IT Business

The DRG business was bought under the premise of entering and scaling a lucrative Data & Analytics business focused on Healthcare. As a practitioner in this field and catering to the same sector I can definitely confirm - while being lucrative it is extremely difficult to profitably scale this business unless you are not based in the active developed markets, mostly the US and Europe. Unlike IT outsourcing this is a very local business. PEL brought DRG upto 24% EBITDA level in the last 8 years and now under the new owners (Clarivate) the same business will be monetized at much higher level (close to 40% EBITDA level) making the deal EPS accretive for the new owners.

The IT business was a drag on PEL’s consolidated numbers and they were trying to exit this for quite some time. I believe the exit valuation (5X Sales) is decent and provided a return of 2.3x on the core equity they had put in (in INR terms) over the close to 8 years time frame. This business was 9% of the consolidated revenues (H1FY20) with slow to moderate growth.

Finance Business

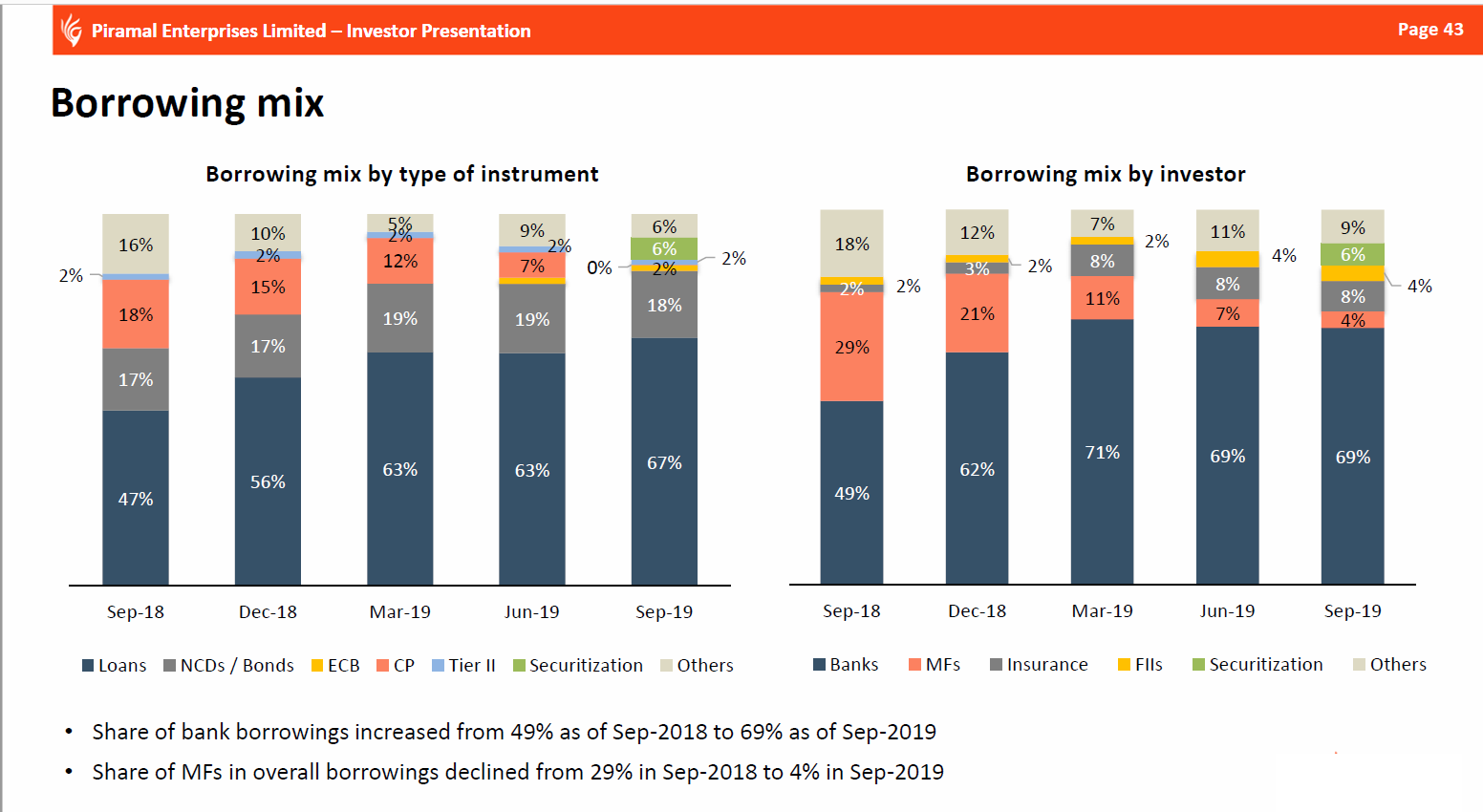

After the IL&FS / DHFL crisis and resulting credit tightening the biggest issue was their short term funding catering to long term loans. PEL had CP based borrowings of 18017 Cr (in Sep’18) which they had to drastically reduce as funds dried up for NBFCs. Most of the fund raised over the past year has gone towards fixing the ALM mismatch and now this exposure have reduced to 1,483 Cr (Sep '19).

On the loan book side, they have kept the loan book size at the same level ~53000 Cr over the last 4 quarters while actively working on changing the wholesale:retail mix (wholesale residential RE exposure is now at 48% of loan book). Share of retail loans has gone up from 4% book, 2325 Cr (Sep '18) to 12% book, 6393 Cr( Sep '19).

There is definitely a lot of stress in the books (the 26381 Cr Construction finance book) which will slowly unfold over the next 3-4 quarters and is reflected in their increased avg. cost of borrowing (at 11%, H1FY20). They will definitely target to amass all the growth capital they can garner and definitely monetize the Shriram stakes to this extent.

PEL has taken some drastic steps to course correct and should emerge stronger out of this crisis. The focus is on expanding the retail book with new head of Consumer lending on boarded and focusing on a technology driven lending (following the footsteps of Bajaj Finance). They are also considering inorganic growth through acquisition of retail and HFC book from distressed entities.

The biggest change in wholesale side is co-origination with banks to reduce the single-borrower exposure and focus towards managing wholesale portfolios and earning fee income.

Pharma Business

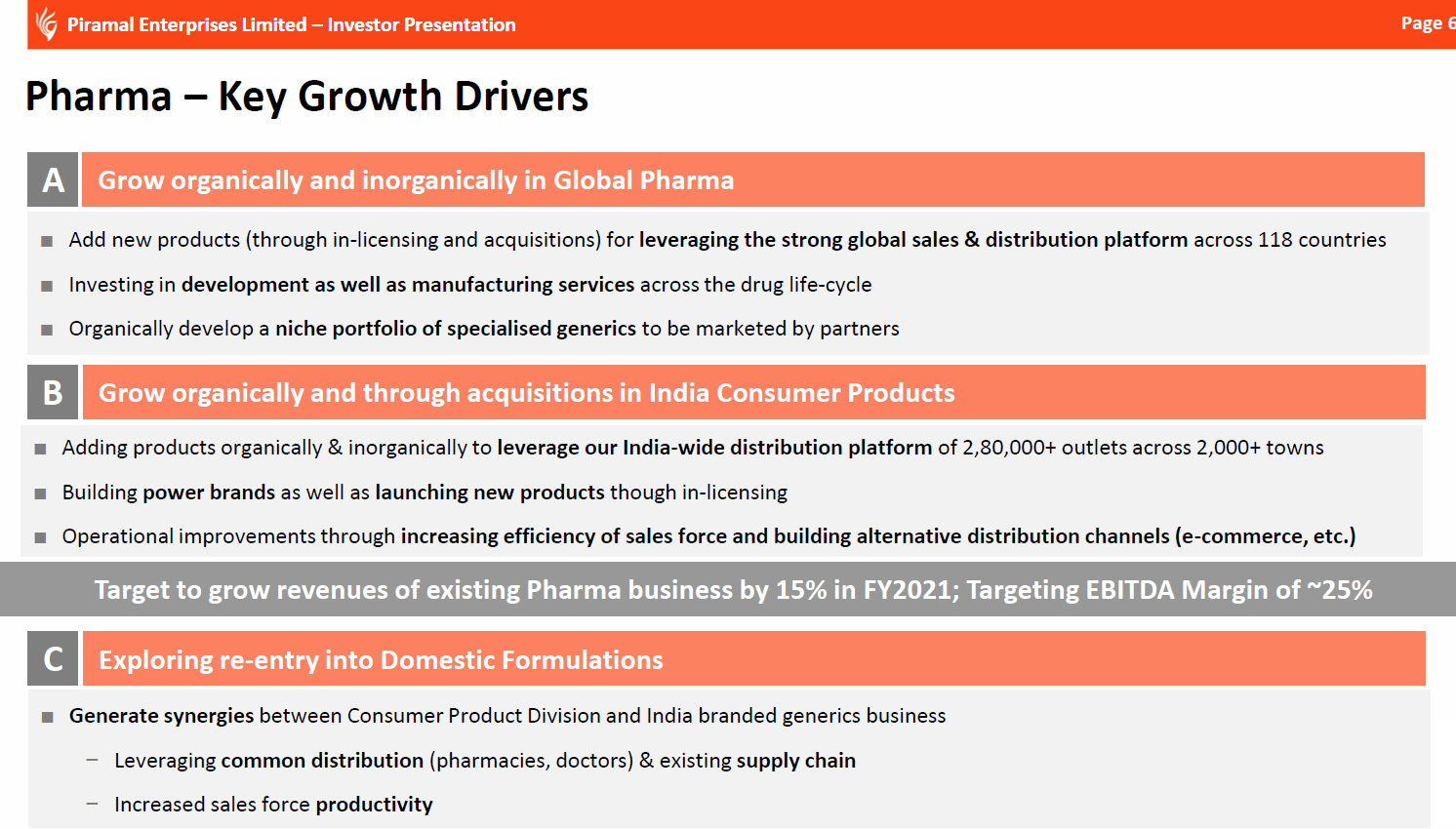

On the Pharma side, both their Global Pharma & India Consumer Products businesses are at a mature stage. While they continue to optimize this growth (in mid teens) and further tune the EBITDA (already at 24%, can go up to 25% by FY21) - it is not a bad time to consider selling a minority stake in this mature business.

Their focus would be to re-enter the lucrative domestic formulations (as the non-compete with Abbott has ended) where PEL definitely has a strong know how and advantage of having scaled this in India in the past.

Overall, the business is at pretty weak juncture at this point, but given the strong support they have garnered from external partners speaks volume about their commitment. I believe PEL will ride this tumultuous phase and come out victorious on the other side.

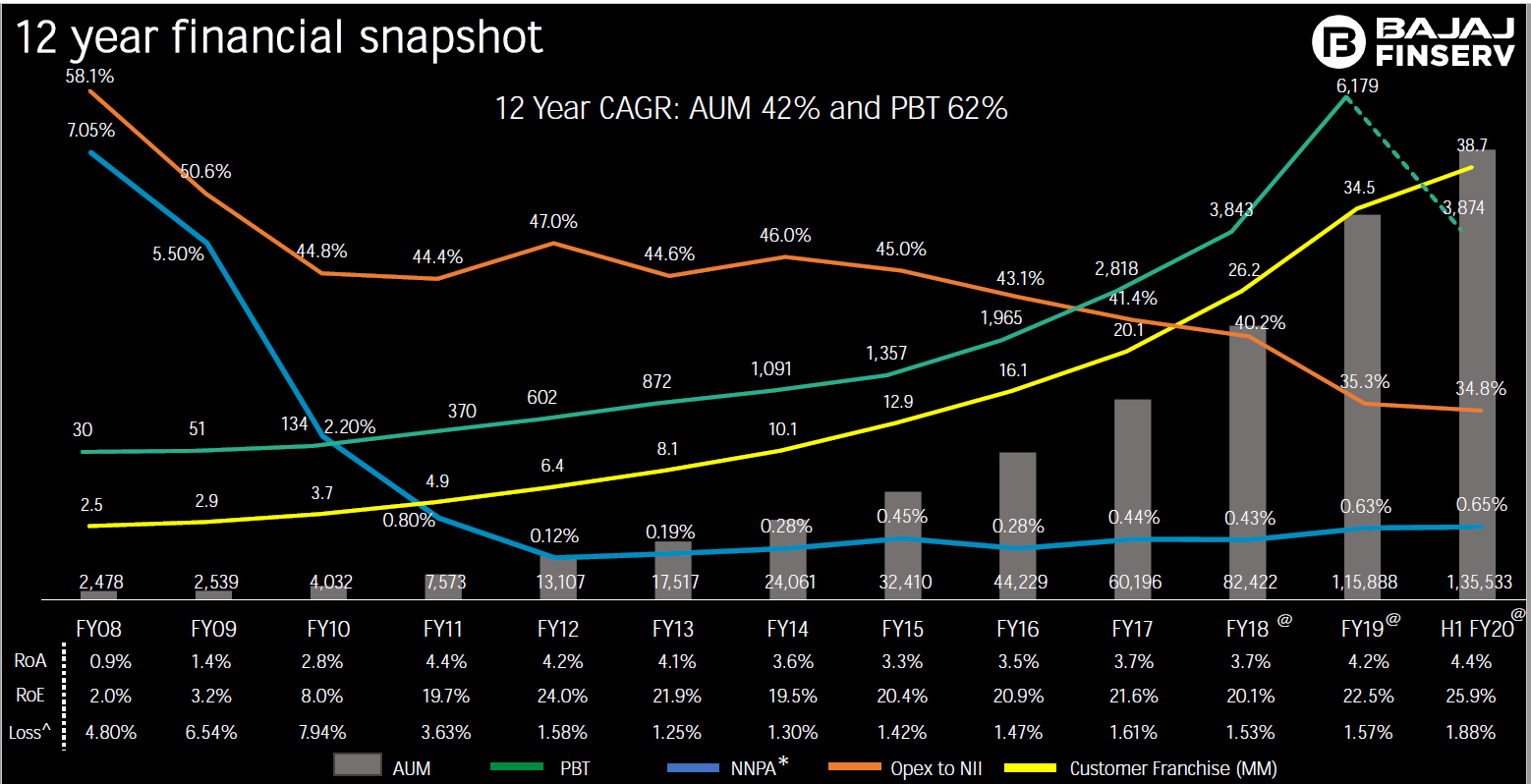

For sake of history, we should always remember the now venerable Bajaj Finance once had a pretty shaky start (FY08-09) with very high NPAs (7%+), but they did all that on a lower loan book and came out as winner over the next 12 years. So the opportunity size in Financial Sector in India is humongous and there is definitely room for a long term play!

Disc: Invested since 2016, no recent transactions, not subscribing to rights at this time.