You can either exercise rights-by going to a designated ASBA enabled branch and buy your quota of eligible shares at a discount or renounce your rights by selling it to brokers buying renunciation rights. google this.

I am a newbie to this company’s history and prospects. Just couldn’t get one thought out of my head after reading the product called SURF where people are given bigger loans for lesser EMI (after claiming to check creditworthiness). This sounds eerily similar to SUBPRIME, and sows the seeds of doubt. Besides, this product can be susceptible to manipulation through a nexus between the HFC and any opportunistic real estate investor who repeatedly flips property within a couple of years. Having seen both such forces in action during the US subprime crisis, this product gives me the heebiejeebies. We Indians narrowly avoided a subprime crisis here in India thanks to a few stringent lending norms my RBI, but products such as these could be easily duplicated by other lenders and cause a mountain of bad debt that would implode at the first sign of a softening housing market. I would welcome opinion and inputs from other esteemed members of this forum.

Not sure whether it will happen in one year as suggested by Mr. Mehboob Irani but looking at the past record, I feel it can achieve this price in next 3 years from current price of Rs 2800.

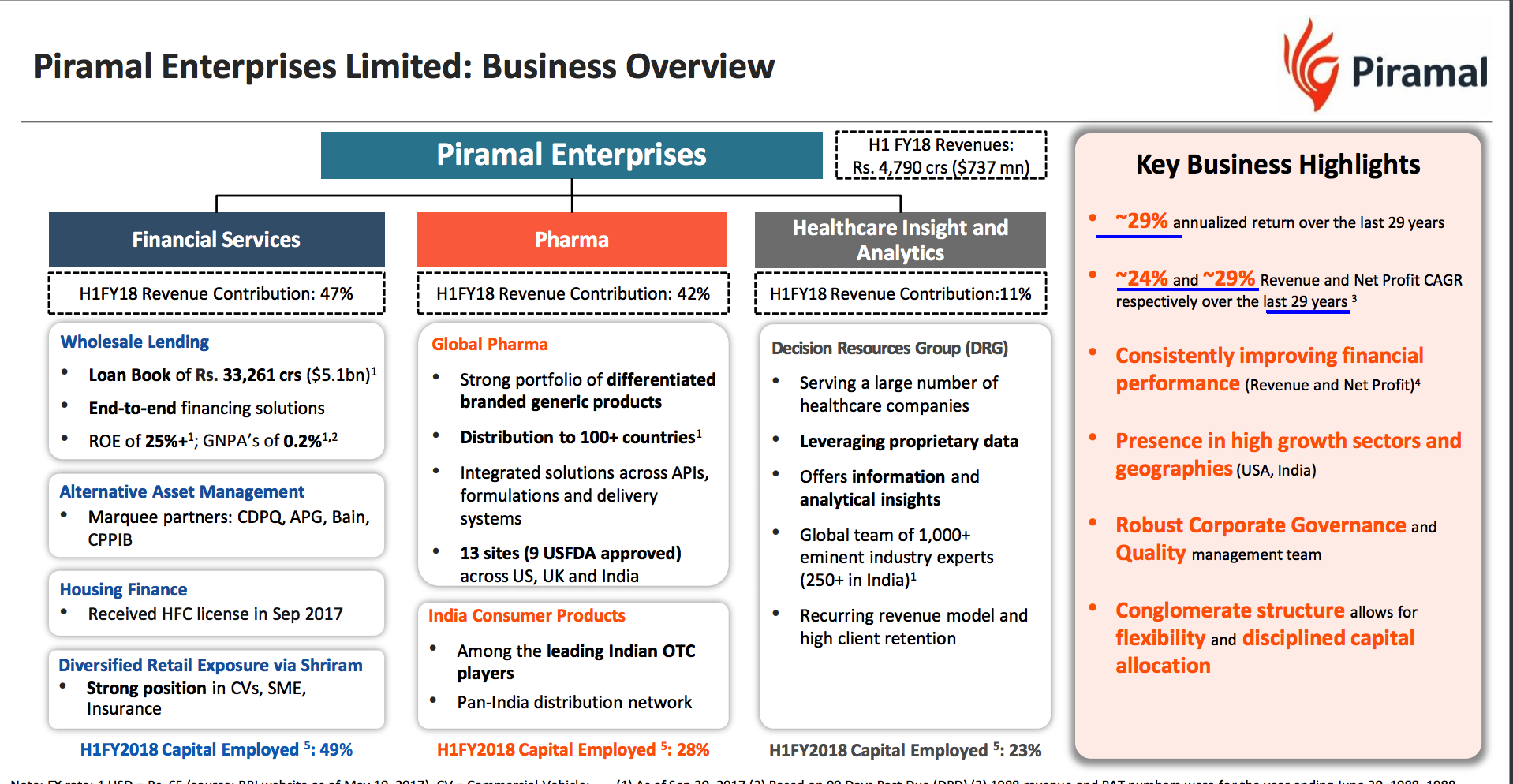

Could anyone please explain the reason behind the abysmally low return ratios? Is it due to some temporary setback, and expected to normalise soon?

Reading March '17 statements, on a NetWorth of ~14,000 crores, they made a profit of 1,250 crores. Given that their Finance biz is generating 25% ROE and usually large pharma companies all have ROEs in the 20-25% range, can we assume Piramal’s ROE has significant room for improvement? If it were lets say 22%, company could have been making a profit of 3000-3500 crores on a 16k crore equity. ( BVPS= ~800, assuming normalised EPS to be 160-200 ) At this price, if my assumption is correct, the stock looks unbelievably attractive.

PEL had acquired few pharma companies and has been investing in the growth of the Pharma business. I would expect the ROE in the pharma business to improve with the growth of the business and operating leverage kicking in.

I also expect the ROE to increase to higher levels, increasing PAT and the valuation. The demerger of the businesses will also help reduce the holding company discount.