I am from Pune and know PNG since my childhood. They are honest and ethical. They do good business in and around Pune but I am not sure if they will be able to replicate it outside Maharashtra. People visit PNG because they have been in the business for almost 200 years so PNG is a household name here. If you need Gold you go to PNG and that is a mantra here because they have been here for 2 centuries now. People don’t question this loyalty because that has been followed across generations. Same thing is unlikely to happen in other states. They will make some inroads in other states but I am confident, the brand loyalty wont be the same as you have in and around Pune.

9 Likes

Few days ago I sent the same email to them lets see whether they will clarify or not

I sent an email to them asking why they changed their plans to expand in UP and Bihar from earlier Peswa Route? sent multiple mails but haven’t received any response. If anyone here knows that will be really helpful.

1 Like

Today I had a cal with the PNG Finance team to respond my query in relation to drop in Gross Margin YOY in Q4

Two things came out

1 ) They had a inventory gain of around 15-20 cr last year and 40-50 cr of hedging cost in current quarter , If we normalise both Gross Margin has improved from 13 pc to 15 pc on a YOY level

2 ) We need to dig deep on hedging cost of 40-50 cr , Can anybody explain what can be this hedging cost , what are the drivers and how much of this is sustainable ; my understanding is that hedging cost should be around 3 pc p.a. of total inventory hedged . if their overall hedged inventory is appx 1000-1200 cr , quarterly hedging cost including interest on GML should not be more than 30-36 cr per annum and 8-10 cr per quarter , if this is true then their normalised PAT margin in Q4 should be around 5.5 pc which is way above the guidance they are giving , I don’t think they are too serious in their investor communication

3 Likes

Yes, Hedging cost for the quarter seems to be very high.

Atleast we can ask this in the next call if they can understand what are we asking

2 Likes

Could anybody figure out what would have led to sharp increase in hedging cost in last quarter ?

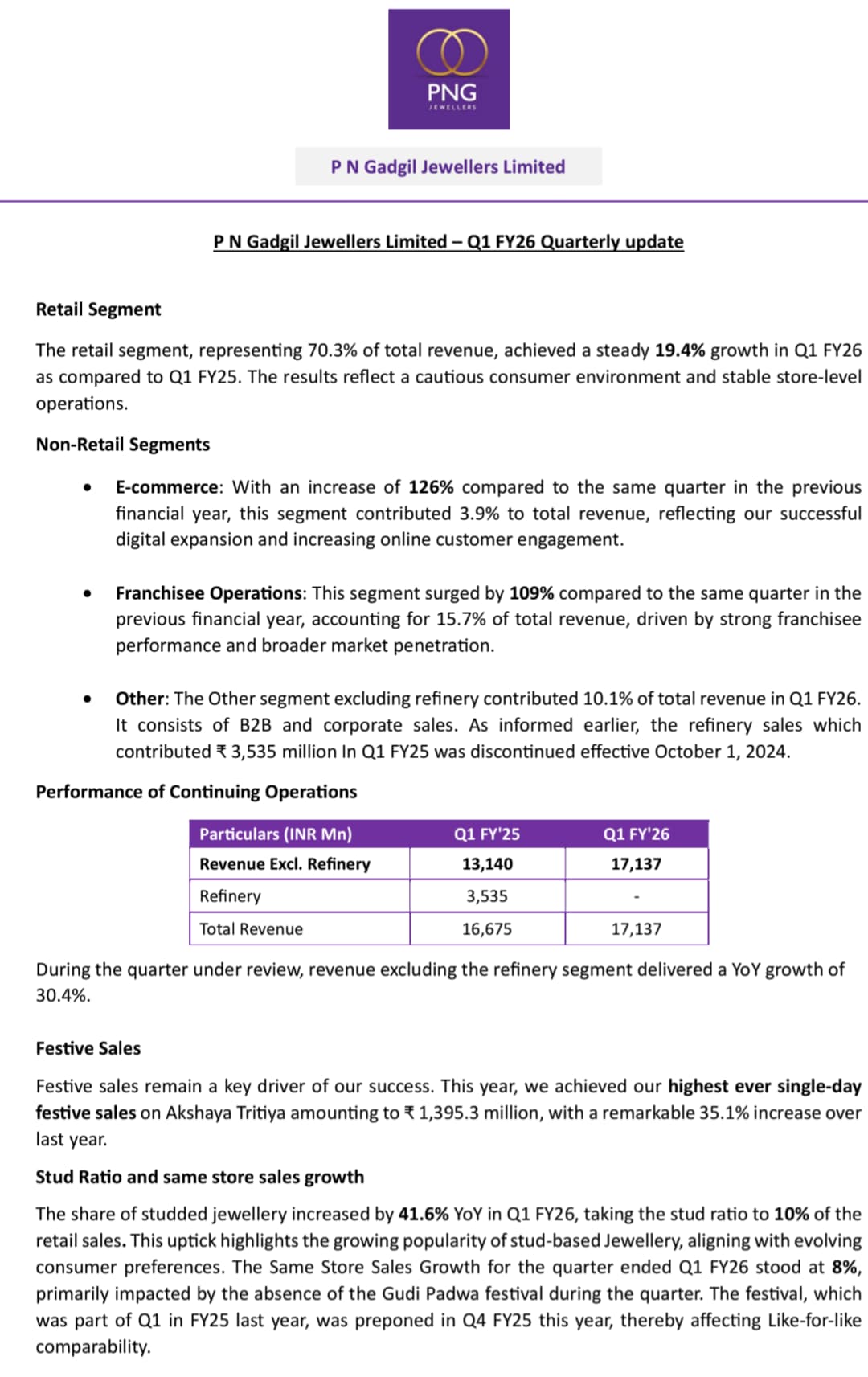

Q1FY26

- 30.4% revenue growth YoY excluding refinery revenue

- Stud ratio is at 10%

*SSSG- 8% - 7-9 stores in Q2 (20-25 in FY26)

2 Likes

PN Gadgil Jewellers ltd -

Company retails Jewellery through a network of 53 stores ( 41 owned and 12 franchisee stores ) across 27 cities in Maharashtra and Goa. They were able to sell 8.6 tons of Gold and 25.2 tons of Silver in FY 25. They r the second largest Jewellery brand in Maharashtra ( after Tanishq ). Maharashtra accounts for 15 pc of India’s total Jewellery sales

Jewellery sales in India are highest during the Marriage seasons of - May - Jun, Sep - Nov and Jan. A lot of rural households in India invest their savings in Gold post the harvest season in Nov - Dec. Jewellery sales also pick up during the festive seasons of Diwali, Dhanteras and Akshay Tritiya ( Apr - May )

Industry is seeing a trend of youngsters preferring light weight Jewellery and consumers in general as a consumption item vs an investment item. Frequency of purchases have gone up due rising disposable incomes

SSSG for FY 25 vs 24 stood @ 26.5 pc

Stud ratio in Q4 stood @ 8 pc

Company launched ‘LiteStyle by PNG’ - a dedicated brand for light wt jewellery made in 18k and 22k gold. Currently 2 stores of this brand are operational in Pune and Goa

Q4 outcomes -

Revenues - 1588 vs 1512 cr, up 5 pc

EBITDA - 109 vs 91 cr, up 20 pc ( margins @ 6.9 vs 6 pc )

PAT - 62 vs 55 cr, up 13 pc

Segmental revenues for Q4 -

Retail - 1293 vs 861 cr, up 50 pc

E - Comm - 90 vs 26 cr, up 243 pc

Franchise sales - 185 vs 135 cr, up 37 pc

B2B bullion sales + Refinery operations ( discontinued in Oct 24 ) - 487 vs 18 cr, down 96 pc

FY 24 outcomes -

Revenues - 7693 vs 6112 cr, up 26 pc

EBITDA - 371 vs 278 cr, up 33 pc ( margins @ 4.8 vs 4.6 pc )

PAT - 219 vs 155 cr, up 41 pc

Company added 13 stores in FY 25. Aim to add another 23 stores in FY 26

Revenue per store for FY 25 @ 145 cr

Net profit per store for FY 25 @ 4.1 cr

Summary of Q1 FY 26 updates -

Revenues @ 1713 vs 1667 cr ( in Q1 FY 25, 353 cr of revenues came from refinery operations. These operations now stand discontinued wef Oct 24 )

On a comparable basis, Revenues are 1713 vs 1314 cr, up 30.1 pc

Segmental growth in Q1 FY 26 -

Retail - up 19.4 pc ( Retail segment represent 70 pc of company’s total revenues )

E- Comm - up 126 pc, now represent 4 pc company’s sales

Franchise Operations - up 109 pc, now represent 16 pc of company’s sales

B2B and corporate sales - now represent 10 pc of company’s sales. Refinery operations have been discontinued

Company recorded highest ever 1 day Akshay Tritiya sales of 140 cr in Q1

Stud ratio in Q1 ratio saw a sharp jump in Q1 and now stands @ 10 pc

SSSG in Q1 @ 8 pc - due absence of Gudi Padwa in Q1 ( as it was pre-ponned to Q4 this CY )

Opened 2 stores in Q1 ( 1 COCO, 1 FOFO ), taking total store count to 55. 7-9 new store openings are lined up for Q2. Company now intends to expand in MP + UP ( in medium to long term ). Should open a total of 23 stores for FY 26

Highlights from Q4 concall -

Since company has discontinued the low margin Refinery business, they expect sharp improvement in EBITDA and PAT margins for FY 26

Aim to open 13 full fledged PNG Stores + 10 LiteStyle stores for FY 26 with a broad 50:50 breakup between Franchise and Company owned stores. Should be entering UP + MP + Bihar within FY 26. By end of FY 26, company intends to be operating a total of 10 stores outside Maharashtra ( including 3 Goa stores )

By end of FY 26, company aims to incline their retail sales to 75 pc of company’s total sales - aided by strong expansion spree that the company is undertaking

Breakup of FY 25 sales -

Retail - 5327 cr

Refinery ( now discontinued ) + Corporate + Franchise + Online - 2301 cr

Aiming to clock 3 pc kind of PAT margins on a consolidated basis for FY 26 ( with retail EBITDA margins @ 7-8 pc )

Assumption : assuming a 15 pc topline growth for full FY 26 ( because of loss of refinery sales ), Topline should be around 8850 cr and PAT may be around 265 cr ( @ 3 pc PAT margins )

Traditionally, Maharashtra was never a studded jewellery friendly market. Company has made dedicated efforts over last 5 yrs to start growing their Studded jewellery sales. They have introduced various new designs of diamond studded, Polki Studded, Kundan studded jewellery and are now seeing encouraging response. Now they r strong growth in these categories led by - smaller base, higher Gold prices

Talking about old stores ( opened before IPO ),Value growth for FY 25 was @ 27 pc and Volume growth was @ 3 pc. These stores operated @ 6.41 pc EBITDA margins

The new stores that the company has opened in last 6-8 months are doing exceptionally well ( clocking EBITDA margins > 8 pc for last 2 Qtrs - although both Qtrs were full of festive and marriage seasons )

The store opening + inventory costs for a LiteStyle store are 8-9 cr / store vs 16-18 cr for a normal PNG store. Plus the margins in LiteStlyle fashion jewellery are much higher than traditional Jewellery

Disc : initiated a tracking position, not SEBI registered, not a buy / sell recommendation

3 Likes

gold value remains at prevelling market rate and labour charges are deducted ie any one can exchage old jewellery by simply paying off labourcharges and hallmarking charges apart from this if any stone/ enemal/rohdium charges and can get new jewellery of same wt

1 Like