CMP of OCCl Ltd is 97 rs…

Whether it seems like under valued after it demerger?

The chemical business alone posting a turnover of over Rs. 100 crore for the recent quarter is very heartening to see. Looks like some degree of recovery has happened. On a very crude basis, just annualizing the recent earnings translates to a P/E of ~16. With the balance sheet data available, Price to Book of 1.3 times.

2 Likes

has become quite a mess to understand OCCL and OCCLtd post demerger. One is a holding company and other has the business.

Anybody know if it is still on vijay malik’s portfolio

2 Likes

There is no mess created by the company.

Mess is in the mind of investors, who don’t like the valuations of individual companies post demerger ![]()

2 Likes

so this stable 100 Cr quarterly topline with a PAT of 7 Cr per quarter = 28 Cr growing at 8-10% YoY available at < 500 Cr Mcap ? which is roughly 15-16 PE

this kind of monopoly business with apparent 10% MS in Soluble Sulphur should be at least 30 PE ?

What are we missing ? Is it truly undervalued ?

1 Like

Why should a company growing at 8-10% with 7% npm get 25-30 PE?

30 PE is for firms growing in the mid-teens.

sorry, I didnt mention the growth prospects. Due to Electric Vehicles, the radialisation will be even faster (especially India) also the tyre wearing out will be faster than non electric tyres, the growth rate of the tyre industry (inflation plus volume) should be double digits going forward at least in India.

so half the business (in terms of Revenue) will be growing double digits for OCCL

2 Likes

Growth appears to be lacking, which is a significant concern. While the company generates decent free cash flows, these are not translating into higher dividend payouts or share buybacks, raising additional concerns. That said, setting aside the P&L challenges—likely driven by temporary factors such as high freight costs and increased global IS supply—the balance sheet’s strength stands out. The replacement cost valuation of the existing capacities alone could justify a decent re-rating, especially considering inflation over the past three years.

Disc- Invested

3 Likes

One thing that I noticed is that in the Oriental Carbon (Chemical company) they have restated the Q2 results there. But not in the main company (Insoluble Suplhur), so I have tried doing it, may not be fully correct but here it is.

Oriental Carbon & Chemicals Limited is the parent company which is an investment holding company.

OCCL Limited is the chemical company (Insoluble Sulphur). The company has created unnecessary confusion around names.

2 Likes

HDFC fund house reduced the stake from 8.6% to 6.5% something

no wonder, stock is not able to sustain over 95-100 range last two weeks.

Sharing my thesis on OCCL (Operating business now demerged from Oriental Carbon)

Background

- The business of insoluble sulphur (IS) is niche business , oligopolistic in nature with three players capturing major market share excluding china (Solutia - 60%, OCCL -10% and Shikoku -15%).

- Players from China (e.g. China Sunshine) used to cater majorly to chinese markets, however, situation has changed now.

- Its low asset turnover business, where you have to invest Rs 1 for generating Sales of Rs 1. However, its a high margin business with 25-30% EBITDA in steady state when demand supply is in balanced state, which makes it 15-20% ROCE business

- IS is majorly used in tyres as an important additive and disruption risk is minimal. However, total world wide addressable market is small ($2 billion).

- There is stringent approval process from tyre companies , which may take 18-24 months to complete, to become their supplier.

- OCCL has 39,500 MT capacity and derives 50% sales from india and 50% from exports.

- Consumption of IS follows cyclicality of economy, in good economic conditions, there is lot of commercial activity, usage and consumption of commercial tyres increase a lot.

Growth

Its a steady industry with long term growth rate of 5% globally. However, for investors, growth is not the only ingredient to make reasonable return in the market.

In cyclical and ignored industries, Mr Market sometimes offer deals that may prove to be good bargain.

Current situation

For more than a decade, IS supply and demand dynamics were in balance, and so , prices were stable and EBITDA margins was north of 25%.

Chinese players were confined in china.

However, during last 3 years, lot of capacity is built up in china, which coincided with economic slowdown, which has caused chinese players to start dumping IS to india.

OCCL has to let go its margin to remain competitive in current situation, which has dampened its profitability.

However, OCCL is cost competitive when compared with chinese players and can compete this attack. Its balance sheet is strong with negligible debt and it has capacity to suffer. Anti Dumping Duty is what OCCL is trying to get imposed, but will it succeed, I dont know

Same situation occurred in past (2006-08) and OCCL has able to handle it. However, when the situation will turn, no body knows, 2 years, 5 years, 10 years, I don’t know

Valuation

Currently OCCL trades at 450 Cr Market cap with 400 Cr sales and 30 Cr PAT. Both sales and PAT are depressed due to low pricing and low capacity utilization (70%).

Recent Capacity addition of 5500 MT is not utilized due to low demand but it is adding to depreciation, impacting profitibility. Further Capex of 5500 MT is halted due to same reason.

When situation will turn (which I dont know when), base on my estimates the sales can reach 700 Cr and Profits will hover around 125 Cr (I dont want you to agree with these estimates, You need to work out your own estimates)

Is current valuation reasonable, is for the investors to decide.

Promoters

In the past promoters have not taken minority investors for a ride. They has done buyback when they thought price was favorable and when they were questions by investors on unrelated investments, they did a demerger to spin off the investments from OCCL.

The dividend policy is framed as 50% of PAT and management talks candidly about their views on the business.

Disclosure - Invested and biased. Not a SEBI registered analyst and this post should not be construed as a buy/sell recommendation

6 Likes

Before the demerger OCCL was doing 5 times business of Oriental Carbon (based on the revenue generation). Current price of OCCL Rs.85 x 5 = Rs.425 is only two times of Oriental Carbon’s share price of Rs.212.

Once both companies present their annual report this year, probably the price of Oriental Carbon will come down and the OCCL will go up.

The DII shareholding pattern is not very much clear here. The numbers of Oriental Carbon from September are put for OCCL in December. Though it’s mentioned as new-buy in many reports for HDFC, it looks like it is the demerged component which is yet to be consolidated.

1 Like

OCCL is suffering from a demand fall in insoluble sulphur in Europe/USA and dumping of insoluble sulphur in India by China & also by the leader in the segment Flexsys. This means it is being hit both on sales growth and also declining margins, and very low capacity utilization with machines being idle

Some triggers for the stock can be:

- Increase in demand for insoluble sulphur (likely 2-3 years away and an ‘if’)

- Anti-dumping duty levied by Govt of India (can never predict ‘when’)

- Company finds another business with 70% of its capacity lying waste

- Management is ethical, however they have done unnecessary complication by hiving off all the investments as a holding company

Balance sheet and cash flows are strong. It is trading at low P/E and risk in owning this company is very less. I bought a truckload of this stock as I think trigger can happen in next 3 years

This is the kind of stock that will give all returns in 1 year and it could be flat for 3 years and become 3x in a year. I bought this as a hedge against stock market crash. I don’t think it can go much lower given depressed valuations. The upside is not dependent on the beta with the market

7 Likes

Notes of Q3 FY25 Concall held today:

- Global Alliance - On asking what the management thinks about the Global alliance, that was guided pre-demerger, it was bluntly mentioned that any kind of alliance makes sense, when Maket cap / valuation is in company’s favor. Current valuations are depressed/distressed and hence alliance does not makes sense at all.

- Supply Demand Balance - Global demand supply of insoluble sulphur (IS) is imbalanced now. With global growth in IS of 3% it may take 4 to 5 years for the existing IS capacities to be absorbed. OCCL current utilization is 70% , which may climb to 90%+ when that happens and operating leverage will kick in.

- Fall in IS selling price is due to excess supply globally, where as Increase in Costs is due to High freight rates.

- Anti dumping duty implementation and fall in freight rates can be positive in short term, where as firming of IS price will be positive in the long term.

- Current IS prices has little scope of further correction, and neither anyone has incentive to put new capacities at current IS prices.

- This is one of the specialty chemical company where rather than china +1, chinese players entered from no where and messed the IS market.

The notes above are probably what I wanted to hear, rather than what was actually discussed, which is how the human mind is designed. So, better read the concall yourself.

3 Likes

3 Likes

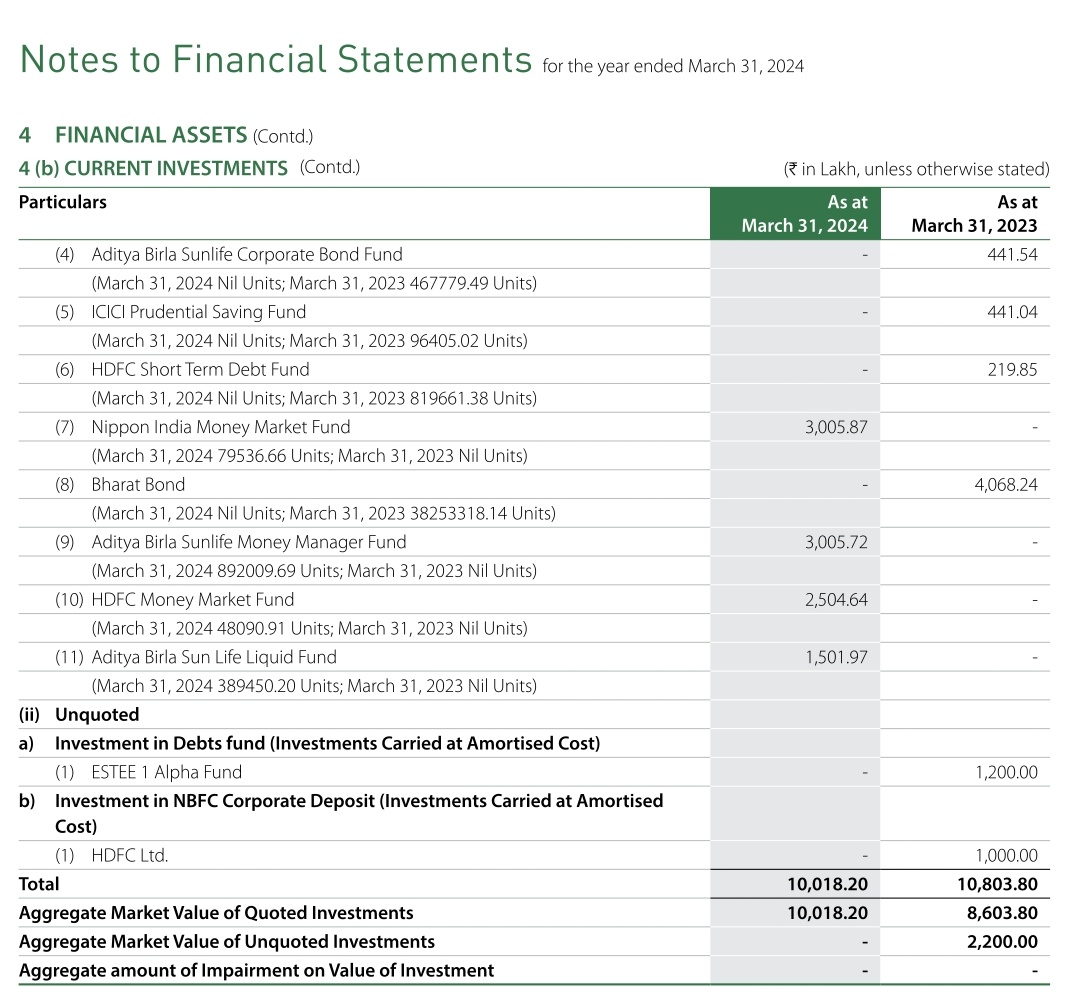

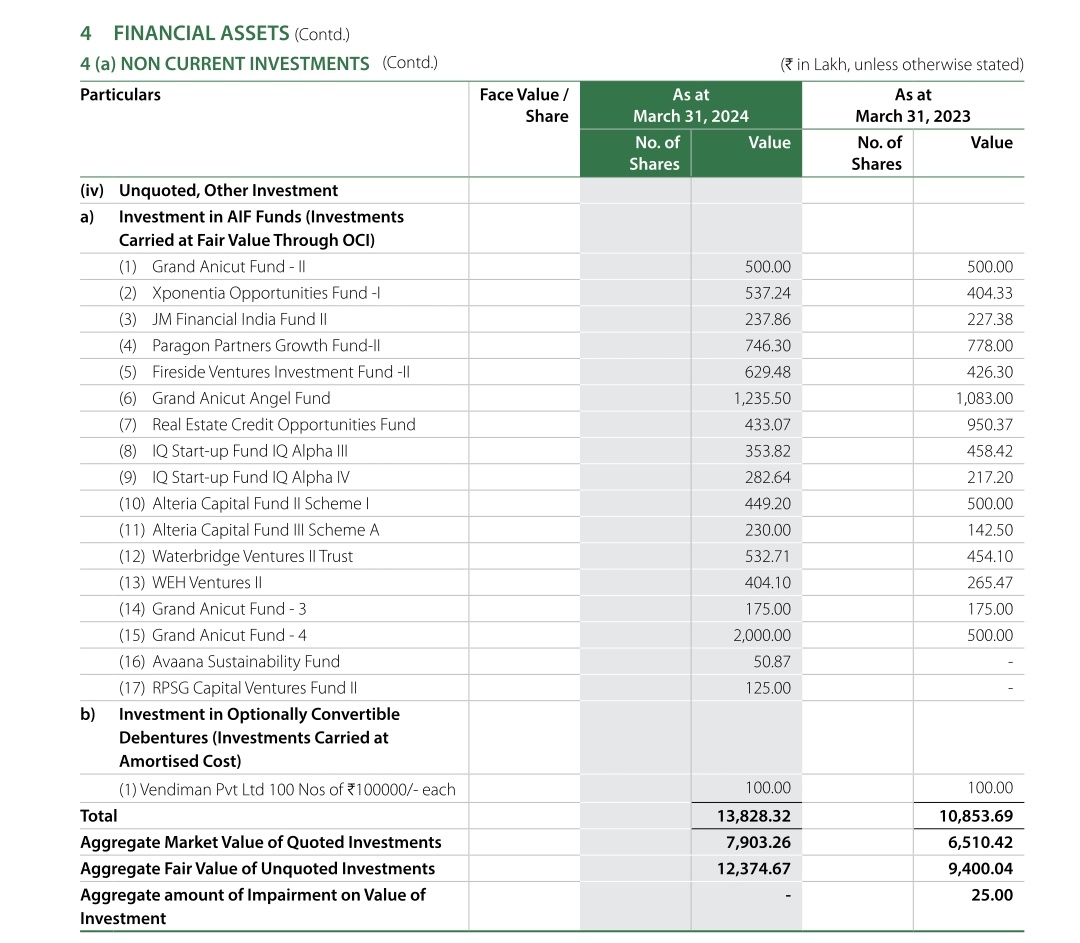

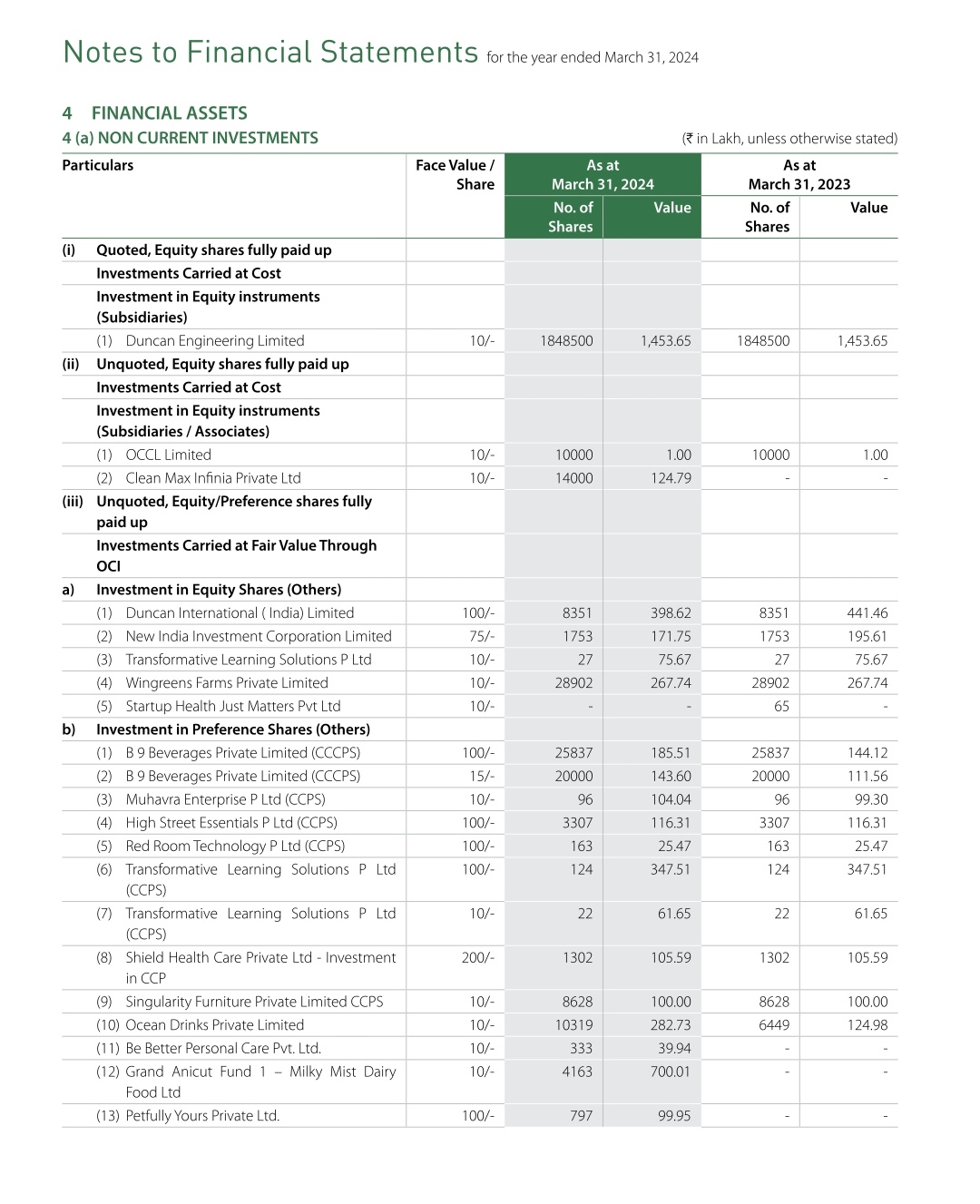

Anyone tracking the demerged investment business? Can and should it be thought of as a typical holdco?

Also, I think the book value reported is deflated because it doesn’t correctly value the Duncan Engineering business.

If you pull the FY24 AR, the investment business has 18.5L shares (ie 50% stake) in Duncan Engineering valued at 14 CR when it should be much higher than that (as of the last closing price of Duncan Engineering, that should be about 70 CR).

So as per me the book value of this business is about 300 CR and not 264 CR (as shown on screener).

Here is my calculation

A) Current investments: 100 CR

B) Unquoted non Current investments: 124 CR

C) Duncan Engineering stake: 70 CR

A+B+C = about 300 CR

1 Like

If you look at page 11 of the September 2024 results declared by the company, you will see that the equity attributable to the owner of the parent is 263.59 crores which is what screener is showing as the book value.

Ok. Coming to the question of valuing the stake in Duncan Engineering. The company has invested about 14.53 crores in that business and they will always show it at that cost value in its books. On page 133 of FY24 Annual Report the company states the following

Investment in subsidiaries is carried at cost.

Since Duncan Engineering is a subsidiary the company will not show the value of their stake at its current market value as per their chosen policy. In my view this shows a conservative management.

But yes as investors we know that the current value of their 50% stake as per the market cap of Duncan Engineering is 70 crores.

4 Likes

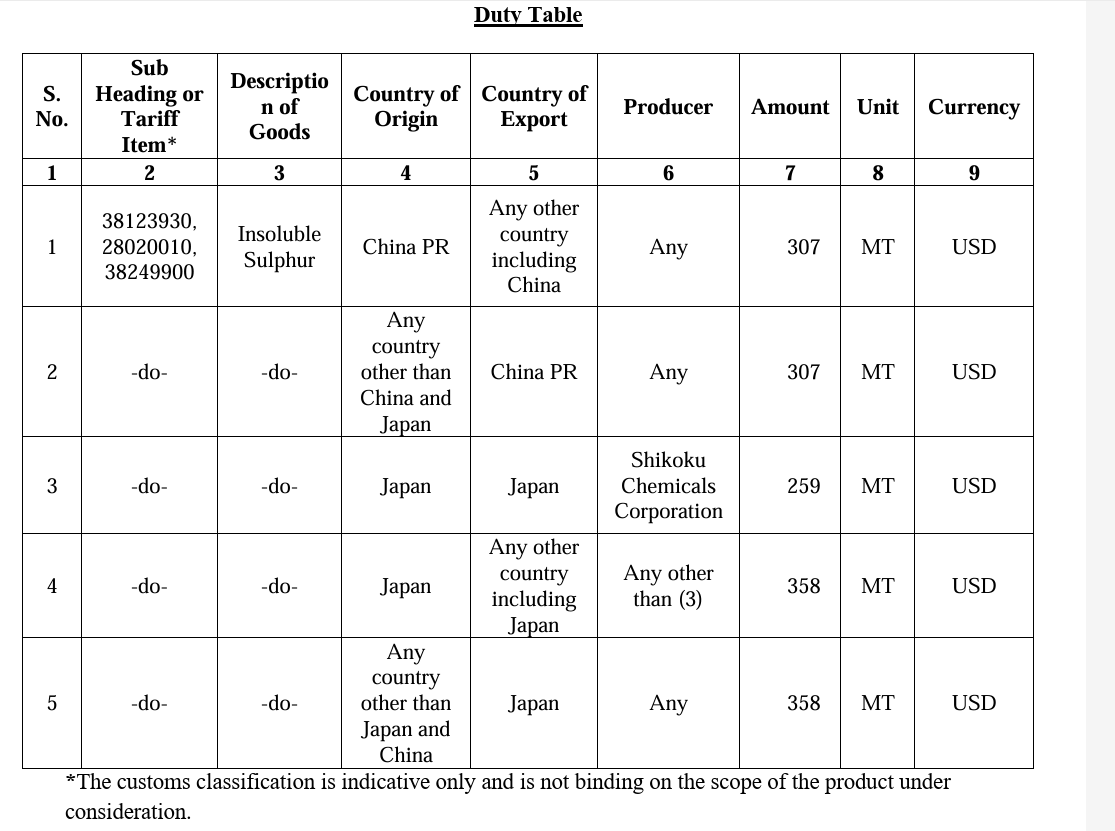

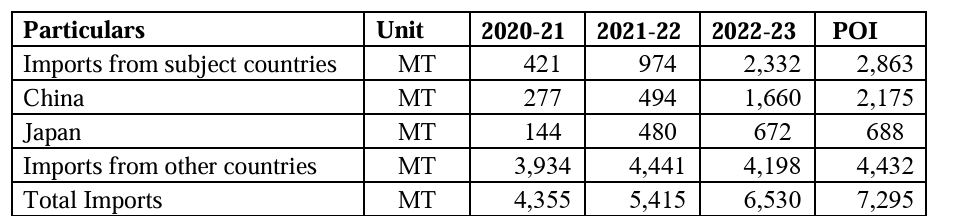

I was trying to break my head with the Final Finding Document on Anti Dumping Duty (attached below) imposed on China and Japan for Insoluble Sulphur (IS). It is a very informative document but lengthy and hence requires enough time commitment to do justice with it.

Based on the document, I understand that roughly 300 USD ADD is imposed on every MT of Imported IS.

At selling price of ~Rs 120,000 MT, the ADD will entail additional cost of Rs 24,000 (300 USD * 80), roughly 20% more. As OCCL sells 50% of its capacity in domestic market, it looks that the company will be protected from import dumping for half of its revenues.

(These are my estimates based on the data, and it may be completely wrong).

Excerpts below:

Few other interesting observations:

MRF confirms Insoluble Sulphur constitutes 0.17% of the cost of tyre

The raw material (Sulphur) is derived from Crude oil

Claims made by Exporting parties

Import Volumes from China and Japan

FF Insoluble Sulphur English version.pdf (756.7 KB)

8 Likes

Notes OCCL Q4FY25 Concall

-

Major insoluble Sulphur players include 2 in China (China Sunshine, one other), 1 in Japan (Shikoku) and 1 in USA (Flexsys). All insoluble players have strong balance sheet. All other players produce basket of chemicals, only OCCL is pure play Insoluble Sulphur producer.

-

Flxsys has plant in Malaysia, from where it supply to India. It’s not possible to supply from US as it will be too costly.

-

At current prices, it does not makes any financial sense for new player, even in China to start new capacity.

-

Sulphur (Raw Material) price have remained elevated at around $300 this year. Chinese players are dumping insoluble Sulphur at $900 in India.

-

Proposed anti-dumping duty is ~$300 / MT for China and ~$250 / MT for Japan. Antidumping duty is under approval process from finance ministry, and if approved, it may be effective from June 25.

-

As the global demand for Insoluble Sulphur grows by 3% annually, and the fact that existing players have increased capacity significantly, apart from anti-dumping duty in India, there are no other triggers of margin improvements for OCCL as of now.

-

Rs 3.5 Cr was paid as stamp duty for demerger process this Quarter, excluding it, margins would have been a bit better.

-

Current capacity utilization at OCCL is 70%.

Disclosure - Invested and Biased

1 Like