What does this imply … Is it a way of raising funds or seizing a opportunity considering the inherent value of the business …

Disclosure : invested

Few days back - NBFCs have poor governance, low promoter holding, toxic assets etc etc, But we are different.

NBFC Stocks crash across the board including PEL

Today - Pls don’t paint everyone with same brush. Some NBFCs are critical for the economy. We should not attack all of them. But we are different.

How many biz leaders attack peers at time of their weakest surroundings? It is good that good sense has prevailed on him. He must learn how other NBFC promoters presented the issues for the industry as a whole.

Disc: No holding

Based on the interview to ET, he seems worried if there is large scale run on the NBFC which might in turn cause some concerns even for PEL , at the same time is also scouting for opportunities but probably wants to forewarn the government . there is definitely some more that he might be privy too than meets the eye.

Disclosure : Invested : can’t make up mind to invest further

It seems to me that the market is overlooking pharma side of PEL in this whole NBFC fuelled downfall. Although PEL’s finance business is growing very fast and is now contributing more than 50% of the profits(which may slow down post ILF&S issue) , PEL has a very strong and stable export oriented pharma business. In current rupee depreciation, this business will benefit a lot.

The market sometimes exhibit a tendency to “throw a baby with a bathwater”. The current situation looks a lot similar to that to me in term with persistent selling in PEL.

Demerger at Opportune Time

A lot of data in this blog is just wrong and even does not provide any insights (you could gain that information with just cursory Google Search). For example data like PS of Rs.280 per share and P/E of 8 (you need to remove the one time income otherwise you would make a wrong investment judgement with just cursory reading).

Current year EPS is ~Rs.100 per share (excluding one time adjustments)… and their is no mention of investment in Shriram Group which is worth ~Rs.500 per share.

Even about demerger umpteen information has been given by Mr.Ajay Piramal that its medium term 2 years back (FY20 types).

Hi everyone,

I recently saw one of the ads of piramal realty’s Piramal Aranya, I have observed in the end saying this project is funded by hdfc ltd.

My question is why did Piramal realty chose hdfc instead of PEL , can someone thrown any light on this

Conflict of interest

Just a guess: May be they don’t want to finance certain type of home loan customers.

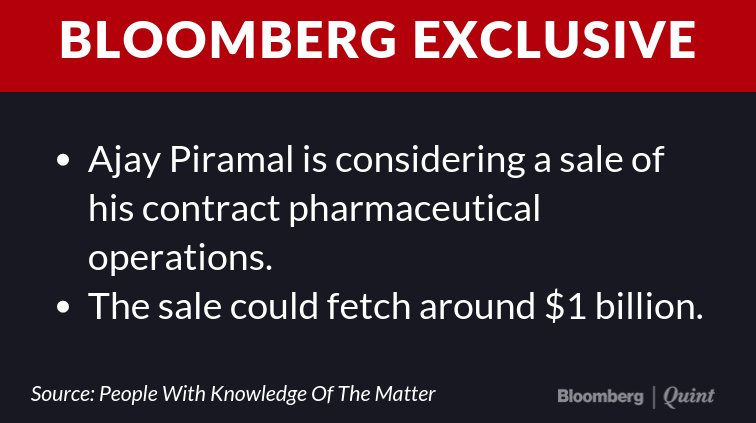

Hi All. Why Piramal is selling their contract pharmaceutical business? What are the plans to use money received ? In fact, I always belived that contract research and manufacturing is a beautiful business and can generate a great profits.

The list is long

NCE Biz - Failed and exited

Imaging Biz - Sold after making losses

CRAMs- Will get sold

IT biz - Struggling

Real estate biz is flourishing since there were so many near bankrupt companies hungry for capital. RE is a sector in which even the leader Godrej is struggling to generate good returns without taking huge leverage.

Disc: No holding

For a novice like me, it sounds like the great capital allocator is sending good money after bad. I see the Abbott deal which happened back in 2011 still mentioned 6 times in the FY18 AR - specially the valuation bit - 9x Sales and 30x EBITDA (search for 30x in FY18 AR). The pharma unit seems to be generating Rs.4322 Cr in revenues and a 22% EBITDA margin which means a EBITDA of 950 Cr. The article also mentions a $1 billion valuation for this unit which means barely 8x EBITDA and not even 2x Sales (Remember the 30x EBITDA and 9x Sales proudly mentioned 6 times in the AR).

Why sell this unit which is a good cash flow generator now and why at such cheap valuations? Why after having raised 7000 Cr in the last FY? To fund more RE ventures? Something does’t smell right to me.

The real problem isn’t in completing a project but in selling out units in a project.

When a project is sold out, then the customer advances more than cover the construction cost of a project.

The final 30% stretch of residential construction can take as much as 60% of total construction cost.

That’s a lot of float that the builder gets to play with.

Finance is only needed till a project sells out to a level where it becomes self sustaining.

PEL isn’t funding construction as much as buying time for a builder so that he can find buyers for his unsold inventory and then he can repay PEL and other lenders.

Successful projects have a public perception of being fully sold out or few units left. The reality can be that a builder is struggling to keep lenders at Bay while carrying unsold inventory.

Now the problem is in almost all markets if something isn’t selling than lowering the price is the rational choice.

Unfortunately this goes against rule #1 of Indian real estate that you never lower prices come what may.

If prices are lowered, builders face unbearable heat from some big investors and they also cause a stampede like effect of sellers wanting to get out in surrounding projects.

No one has ever repealed the laws of supply and demand - Jim rogers.

Real Estate Sale is definitely a problem and industry is suffering from huge unsold inventory - but what i have seen as a real estate professional is that if you ensure “the right product and price it right” you do get good sales velocity (infact i have seen amazing sales numbers). Problem is most builders work on a hunch (they just do not spend enough time researching the type of product which customers want or if sufficient demand is available for that product, pricing it right and ensuring proper design). This problem is more acute with smaller and medium size builders the big builders are predominantly now launching projects with proper market study and they have the team to ensure good sales - Sales team, Marketing team, CRM, Design etc. (These are generally the top 10 developers PEL is funding now!). I am not saying things do not go wrong in big builder projects but there is a clear distinction and if you apply enough due diligence you can avoid funding such projects.

Further I would like to add that people generally hugely under estimate the difficulty in construction - its not an easy to get necessary approvals and ensuring construction within budget and timelines. That’s the reason most financiers even when they see the builder mismanaging the project do not step in. PEL clearly has an edge here and this is what I had high lighted.

Based on the news and the valuation figure, whole pharma is not getting sold. Pharma business has 3 main divisions - CDMO(aka Pharma Solutions), Critical Care( pain management- inhalation, injectable anasthesia etc) and India OTC. Only the Pharma Solutions (CDMO) is on the axe I think. IMHO, this is a low margin business. Critical care and OTC are the future and that is where acquisitions are happening.

in these matters it is best to trust the promoters. AP is a man who

can think far ahead as his track record since the 1980s have shown. As

he harps at every AGM, promoters own 60 per cent in the company so

they cannot afford to make mistakes.

disclosure: holding

shiv kumar