Surprisingly , Sanjeev Bharat is not signing the update letters and other disclosure documents submitted to exchanges after the buyback was withdrawn. I see company Secretary or Balram Garg is signing these documents which was not the case before that 25 May typo error episode. Also he has stopped replying my emails, and asking to contact investors email contact…

1 Like

*Bhatia… should be read

Finally some good news on the debt front. Well, it is mixed but I would like to see the glass 90% full than 10% empty. Please check details here: Ind-Ra is no longer required to maintain the rating, as there is no debt outstanding.

This is talking about their Commercial papers (3-6 month debt) of 200 Crores. If we see the earlier ratings then we understand that the initial plan was to raise 500Cr but then it was curtailed to 200Cr and now that too is paid back.

The negative part is that the rating was downgraded before withdrawal. The reason for Rating Watch Negative status which converted itself in to the downgrade was related to share price erosion in the month of April and hence possible loss of liquidity. Well, those concerns remain but with no debt outstanding status there should not be any problem to raise working capital requirements. As @LTInvestor has earlier pointed out there are no pledged shares either. Overall it seems all other sins apart the PCJ management is at least true in their intent to reduce debt. I would take it as a big relief/ plus. regards,

4 Likes

Yes- this is good news. PCJ has filed an added clarification on this rating withdrawal to exchanges where they have highlighted (in bold) about he debt reduction part as @neopandit mentioned. This time the CFO Sanjeeev Bhatia has signed the release so @ranviraaj this should also be construed as good news. https://www.bseindia.com/corporates/anndet_new.aspx?newsid=7eb86a4c-b792-4f24-b426-26190314eeb3

All things said and done nothing real has so far come against PCJ.

3 Likes

They paid this on 27 April 2018 , so I think this is already priced in and the debt which company has mentioned in the presentation is excluding of this commercial paper debts. Please correct me if my understanding is wrong.

No, all numbers on the presentation were as of march 31st. Last year out of 650 odd ST debt 192 was the CP drawn. I assume this year the entire amount was drawn. Total ST debt is 1000 odd crores.

I would not look at todays price movement. Expiry day. Interestingly 100CE for todays expiry is still adding open interest. Someone actually buying it!

3 Likes

Thanks @LTInvestor for the details. However, I was not able to link it to the table posted along with. (1) I guess last year is year ended in Mar 17 and 650 odd is 634Cr of ST liability. Am I right in those assumptions? Also, (2) I could not understand the 192Cr of CP out of 650 that you have mentioned. Other current liabilities are 228Cr and lastly, (3) you have mentioned “I assume this year the entire amount was drawn” meaning which amount? The 200Cr CP that IND-Ra was rating? And is your assumption based on the other current liabilities remaining in the same ball park?

Actually, I am hoping to learn the basics of fin statement analysis through this forum with a hands on approach. So, I want to confirm that my understanding is correct as well as to get my doubts cleared before I lose my way  I also like companies like PCJ with simple biz model/ fin statements as a case study. Thanks for your time and patience. regards,

I also like companies like PCJ with simple biz model/ fin statements as a case study. Thanks for your time and patience. regards,

It take ages to prove someone guilty and more so to prove financial/accounting gimmicks.

By the time the retail investor knows it, damage is done, here it already happened the price drop is real I think around 90%, as retail investors don’t have the patience/financial power.

The price chart is real-no business loses around 90% value in 6 months. I think just see the chart and it says in the last 6 months - get out of it - as simple as that.

PS:Nothing against PCJ, only part of my learning, so that I will avoid land mines in the journey to financial freedom.

3 Likes

Yes, I did not have the exact number. ST borrowings of 634 crores out of which CP was 192cr. So this year I assumed that they drew the entire 200Cr on the paper which was repaid in April. Yes Ind-Ra was rating those paper. 200 will be part of the 1000 St borrowings o/s.

Not sure about other current liabilities. Those must be payables to customer or government authorities. Else it will be shown under trade payables.

1 Like

You are right…retail would be the last to know. Let me lay down my thought process… I guess there are two ways one could approach this:

- Fraud-> leading to collapse in stock price

- Collapse in stock price -> and hence the post-facto deduction that all along fraud was being perpetuated

If you look at category 1, Vakrangee, Kwality, Manpasand could perhaps if I speculate can fit in there. Auditors resigned, treasury policy changes, promoter pledges etc and hence the collapse in the price.

PCJ to my mind till now (i.e. as of writing this) based on the available data and information is still not in category 1. Whatever we have seen so far- gifting of shares, Vakrangee buying, withdrawal of buyback due to the alleged NOC not being given by the Bank etc- I am not sure if they are straight examples of fraud. For all of these there could be alternate narratives. There are lot of allegations- Balram Garg arrested by CBI, they are linked to Nirav, money laundering what not- but I guess these are all still allegations. These are not supported by facts- at least not in the public domain. You can blame these guys for professional inaptitude; excess greed; trying to play around with rules etc but I am not sure if there is a fraud per se like say Satyam. They published audited numbers on May 25th and I reckon the auditor would (and should) have been doubly careful with all the other fiascos happening. Now I by no means know how the future unfolds but this is what I mean when I say “Nothing real has come far”.

2 Likes

Agree with you. However, one thing is not clear to me since I joined PCJ shareholders - in mid June 2018. Why everyone treats “Vakrangee buying PCJ shares” as fraud? Not even remotely trying to defend PCJ management here but what can a management do if someone buys the shares. The gifted shares were about 2.6% and Vakrangee stake is 0.5% so those two also do not match. For quite some time, I thought may be the gifted shares landed up with Vakrangee etc. because I did not know when and how many shares were gifted. That became clear only when I saw the postal ballot notice. But the quantities do not match. So, can someone please tell me why Vakrangee buying shares of PCJ is treated as a fraud. Thanks, regards

It’s being suspected that jewellery companies earned money in old currency and ND then got it accomodated through various channels I like

vakrangee .I m not claiming that PC did but so many companies did similar to things, why else vakrangee would invest in pcj.

PC Jeweller is a classic case of lot of mixed events, no doubt that it’s products are appericiated by customers, 2nd across India by sales, good brand build up, 20% growth converting on showrooms to franchise model which will increase the margin good market share of 20%, promotor are old Delhi Jeweller knows in-depth of business. PC Jeweller Rose from 270 levels in March 17 to 630 levels in Jan 18 than 85 to current rate. Rise from 260 to 630 was due to pump & dump strategy of Motilal oswal which they have followed in several stocks, MOSL dumped stock at higher levels, fidality had obligation to dump stock due to fund based decisions. Reasons for fall

- PCJ involved in fraud LOU/LOI

- Tieup with vakrangee for money laundering

- Name associated with Vakarangee

- Promotor arrested by CBI

- Gifted shares to own daughter

- Proposed buyback & called off

7 management is chor, not ethical

I see this as a classic case of fear & greed syndrome as nothing has been proven till date for any scam. Funding was also done in June 17 why so harsh reaction now. Buyback was a foolish idea for small traders only, I am happy it had been called off for any legtimate or non reason. So all in all it’s a 20 % growth company with PE of 5 Sales to Market cap 2, 2nd largest jewellery chain, manageble debts, paid off debts good auditors. It’s trading at 80% discount to intrinsic valuation. What else u will buy?

3 Likes

In your claim, most of the points are may be valid (like the money laundering during DeMo), but nothing proven yet. But the following are just rumors, not even allegation:

- PCJ took LoU (they never took LoC/LoU)

- Promoter arrested by CBI - on that very same day he appeared on media and given interview, gout away within 10-15 mins of promoter arrest?

1 Like

Thanks Atul. Actually your reply prompted me to check more about Vakrangee. I had read it to be a software company. Now I understand it provides lot of IT enabled services to grass roots. Still they can not explain vast amount of cash in old currency.

This is the worst thing I experience with PCJ - We keep losing time on a never ending chase that has no answers. May be we are trying to find rational in actions that are reactions to things we will never know. Right? This it self is a good reason (for me) to book loss in INR, close the topic and save time. There is absolutely no learning here (the financial statements are good) besides avoid inexplicable stocks in the first place and dump as soon as possible without offering any benefit of doubt to anyone at any point of time. Price is supreme. Thanks, regards,

1 Like

Panditji, untill you see things, don’t take decisions in stock market, most of time panic is created to snatch good stocks by spreading rumors, I am not saying PCJ is a good stock. However I decide good and bad stock based on valuations and future cash flows. Current rates Titan is a good company but bad stock and PCJ is bad company and good stock. It will take 1 year for PCJ from turning to good company however at that moment your buying capacities will be limited. Whatever wealth I have created in stock market is with companies which market don’t like & started liking later. All investment which market liked & I bought are suffering. Choice is your. Your need to convince yourself nobody else. Promotor lost 11000 cr in this debacle and he has single investment.

But you are saying so!

Value is subjective. It is your opinion that differs from the market, and that is perfectly fine, otherwise there will be no market.

Same goes for me. I started by buying metal stocks in 2015. But it is not the only strategy to make money; it certainly was the most vexing one. Take PCJ as example, every day you wonder whether the company is fraud, while the “blessed” companies keep making fresh highs.

1 Like

I have Ambuja Cements, IDFCBank, Reliance Capital, and Reliance (since the time no one liked it). Before that I averaged up in Cairn and was rolling over one lot of Crude for couple of years. Currently I am holding Silver contract and planning to roll it over. So, your point on taking contrarian bets is well taken on board.

But PCJ is not a contrarian bet at this point of time because there is no visible challenge to the business and the stock price is literally decimated. This basically means I do not have all the inputs. And there seems to be nothing publicly available that I am missing. Besides more people like PCJ today than a quarter before. The number of shareholders has swelled ![]()

There is a lot of difference, First, Promoter knows the real situation and I do not. If I knew the real situation then I will have no problems - I will know exactly where the biz, stock, and promoters are heading (London, Antigua, Delhi). Secondly, my primary worry is not about my losses in INR. I am worried about my loss of time, loss of attention to other scrips in the portfolio and whatever happens in their environment, and my possible loss of new opportunities. I can not bother myself and neither I am required to be bothered about what is a loss to any other investor in PCJ including promoters. Promoters on the other hand are obliged to care about minority share holders and be transparent in their dealings which they are not, Third, there is no proof that promoters lost a single rupee. You may be stunned by the spectacular notional loss but we do not know what was their position in the derivatives market. This is same as saying RJ loses crores of INR in Lupin and quarter after quarter he adds Lacs of shares in his Lupin holding. And Finally promoters can buy at least 15% stock from the same amount for which they sold, sorry gifted, their 2.6% taking their stake from 60% before gift to 72% now. And that is without running any conspiracy theories about derivatives trades and running/ helping bear cartels which can be and most probably are true.

So, I am not at all impressed by the notional loss of 11000 Crores to promoters as some sort of psychological compensation for loss of my time. Regards,

5 Likes

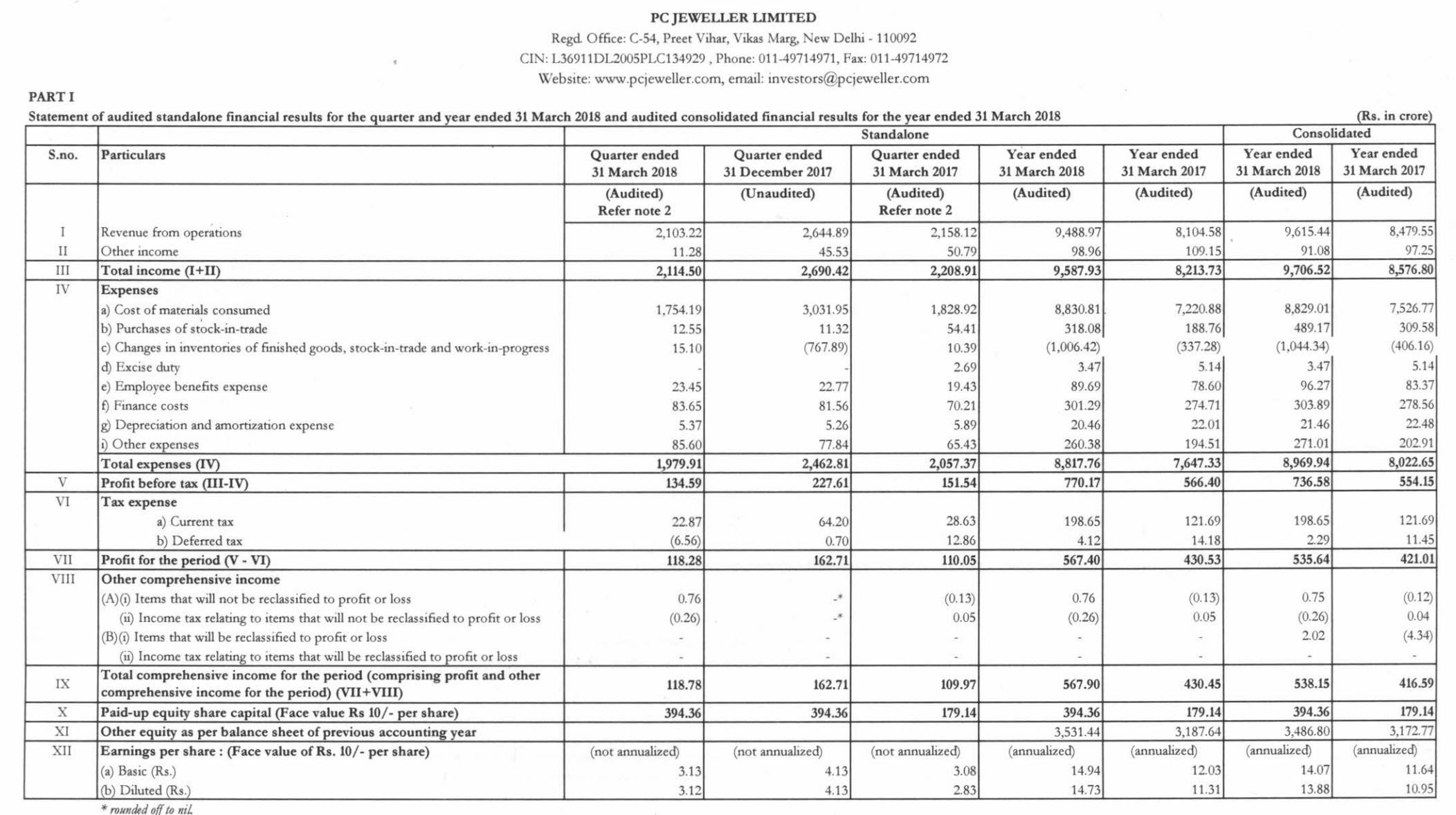

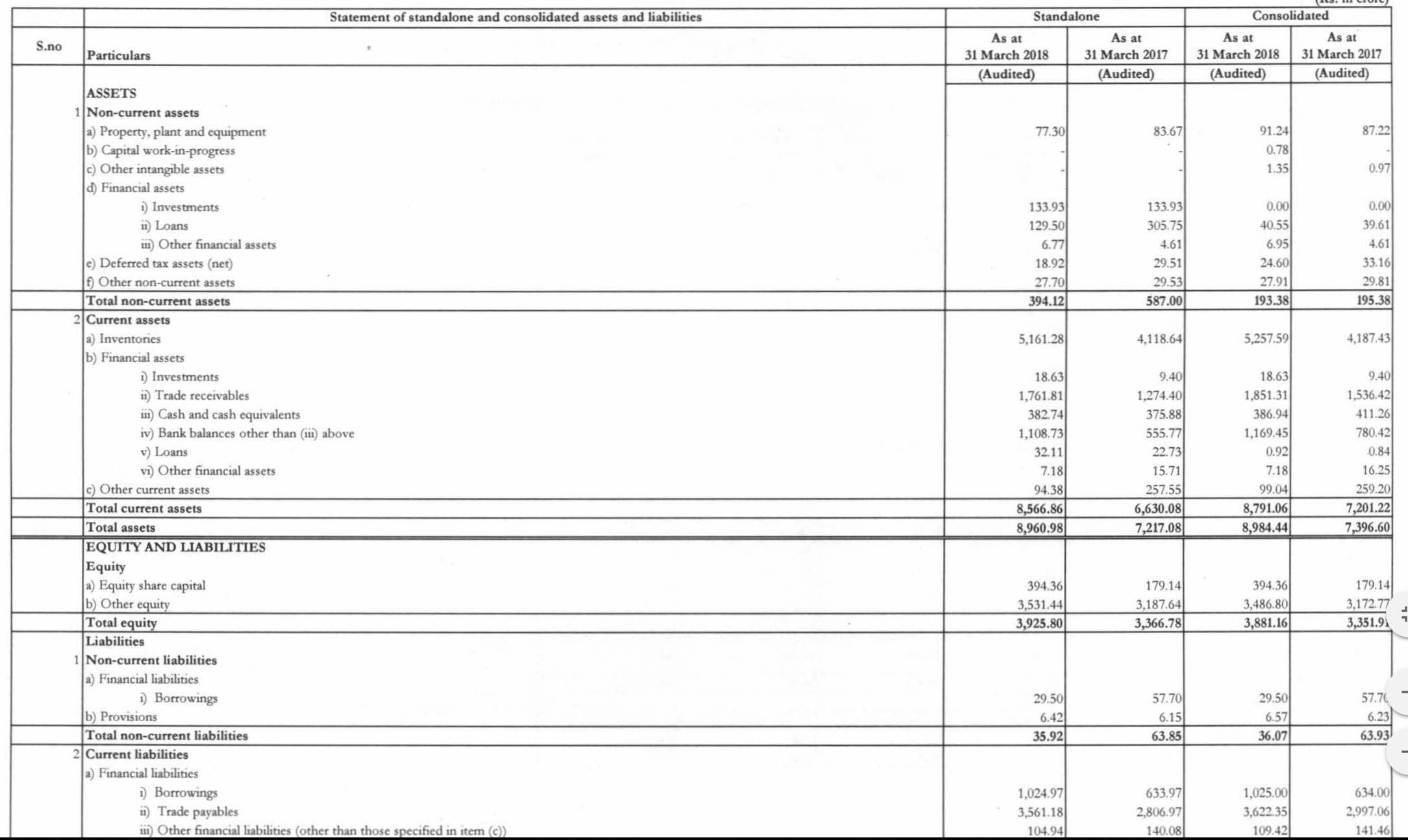

One basic question: As on March 31, 2018, the trade receivables are huge (Rs 1851 Crore, nearly 20% of the revenues), while the trade payables (Rs 3622 Crore) have gone up as well. Looking at the earlier balance sheets (FY16-17 and FY 15-16), the numbers have increased at a huge pace. The main reason for the company’s claim of Rs 1400 Crore cash (in current assets) is the increase in trade payables.

My question is, why are the receivables so high in this particular jewellery company? If the demand is there, nobody would like to sell jewellery on credit right? In comparison, Titan and Thangamayil have minuscule receivables compared to their total sales.

Attaching the balance sheet and PnL for reference:

Cash receivable are from export business as claimed by Company, currently 1274 cr. Trade paybles are gold lease which is close to 3000 cr, inventory is 4100 cr. 425 cr receivable recognized in April 18.