If u see none of their stores are in Mumbai. This what makes me doubt on them. Their one new store is in pune & other in Nagpur. But how come a Jewellery seller doesnt have any outlet in Mumbai or Navi mumbai might be scared of Titan.

@Pankaj181…Haha no hard feelings in the stock market. You marry a stock, you divorce your wife.

But to my defense, in case of Vakrangee, my feeling is that the cash flows are not real. Maybe real, but politician money moving in and out. In this case unless every second piece of jewellery sale was non-existent and every second store in non-existent, difficult to see how the cash flows are fake.

U may be right with ur views. But I am still not confident with PCJ mgmt . For me the biggest red flag was selling of shares by one of the promoter Krishna Devi that too 10lakhs just few days before the Gifting story started. It clearly means she knew something. And at present her holding is NIL.

Have you ever" heard of anyone saying shaadi may jwellery PCJ se liya hai"

I heard of PC Chandra jewellers but about PCJ i heard only in Forums or in media news.

As pointed out by @phreakv6, even i find sudden rise in CFO in 2017 just after demo intriguing. Working capital requirements suddenly turned around (became positive) completely…all receivables received all of a sudden! Cash rose from 300 cr → 1120cr.

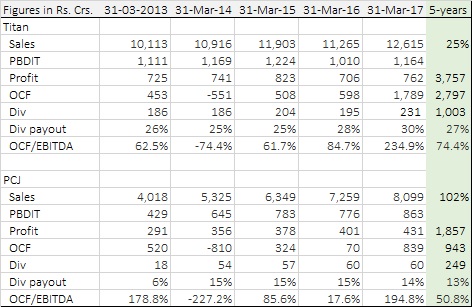

Reg financials, 10 yr cPAT (2500 cr) vs cCFO(640 cr). That too aided by demonetization (839 cr in FY17) a big red flag!

Another related point is it’s huge receivables, which they say is because of exports business. Why a B2C company got this kind of receivables? In comparison, Titan got not much receivables! Are the profits real? Why would a company, which claims there is such huge market domestically with superior B2C margins, even try going for exports with these kind of receivables?

My jeweler friends had intimated about wrong practices that were prevalent with this brand. They never spoke highly of the promoters or its products. Many of them have been dealing with PCJ from last many years.

Share gift to non promoter #Hindsight bias

When both scuttlebutt and financials puts question mark on corporate governance & mgmt, i tend to stay away from such companies. One must look beyond numbers. Scuttlebutt helped me stay away from many value traps such as Kwality, Vakrangee. One should always look for ‘quality of earnings’ rather than ‘mere earnings’. Promoters must be ethical, else would destroy shareholder wealth in long run.

To be sure, Titans CFO also went from 598cr to 1790cr from 2016 to 2017. So the jump in CFO in 2017 is not unique in PCJ. Surely you are not saying Titan also did some demon hera-pheri.

per March 2017 balance sheet, Cash and bank balance is Rs 1,191.68 cr. If half of that will be used for buyback of 10% shares(looks like stock price will stay in lower levels till then? it will be a confidence booster. But not sure about current cash position ?

Can you explain your observations a little more in layman’s manner for my understanding and the relationship between off and profit and your conclusion.it will help me to understand

This is completely disastrous. Can investors have to believe of PCJ’s management as they keep saying one thing that they don’t know why share price is decline so badly and they are keep giving this statement since vakrangee case. Now once PCJ will be ban from F&O then this share will start behaving like penny stock. Sometimes upper cirkit sometimes lower. Hard to reinstall trust of retail investors now. This type of fall causing great damage to company as well as investors pocket. SEBI have to take some stand in such cases. SEBI keeping mum that is also disgusting. No security of investors if such things keep happening with us.

@atul1082 What I was trying to do is to compare with best of class to see divergence because what is everyones mind is if the financials are real or fake. So,

The sales growth stands out. While Titan grew only by 25%, PCJ grew by 100% in a lacklustre environment. There could be false invoicing to launder money. Show cash sales but no real transfer of goods. So the gift was a payment to settle dues. But no real effect on the company. Company got cash and promoters settled with own money. Doubt this happened. No Indian promoter is this generous.

The OCF/Net income in simplest terms shows how much of profit is cash. If everything is in cash and just in time, then difference will be D&A + interest. Here PCJ numbers are lower, but they are expanding stores and sales. Assuming sales are not fake, they will need more inventory, give out more credit which will utilise working capital. If Titan grew by 100%, think their numbers will also come out similar. The stores can be fake but in Delhi they show stores at South Ex, Karol Bagh, Rajouri Garden. These are very upmarket locations.

Again the market knows something we don’t; maybe their international business in Dubai has LOU as per rumour.

So this is really at 36K feet level. My exposure is limited so for now this is good enough to take a small call. Please do self due-diligence before purchasing.

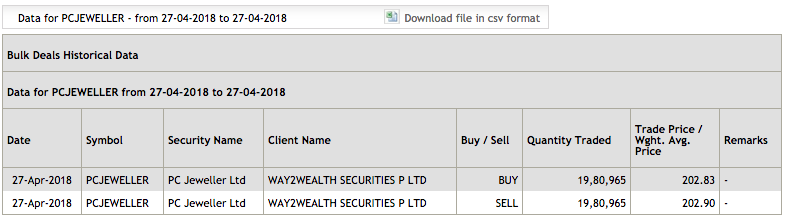

This YouTube Video gives and Idea what officially is being said about the promoter Stake being Gifted to some person in the Family. Very important to note that there are NO details provided on who received these shares.

The Video Link below has got some very interesting Insights on what could be taking place in this stock, IMHO Something very Fishy is going on here…

L.T Investors should stay away.

This also includes a short discussion with Balram garg towards the later part.