years, we will not need capital.

Omkar Sales- Restructure to address potential IBC issues. We will not accrue interest in this. This was done in Q3.

- We will master developers for this property. We will sell it in the market.

- Andheri east property-

- We had envisioned- LOI. 67 lakhs sqft.

- Group decided to take cover land (100%). The land is not developed. We will split the land and give it to individual developer. The current value of land is far more than the loan.

- Monetisation process begins in FY 22/23. Get the money, and hopefully, we will get additional money also.

- Omkar exposure 1300 cr.

Lodha Exposure-

March 3300 cr- March 21- 2637cr.

1500 cr SPV_ Fully ready investory.

1000 cr - 431 cr repaid in April-

Total exposure 2150 cr (as on April).

RE Sales:

One time charges due to amortisation introduced in budget 2021. Future amortisation is not allowed as tax-deductible in future.

Supreme court decision (compound interest waiver) has impacted 75 cr . Hence the NIM looks weak. This, along with Omkar charges, has impacted the number.

Developers performance- April sales are happening- our developer sale- 2 X times of pre-Covid level.

- Collection for April 750 cr- (Normal)

- Dip in construction activity in May.

- Watch the construction. Our focus should be on construction not on sales.

- it was far far better than Q1 last year.

Slight increase in GNPA.

Pharma

Developed markets are opening up.

40% of CDMO order book is due to integrated loan book.

Largest fluorene based product in the US in 3 and 4th quartes in the US.

Loan term growth rate of 15%. This year growth shall be better than that.

-Pharma Capex- Fy22-23 higher Capex- Avg of 90-100 million capex over two years.

Margin on hospital business is higher.

Carlyle - Upside- It is not likely to happen due to the slowdown in the generic hospital business.

CDMO will grow faster. 15% organic growth and acquisition will be in addition to that.

CDMO Development 35% three years it was 11 %. (I presume this is early-stage product development)

We have been talking to Hemmo for last 3 to 4 years. A lot of peptides are injectable. API was generated by Hemmo and PEL used to fill it.

- Will invest in capacities. They did not have the capabilities to increase it earlier.

- Due to size, customers were unwilling to give order to Hemmo becauase they were small.

Unallocated equity: 11,000 cr (Book Value)- Only difference will be Shriram investment. Other than Book value= market value.

Pharma business does not need any equity.

FS will not require any equity for 20 CAGR.

We will no allocate money.

Currently, there is no plan to utilise that.

It could be a new business or acquisition in FS or pharma or new line of business.

Note: I have scribbled these note during the call. Some of the info could be incorrect/wrong. Please refer to actual con call.

Piramal had offered upfront cash of Rs 14,700 crore, including cash on DHFL’s balance sheet, and a deferred component (non-convertible debentures) of Rs 19,550 crore.

Question: Wouldn’t FS use unallocated 11,000cr for DHFL acquisition?

“…the resolution plan approved by the committee has assigned a mere Re 1 value to the estimated Rs 30,000-Rs 40,000 crore swindled by the Wadhawan brothers…”

Once demerged, the future of Piramal Finance will largely be determined by how much of these funds flow into the company.

NCLT is doing it to ensure no offer is rejected without proper consideration. I don’t expect any new decision from CoC. But this will curb any further challenges once NCLT clears it. This news may delay the final decision by a month or so. So wait continues…

Global life sciences firm Bayer on Friday said it has launched its Consumer Health division in India comprising 10 brands across the categories of allergy, dermatology, nutrition and analgesics. These brands include Saridon, Supradyn, Becozym C Forte, Benadon, Alaspan, Canesten and Bayer’s Tonic. These products will be manufactured locally in India, Bayer said in a statement. “The brands Saridon and Supradyn licensed to Piramal Consumer Products division in the past, have been transitioned back to Bayer’s new Consumer Health business at the end of the licensing agreement term. Piramal will continue to distribute these brands for Bayer Consumer Health in India,” it added.

Saridon is a significant part of Piramal’s OTC business. I think it will be a big loss.

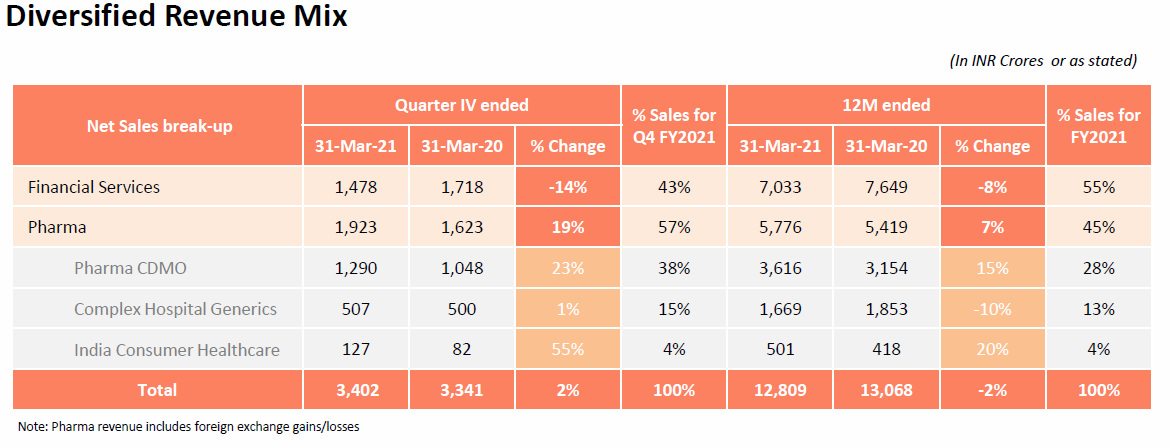

As per recent investor presentation (snapshot below), Indian consumer healthcare division is just 4% of overall revenue . Even if we assume Saridon/Supradyn forms 25% of this division, it will makeup only 1% of the company revenue.

So I expect hardly any impact on company’s results due to this change.

With real estate sector looking up and old pending issues getting resolved , DHFL acquisition would be final piece of the puzzle (which may take another 3-6 months). Once that done, I expect company to regain its glory and continue on the path of 20% + CAGR growth legacy it has built over 25+ years.

Disclosure - invested and forms part of my core PF. No transactions in last 6 months.

They fought hard to take it out from the banned list of medicines.

And they had plans to release brand extensions.

Disc. Invested. Highly interested in Piramal Healthcare. Appreciate the financial vertical too, but maybe will keep only the healthcare vertical after the demerger.