Indri could be beneficiary of this initiative

1 Like

Good points.

I read the 2024 AR just now and found something puzzling.

Please could you also ask them about Rs. 39cr investment in Piccadily Hotels (promoter entity) at a price of 10,000 per share (100FV + 9900 premium) about 8 yrs ago. (Refer to AR2024- Unquoted Investment)

3 Likes

USL also ? I believe Godawan is from USL.

That could be a good promotion for Godawan. All indian single marts already been exported to these markets including Indri. Post operations start of Portavadie plant in UK, Indri will be locally produced. Anyone any idea when will this plant will start selling?

1 Like

No…Indri can not be produced in Scotland.

By definition, a single malt can only be produced in a single distillery…

But the Scotish distillery will be used to sell locally in UK n to sell in India as Scotch single malt/ blended whiskies with different brand names.

2 Likes

Indri is also being sold through Amazon UK along with other channels.

3 Likes

This isn’t conclusive at all. All the shares could have been issued at 10k / piece

No sir - premium is part of equity & not reserves and surplus. Your paid up equity capital as reported to MCA includes face value + share premium

In a way it is good if the co is holding these non-core assets that have monetizable value in future. Especially because these are legacy and its not that Piccadilly is investing additional sums in it in the last 4-5 years.

So focus of present management is clear.

4 Likes

The assumption of Rs 6000 Cr + valuation for Piccadily Hotels is based on a wrong calculation.

Just to clarify the arithmetic. If a private company has issued a total of 62,600 equity shares issued at Rs 100 face value + premium of Rs 9900 i.e. Rs 10,000 per share then the “valuation” of the company is 62,600 x 10,000 = Rs 626,000,000 i.e. Rs 62.60 cr. Hope this helps.

2 Likes

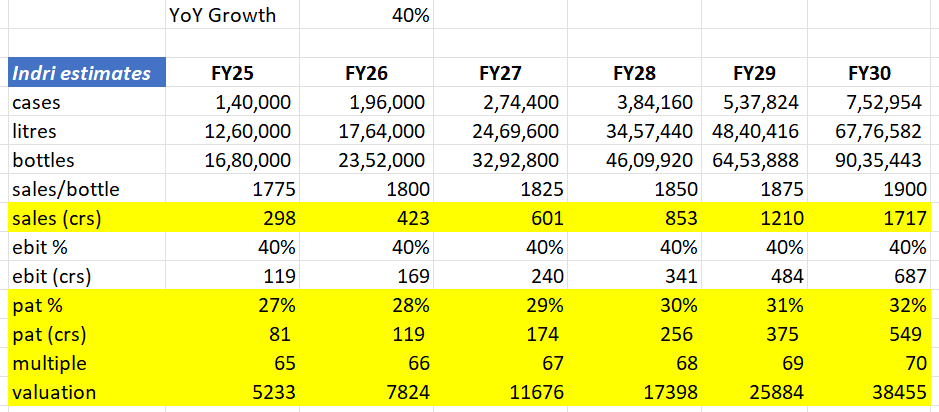

Tried doing some math for Indri… I feel my FY26 numbers are very conservative. In likelihood (if overall consumer sentiment picks up), FY26 numbers for Indri can be around 220k.

What’s interesting is valuation of Indri alone is going to exceed current mcap in 1 year

2 Likes

What supports your assumption of taking 27% as net profit margin for Indri?

27% PAT margin translates to 36% PBT margin assuming a 25% effective tax rate

Q4FY24 which had higher proportion of Indri sales in the overall distillery segment had a 31% EBIT margin. Even if you allocate all of interest & other cost to distillery segment, the PBT % would have come up as 29% for the distillery segment.

Now this 29% is composed of low margin country liquor and ethanol sales and high-margin Indri sales. It’s anyone’s guess as to what margin Indri would have given that country liquor would be mid-teens at best.

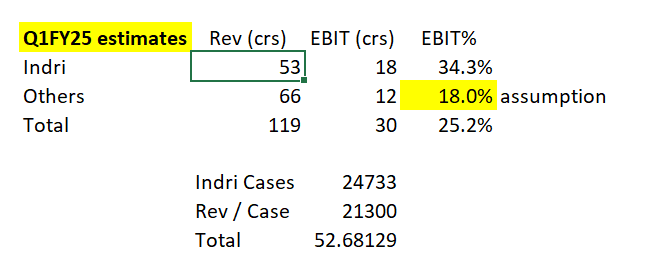

I tried to do the above math for Q1FY25 and here’s the estimate:-

Another way to look at this is 70%+ gross margins. Take another 25% for SG&A and all other kinds of opex. That gives you 45% EBITDA. Interest & Depreciation - take another 10% worst case. 35% PBT and you have 27% PAT after assuming 25% tax rate.

In my practical view though, gross margins would also inch up as special editions of Indri gain traction. They sell at nearly 2x price point, which means gross margins may be substantially higher for them.

7 Likes

Alchemy Capital Management Private Limited, which had consented to subscribe to up to 2,68,817 CCDs, has not been allotted any CCDs by the Company due to their PAN is reflecting equity trades, as per the queries raised by BSE.

Ms. Deepa Sondhi has declined the offer to subscribe to CCDs made by the Company. Therefore, the Company will not be allotting any CCDs to Ms. Deepa Sondhi."

This caught my attention. I wonder what the part about Alchemy Capital means. It’s not very clear.

1 Like

If my understanding is right, if you have prior holding, then preferential gets cancelled. Saying on the basis of experience (not sure if its across the board) of having participated in a preferential issue recently.

In any case, another fund of Alchemy has subscribed, so seems like a technical error rather than anything else

3 Likes

It is about the allotment for Rekha Jhunjunwala via Alchemy that company filed disclosure for.

The outlook just keeps getting better.

Indian whisky brand Indri makes retail debut in Tesco | The Grocer

(Tesco is the largest grocery retail chain in the UK)

10 Likes

Curious if export realisations in general in this space are higher? Indri is being retailed at GBP45 for 700ml bottles, which is far higher compared to Indian retail prices.

This is big deal to get to costco stores.

https://www.mensjournal.com/news/costco-2024-whiskey-advent-calendar

9 Likes

4 Likes