Very well said Hiteshji. It is always a great pleasure and learning experience to read your thoughts.

Also feels good seeing markets behaving rationally.

Very well said Hiteshji. It is always a great pleasure and learning experience to read your thoughts.

Also feels good seeing markets behaving rationally.

Apparently market is behaving irrationally, isn’t it?. Stock price is going up based on alone positive management commentary on future outlook. Once thing to remember is management is almost always most optimistic stakeholder in company. They are last to admit negative things about company/business.

We are in bull market and generally in bull market positive commentary is enough to shoot the prices of stock while negative news are conveniently gets ignored.

We should give it more time and assess once price gyration are stopped and news/data/outlook flow received in last 2-3 days is settled in price. May be there is low probability of permanent loss of capital but we may have to pay in terms of Opportunity cost

Disc: hold less than 1% of portfolio and may buy/sell anytime.

That would be true statement in general but I would call it more of a subjective discussion as it would differ case to case basis. As we know PI management have been pretty honest about company prospects in past you got to give it to them.

Disclosure: I have recently taken a position in PI Industries so my views may be biased.

Cartica is finally out. May be some MFs have bought the stake. How to get the data on buy side? Any guidance?

Remaining too much optimistic may not be good unless it is data based/actual performance.

Now crude oil is heading above $60, hence, all industries using petroleum/petrochemical as raw materials (Paints, Rubber, chemicals, agro chemicals, etc) find difficult time to maintain EBITA and in next qtr bottom line get affected as they can not pass this cost to customers easily due to competition and poor demand!

Agreed. I didn’t mean to discredit data based validation, that is something one must not ignore.

Can the global consolidation among agrochemicals companies put pressure on PI industry margins(like what happened with us pharma, may not be exactly similiar situattion). With consolidation these companies should be able to maintain their inventory better,limiting offtake from PI industry.

Recent price Action in PI taking it to all time high.

Does any one know any specific reason or news in offing.

They recently did many Investors meet. Any strong hands buying it.

Disc:Invested

News normally follow price action ![]()

In any case, I feel temporary halt in growth provided excellent opportunity to a serious investor to add PI at good valuations below 800…multiple triggers seem to be inplace in last quarter of this fiscal in the form of back-ended delivery schedules in csm, reasonable growth in agri input segment in Rabi season, likely acquisition announcement, likely good guidance for next fiscal on back of low base of current FY18, more strategic tie ups announcement, etc.

Rgds.

Discl.- Invested

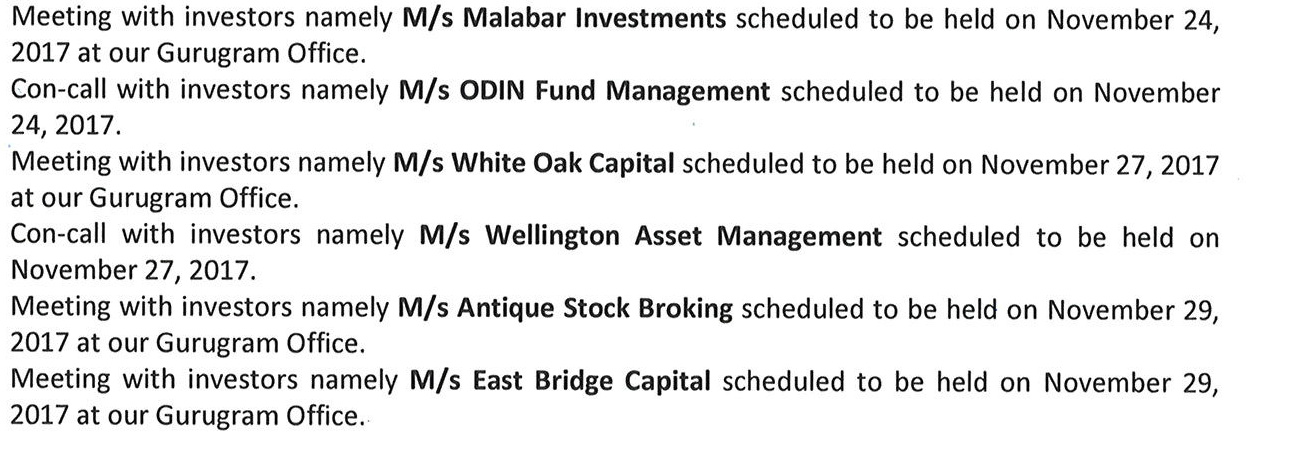

This seems to be unusual to a management devoting considerable time to hold a slew of investor meetings (close to 10 meetings now from past few weeks). could not think of a good reason why this will remove the doubt of management trying to showcase to fund houses/investors which generally is not a good sign nor a good use of time. any thoughts ?

Disc: Invested

Such slew of meetings are normally a precursor to equity fund raising. Also a proactive management has to remain prepared everytime to grab the opportunity when it throws up. In addition, it’s not necessary that in every meeting senior executive management will represent the company, such companies have a team dedicated for these.

Rgds.

Discl. - invested

Then they may be heading for possible equity dilution or offloading promoter holdings (currently at 51.55%) for fresh capital. So, the current valuations may be giving a better leverage on this front than debt instruments.

Pi Industries has been trading in a narrow range 920 to 1000 in last few weeks. Expecting a fresh breakout soon, especially before the Budget 2018. A budget with focus on Agricultural sector should benefit PI Industries.

If market continues to do well, i am expecting a 10 to 15 % upside.

Disc : Not invested, but planning to invest.

PI Industries Q3 results out

Results are out , I think results are ok it clearly shows stress on domestic agriculture but company managed 3 %,but on exports it was 14%growth , request all seniors to decipher the numbers more in detail

Would anyone could attend conference call give a summary of it and your take on the results?

Some points discussed in Q3FY18 conf call:

General

Raw material supply issues:

Generally PI sources around 30-35% raw material from china. Now in last 6-9 months PI has reduced this to less than 20%.In next 6-9 months, dependence on china will go down further mitigating this risk

The whole chemical industry is establishing alternate sources for basic raw materials.

This price increase caused domestic margins to go down. CSM margins could be maintained.

The value chain is as follows

starting materials-> intermedites -> AI (like APIs in pharma)

PI is predominantly into AI (active ingredient) where there is higher valued add. AI goes into formulations.

PI has started derisking by backward integration into intermediates in some of the molecules.

Also, PI is developing alternate sources with other suppliers in India for supplying intermediates. PI guarantees off take from these suppliers for next 1-3 years.

Last year PI did backward integration of two products. This helped PI get into newer products.

If backward integration gives PI financial/strategic advantage then PI will go for it, otherwise it will look for indian companies to supply them.

In general with these issues in china, huge opportunity for indian chemical companies will open up.

Some of the reactor companies, plant equipment companies are expanding/dong well.

Getting into pharma:

Seeing the current turmoil in pharma industries, change in valuations, going bit slow into getting into pharma.

Interesting opportunities in agrochem has opened up and hence gone slow in pharma.

Capex: FY18 - 175cr capex (spent around 100cr), FY19 around similar number.

Domestic:

CSM

Overall: difficult to achieve 10% growth given guidance for fy18, exports business in hand for 10% growth.

firm order is there for 25-30% growth in q4 in exports, but some spillage may happen to q1.

FY19 can be better than year than FY18

Fy18 - 22% tax rate, FY19 - similar range.

@ananth

Exhaustive summary, thanks.

Would like to reproduce here Bharat Shah’s queries (from ASK Investment) @47 mins in the call. Always a privilege and pleasure to hear Bharatbhai (he has asked similar queries in PI previous conf calls too).

Note: Can find his interviews and articles here.

Bharat Shah (ASK): Mr. Sarna, Hi. You mentioned that for the current year you hope to have a single digit growth. But for the nine months our top-line is about kind of flat, little about a percent down compared to the last year. So therefore the equation is, if we have to do - let’s say 5% type of growth for the year in entirety, then our domestic and international business CSM would have to grow about 20 to 25% in the fourth quarter. Is that what you think you are implying?

Rajnish Sarna (PI): Yes, good afternoon Bharatbhai. So as I said, the plan is there. The orders are there for even achieving whatever 25%-30% kind of growth. And we are expecting to do well in the fourth quarter. Now whether it will become 5%, 7% or 4% is something will depend on deliveries and other critical aspects. But what I can tell you is that - yes, the business is there. And if it will not happen 7%, 5%… it will… couple of percent it may spill over to the next quarter. But business will happen.

Bharat Shah (ASK): Okay. And secondly range have been little weak not just in the farms, I think the numbers have also - we have been deprived for a while. So can we assume 18-19 finally will reflect the normal year that we associate with PI in terms of the growth as well as the profitability?

Rajnish Sarna (PI): Yes, we do hope so.

Bharat Shah (ASK): So drop/drought should end now? Hopefully.

(gentle laugh in background from PI team)

Rajnish Sarna (PI): Bharatbhai… Ek marathon race hai… Woh bich me kabhi kabhi pani peene ke liye rukta hai dhaavak (racer)… Phir bhagne lagta hai…

Bharat Shah: Theek hai, sir. Bas to utna… Pani pine ke liye hi ruke hue hai na? (with smile)

(respectful laugh in background from PI team)

Rajnish Sarna (PI): Absolutely.

(with required seriousness)

Bharat Shah (ASK): Okay sir. Thank you.

For quick reference

PI industries was the second highest recruiter by hiring 5 students.