Lodha Developers to raise Rs 1,800 crore from Piramal Fund

Sumant Sinha of ReNew Power Ventures raises $100 million from Piramal Capital

Some dated interviews with Ajay Piramal but will help you understand who is Ajay Piramal and what is the value system of the group.It is rare to see Indian businessman talking about integrity, trustee of stakeholders, sharing and compassion etc. He is true follower of Gita…

Interviews like these helps investors understand the promotor’s thinking towards various aspects of life. Personally I feel it is extremely important to understand before I decide where to put my hard earned money.

13 Likes

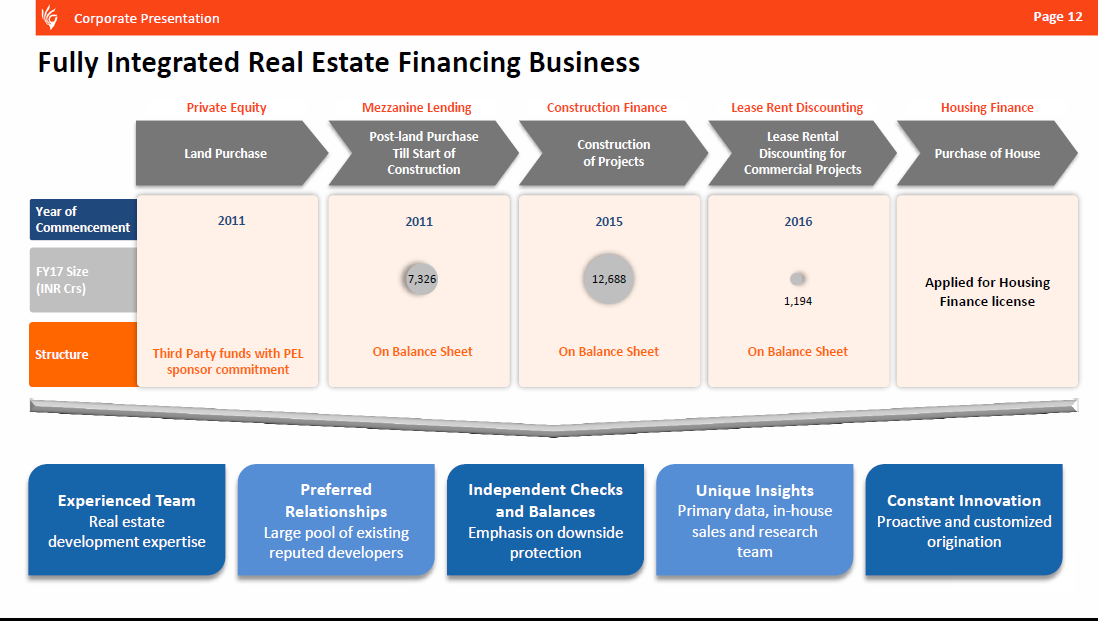

Recent investor presentation shows Piramal’s approach to real estate financing which is the growth engine of Piramal in last 3 years

Its quite interesting to read complete investor presentation.http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/26fbe02f-aecb-4ba6-a6fc-e462c83b7b5f.pdf

Piramal Finance invests Rs 565 cr in two auto component makers

The company has invested Rs 275 crore in RSB Group and Rs 290 crore in Indoshell Mould Ltd, Piramal Enterprises said in a statement.

1 Like

Thanks for sharing @noelsouza.

Would like to believe Piramal team would have seen Tony Seba’s energy and transportation disruption video (here). Curious - what would be the thought process behind investing in gasoline auto component space? How safe/risky it is to ignore obsolescence risk in investing decision? Time will tell.

On similar lines, had Piramal team not invested in Vodafone fearing Jio disruption risk, then would have missed the decent returns from this investment.

Disc: Invested

1 Like

Sometime being too optimistic on any company, creates bias and we believe anything company is doing is an excellent, however when tide turn away it is difficult to digest.

7 Likes

This is not an investment. Its a structured loan given to the company which will be paid back upon maturity.

4 Likes

Latest Piramal group investme in luxury real estate developers but not in affordable housing. Bangalore having so much unsold luxury real estate and developers are struggling for finance as banks are not willing to land money. However, Piramal group investing huge money.

Embassy Group has about Rs5,500-6,000 crore of debt. It has been active in adding new projects and buying land or entering joint venture

1 Like

“QIP is a capital-raising tool through which listed companies can sell equity shares, fully and partly convertible debentures, or any securities other than warrants that are convertible into stocks, to a qualified institutional buyer.”

If my interpretation is correct - above is signalling equity dilution. Please correct me if I am understanding it incorrectly.

Yes, it is equity dilution. But it is important to note what response QIP generates. QIP provides opportunity for qualified institutional buyers to buy large chunk of stock which is not possible otherwise. Hence large over subscription to QIP means institutional investors are finding this price attractive.

Historically stock price of a company moves up after having successful QIP. So by equity dilution, EPS comes down , depending on dilution % but market re-rates (PE) the stock at the same time.

Coming out with QIP shows confidence form company management about company growth. So if QIP gets massive oversubscription, it is great news for minority shareholders. I guess that may the reason why Piramal was up 5% on Friday.

Discl - invested for last 2+ years and continues to add more

5 Likes

Piramal Finance lent Rs425 crore to Noida-based Prateek Group to repay existing loans to Xander Finance Pvt. Ltd and a couple of banks and complete construction of its township project near Ghaziabad

Piramal Finance Ltd, a subsidiary of Piramal Enterprises Ltd, has lent Rs325 crore to Noida-based realty firm Mahagun Group to refinance existing debt and as construction finance

Recently, huge money invested as construction finance to distressed developers to pay the existing debt and to complete projects by Piramal especially in the area which having highest unsold inventories (Noida, Bangalore) in luxury housing segment. Kindly help me to understand following my doubts -

(1) Construction finance - large amount loan to single distressed developers to refinance debt

This is good to show fastest loan growth but have highest risk compare to small ticket housing finance.

(2) QIP (diluting equity) and investing in high risk area (large ticket construction finance)

Are above points to be taken seriously or we have to keep eye closed and just believing Piramal group’s past record of return.

Disc- invested but looking to liquidate

Sideline - View of Kenneth Andrade, Founder & CIO, Old Bridge Capital Management On NBFC

http://economictimes.indiatimes.com/markets/expert-view/there-is-opportunity-in-smaller-it-and-select-pharma-stocks-kenneth-andrade/articleshow/59048657.cms

1 Like

Look at things this way. A builder today is getting his debt refinanced over and over again just to buy time because the loan includes a moratorium period. Today if Piramal has given a loan then tomorrow Xander,edelweiss, india info line, Indostar etc will come and take out Piramal. In this period of time Piramal has earned upfront fees and interest at 14-14.5% which gives them an IRR of close to 18-19%. There are very few business which can absorb and redeploy capital in such huge quantum. Piramal per se will reduce wholesale lending risk to a great extent as soon as the HF license comes in July. They are looking to disburse around 4-5000 crores in retail in this FY. It should be viewed as a financial services company with pharma and data analytics as a kicker

1 Like

Interest rates at which piramal enterprises is lending is usually much higher. For instance, piramal lended a sum to panyam cements and to ncl industries at 18-24% interest pa. These cement companies are pretty risky bets. So interest rate goes up with the risk involved.

But as per the news…Builder took finance to reduce cost of debt. If Piramal charge higher interest then how can it reduce finance cost? No where disclosure about rate of interest by Piramal

Market will see negative if such thing done by DHFL or even by Banks then why we are so optimistic about Piramal or we are positive biased till we see higher NPA

E.g Embassy having 6000 cr debt and no predictable cash flow and correction in luxury property market due to RERA, etc. Is Risk b/s Reward favourable??

2 Likes

So Piramal will lend to A+/A grade developers like Embassy, Lodha around 12% and B+/B around 13.25%. Piramal monitors cash cover and not asset cover like PSU or some pvt banks. Cash cover is linked to sales velocity of the project and also other group projects. They would make sure that this cash cover or Sales doesnt fall below a threshold so as to service the debt. In their term sheet there is a clause that gives the lender the power to sell apartments in the project at market or below market rates if their monitoring process throws up a red flag. Moreover in construction finance the entire sanctioned amount is not disbursed in one go it is linked to various stages of construction.Due to the NPA situation at PSU banks and risk averseness of pvt players (as they dont understand RE) players like Piramal will not face high default cases as the builder knows he will not only lose his project but also no one will give him a loan again. In case of default also Piramal has a network of builders who they can sell the project to.

19 Likes

Excellent, Thanks. The distinction between asset cover and cash cover is the missing piece

I needed to substitute the “Trust in Piramal, they know what they are doing” with legit arithmetic.

It further clarifies my BINNY Ltd investment for me; a component of risk-mitigation for me is that it is funded by Piramal who will take over the project in case the execution risk comes true.

I am particularly impressed by the clause : [quote] In their term sheet there is a clause that gives the lender the power to sell apartments in the project at market or below market rates if their monitoring process throws up a red flag [/quote]

1 Like