Any progress notes on this lately ? Thanks.

awaiting the AR. otherwise no information.

Huge delivery percentages since the last twenty days or so. Product is in superior demand, strong demand and results posted by Heat Exchanger manufactures (Anup Engg, GMM Pfaudler’s Engineering Division), and other private players.

Being certified by the top authorities in the US, and India; coupled with a strong export franchise, it seems Patel’s Airtemp could possibly deliver great results.

The entire heavy engineering sector is seeing a traction, this should surely benefit such a profitable company!

3 Likes

Since the industry and production boom is coming, I think it is a huge opportunity for this company…

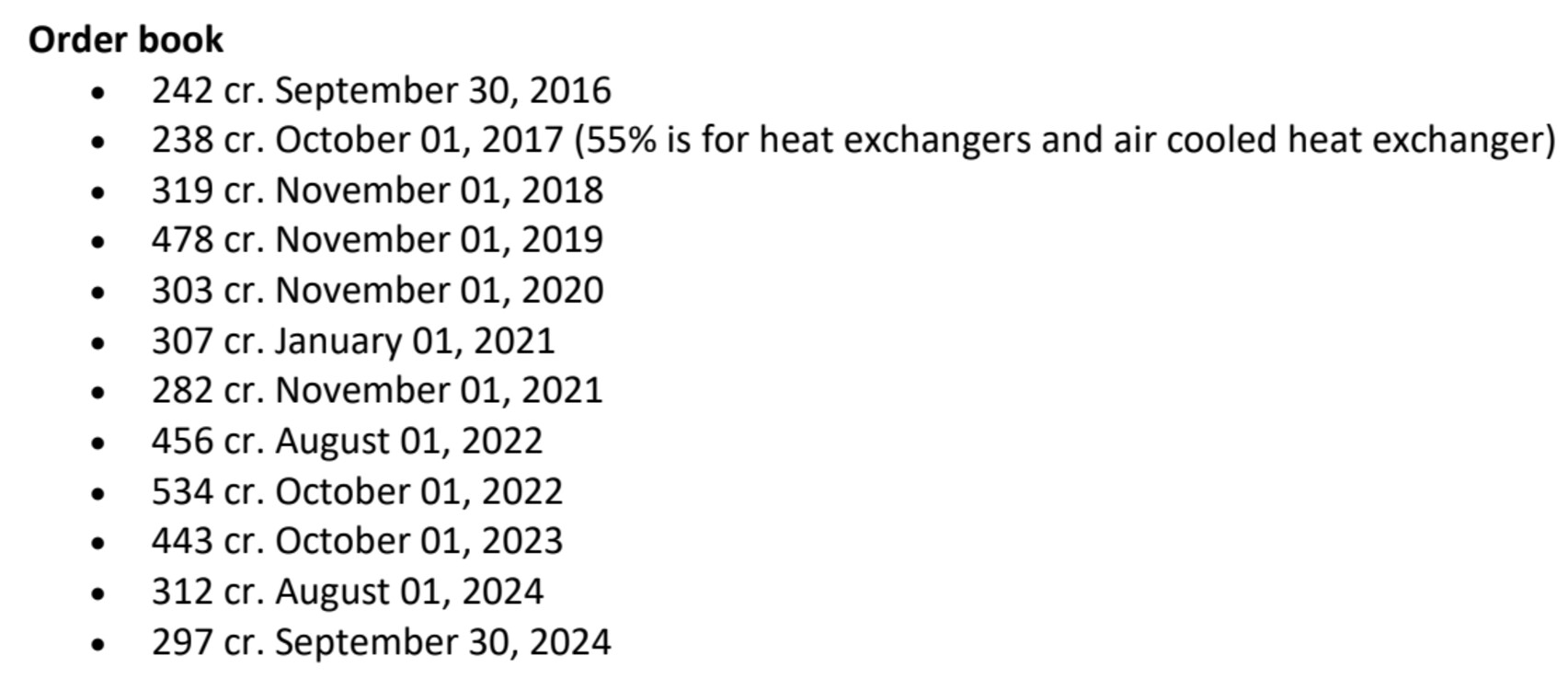

The Company has continued in receiving enquiries from

current and new clients from Domestic and Export market. It’s

my pleasure to inform you that as on 1 August, 2022, the

company is having confirmed orders of about ` 456 Crores

which gives opportunity to achieve growth in terms of

revenue and become market leaders.

Annual report 2021-22

3 Likes

Promoters buy about 10% stake at 232 is a very positive signal. The price was about 200 in August 2022. i think the company is going to see huge increase in orders - from domestic and exports. with many companies diverted to India (from china) it is going to big boost for the company.

3 Likes

Where is this information available that promoters bought 10% stake at 232? I can see that the shareholding has rather gone down by 6% because Rashmika Patel has been classified as a non promoter now. As for promoter buying from open markets, I can see couple of trades in Aug 2022 but it is just around 0.5%. It is indeed a big positive if what you are saying is correct.

Seems like they have taken up the Stake increase through preferential allotment @mkt price… equity capital increased from 5.0 to 5.47… additionally veru helathy order book… same segment peer Anup Engineering is doing good… over all good. but

seems like the have a court case file by someone… I could not understand what is interlocutry case ?

promoters bought at mkt price of 232 was very positive. As it is a small cap, price is volatile but over long term it is multibagger. Demand for air cooled technology is large - they just have to execute… they have decades of experience…

1 Like

Have been following the company. Sales have stagnated - order book in at 450crs in low for such kind of companies - where delivery takes a long time. Recently they wound up the US subsidiary - not sure if they were not able to get orders or they will supply directly from India.

It seems like a wait and watch as company doesnt have share any info thorugh investor presentation / investor concall. I would wait for numbers before investing.

Disclosure - have sold my holding.

Hi,

With passing away of founder, the company will take sometime to gain back the momentum. But in general, the things are well on track and hopefully the next generation Mr. Sanjiv Patel will accelerate the company going forward. I believe the winding of US subsidiary is a good decision as no business advantage was there because of the office and they are able to manage things from India. Company is very conservative but lets see with new person in charge how things go.

Disclosure - Invested and adding few.

1 Like

it appears that the next line had already taken charge so passing away should not affect things. but concerns over growth remains - especially when the PE is very high at close to 20.

Hi,

I have attended few AGMs and also went to visit the factory when they conducted the shareholder tour. During such conversations and also from the presence I found out that founder was involved in all day to day execution and meetings and also vendors were very much used to his style of work and communication. Mr. Sanjiv Patel was mostly spending time in US and now he would be taking care of all, so I believe it will take some time. High PE is related to also sector being in investors focus if you look at other such companies like Loyal Equipments, Mazda, Anup Engineering ofcourse they all have good profit margin which Patel Airtemp is lagging but if that is controlled the overall outlook is good. I sense that they would now focus more on profitability and not order book…Lets see.

2 Likes

While prospects for these companies are good. valuation is very high. even 1 quarter of underperformance can get the stock prices down.

1 Like

True, but looking them on a quarterly basis is something I wouldn’t do as their execution to delivery depends on the current order cycle which largely varies. Looking them on a 6 monthly to yearly basis is good to know the real picture.

3 Likes

Mar 24 results are out, company posted revenue of 370 Cr in comparison to 280 cr , also profit has been increased to approx. 15 cr. Company seems to be getting benefit of the new infrastructure whereby they have started increasing the turnover with some cost benefits. Industry expectations are also high so if company executes well in coming 2-3 years it can reach a good scale as the scope of growth is quite high. Historic problems of low profit has to be seen…

1 Like

Hi @UrvilShah

Companies operating in the area seem to have 20% plus margin. Any idea why this company has relatively lower margin and also unable to increase revenue ?

Thanks

Hi @Amit_Paul ,

They are historically having high cost of Late Delivery Charges / Damages etc. and also due to space constraint they were outsourcing lot of jobs so they had relatively low margins. In the last AGM call they told to focus on controlling such charges so let’s wait for that…

On the revenue side they have been doing pretty good …FY 23 was 280Cr FY24 370Cr also the H1 revenue for the current FY has improved from 168Cr to 195Cr, so they might click 400Cr.

The company in general has some good products but they somehow are not able to reflect their brand value in profits, once it starts coming the company might be at a reasonably good level than present.

1 Like