Had a chat with an analyst who recently contacted the management regarding the equity dilution. The management said when they acquired the company it had very bad financial condition and debt to equity was 3.4 with accumulated loss of 48 million. More debt required for growth at that point would have been disastrous. Hence they issued warrants and it was converted in a staggered manner. At the moment there are no outstanding warrants against the promoter management sounded very positive about it’s financial health.

1 Like

@ayushmit Can you please throw some light on the findings you gathered during the visit to the plant last time? Did you visit their Surat Plant or Kalyan Plant?

Hi Nitya,

I did not visit their plant and havent been tracking the company off late.

united arab emirates trading comanies are basically front companies …need to see that is company expanding it’s foot print in middle east region …then only it is logical … otherwise it is book dressing of some nature

disclosure - have a small position

This looks a very interesting story to me.

It has grown profits at 50% in last 5 years and 43% in last 3 years. Operating Margins have gone up from 6-7 % to 30% levels at 30% ROCE this looks to be a good value buy at 18PE

Some watchouts

There has been equity dilution over time.

Debt keeps increasing and Interest costs seems too low for the level of debt??

1 Like

Massive drop in share price today. Any feasible explanation?

Point to note : Receivables kept on increasing every year. Debtors turnover ratio got poorer with time.

Investors took the opportunity to get out of stock. Constant diluting equity 5-8% each year does harm minority shareholders.

- Constant equity dilution over the years

- Consistent Increase in debt

- Increasing Receivables over the years

Questions

- Are these problems related to each other?

- Are these the symptoms of more serious and deep seated issues?

Ayush,

Hope you are still tracking this company based on your questions in orbit’s Q2fy16 concall.

How do you foresee the company now based on currency issues faced by it in Latin america?

Hi Rajesh,

It was strange to know that they had exposure to South American Countries and got affected due to currency headwinds. I’ll like to give some more time and get more clarity about these things.

Regards,

Ayush

1 Like

bad set of results from Orbit topline and bottomline degrowth yoy.

Hi Ayush hv u got clarity on the Orbit exposures and what went wrong last few quarters!!!

Can we launch Complaint with Company / SEBI ?

The company seems to have lost its mojo!!!

It has invested Rs 130 Crs in Fixed assets from FY14 to FY20. The sales has remained flat over this period of time

Now it has proposed a further capex of Rs 44 Crs towards which it has just acquired the Land & Bldg

Its a good dividend paying company, having near zero debt, conducting buy backs in which the promoter does not participate.

Where is the capex money going?

1 Like

de9f1edd-966a-4c7b-8581-292176c615fc.pdf (5.6 MB)

Good improvemwnta in results on yoy and qoq basis…

2 Likes

There is a healthy increase in sales translating down into the PAT as well. It is important to understand where is this Profitable growth coming from and how sustainable is it. Interest cost has significantly increased

2 Likes

The company has delivered a good quarter with sales around 40 crores(in a seasonally weak quarter) and PAT 5.5 crores. All this is despite higher depreciation and interest due to recent capex which should hopefully start bearing fruit soon as mentioned in the annual report. It seems to be turning around after a dismal 2020 due to covid. This is one of the niche textile players which can benefit as people start going out again(evening wear). Risk of global demand tapering due to inflation remains.

Anyone tracking and has any additional inputs?

Disc: Invested

3 Likes

I had done some work on Orbit Exports and following are some notes. There are a few things that need to be established on nitty-gritties of growth.

Orbit Exports is a weaving company, primarily in polyester space, manufacturing novelty fabrics. The company makes - silky fabrics from polyester (think designer curtains, decorative items in furnishing), jacquards (design integrated in weaving) and Christmas articles. The products page of the company provides good description (and feel) about products. (Silky Aspects | Orbit).

The company has consistently made 25%+ margins for last several years. Since company makes novelty fabrics, occasion wear or decorative items - it is intuitive to see why the margins would be high. With such niche products, the issue is of scalability. The nature of the sales is small sized orders distributed over a large number of clients vs few clients with large orders.

WHAT IS EXCITING/CHANGING

The company has been stuck in 140-150cr sales range for last 10 years. But in annual report for FY22, company came of with aspiration of reaching 4x FY22 revenue by FY27. FY22 revenue was ~125cr, so company is looking to get to ~450-500cr revenue by FY27. If this happens, this would be tremendous growth.

The two underlying levers to achieve this growth is - China + 1 and domestic business.

Out of the two, domestic part is easy. The company always focused on export business and they suffered in pandemic years due to travel restrictions, shipping issues. So company wanted to develop/capture the domestic market opportunity. The company has set target of 30-40% revenue contribution from domestic market. Since domestic business is at low base, one can envision that growth in this segment is sort of low hanging fruit.

The margins in domestic market would be lower than export markets and receivable days might be slightly longer. How company addresses/manages these challenges needs to be seen.

The growth in export markets is what needs deeper work. MD mentioned in AGM about China + 1 but we need to do next level work to establish this.

CAPACITY/CAPEX

Company’s website mentions that company exports 2 million meters of fabric every quarter (About Us | Orbit). Over 5-6 years, approx 70-80% revenue of the company is contributed by exports. So one can estimate that overall capacity of the company is ~1cr meter per annum.

If we read notes to accounts for Q1 FY23 results (https://www.bseindia.com/xml-data/corpfiling/AttachHis/c137c5dc-9586-4f8c-bc1e-19de0a433761.pdf), one can see that company is looking to expand the weaving capacity by 20% in FY23.

In year FY22, company has capitalised ~60cr of capex - this includes land of ~25cr and plant & machinery of ~35cr. This capex is a forward integration capex and not a growth capex.

The company has invested in post processing/dying house. The company primarily makes novelty fabrics through weaving but end customer needs more than fabric to make his novelty product. Company had to outsource this part and depend on third parties. This obviously created following constraints -

- supply constraints - where company can not promise aggressive delivery schedules to customers

- design constraints - team can not experiment and develop new designs and test them out. Also probability of design leaks.

- quality constraints - dependence on third parties to get desired quality, fashionable looks for final product.

With own processing house, company can now - can promise fast delivery schedules to important customers, closely guard its designs and develop new designs and have closer grip on final quality. This capex improves the competitive position of the company, it provides ability to enhance customer experience.

On financial front, this capex is expected to also add to margins. How and when it happens remains to be seen. The capex would have some learning curve, stabilisation and ramp up efforts.

This capex has also built large civil infrastructure and land is quite big. So increasing weaving capacity from hereon - is just a matter of importing/purchasing looms.

SEASONALITY

The company produces novelty fabrics which are mainly get used around festive period - Diwali, Ramazan, Christmas. Company needs to supply fabrics to final product manufacturers 4-6 months in advance after which customer creates final products and they need to go on display 1-2 months prior to festive season becomes. Due to these reasons, Q1 is usually one of the best quarters for the company.

With domestic business ramping up (where shipping times would be less), hopefully seasonality will reduce going further.

RISKS/UNKNOWNS

-

More granular work needs to be done to establish the competitive landscape and China + 1 opportunity.

-

The company’s revenue is distributed amongst large number of customers with small ticket size. 2-3 customers with large order book can not take company to next orbit. Scalability needs to be seen.

-

My understanding is that design team is currently small at 10-20 people. I would like to see consistent investment in design/people and sort of institutionalise this area which should eventually result in consistently breaking into and scaling up new customers. For small companies, it is hard to establish this.

-

Company already trades at 17x TTM PAT (Mcap ~ 525cr, TTM PAT 30cr). Company is in textile segment and might not get high exit multiples.

-

The company went through lean phase with COVID disruptions and fire at Bhiwandi warehouse. Normalisation story has already played out with stock price running up. Stock price performance from hereon will depend upon execution of growth plans.

-

The company’s business is seasonal in nature with H1 being heavy half. In H1 FY23, company has already reported 104cr of sales and PAT of ~20cr.

BRIEF HISTORY

- 1995: Initial Public Offering (IPO).

- 2004: Taken over by the new management under the promotership of Mr. Pankaj Seth and Mrs. Anisha Seth.

- 2010: Set up a new fabric manufacturing plant at Kosamba, Surat.

- 2013: Acquisition of 49% stake in Rainbow Line Trading LLC, UAE.

- 2013: Incorporated a wholly owned Subsidiary Company – Orbit Inc in Los Angeles, USA.

- 2015: Recognised by Forbes as “best under a billion” in Asia.

- 2021: Fire at warehouse in Bhiwandi

- 2022: capitalised process house

- 2023: 20% weaving capacity expansion

MISC POINTS

- Roughly 80-85% of the company’s sales are from fabric and 10-15% sales are from made ups. Made-ups (both occasion craft and decorative items) has better realisation that fabric.

- AR22 - company entered into sales arrangement with large made-ups retailer. Company expects to double the sales in made-ups in 3 years.

- Company has 51-49 subsidiary in UAE named Rainbow Trading LLC. The primary sales are in UAE itself and in middle east region. One can see the warehouse/shop on google maps. (Rainbow Line Trading, (Distributors & Wholesalers) in Al Fahidi (Al Souq Al Kabeer), Dubai). 49% investment from partner is a regulation in UAE.

- One of the players in Jacquard/Weaving space that I have been able to find is VTM Ltd (VTM Ltd financial results and price chart - Screener ). They do not make margins anywhere close to Orbit. My understanding is this is due to - 1) VTM has majority cotton weaving vs majority polyester weaving for Orbit 2) Niche nature of products for Orbit.

TODO

- More work needs to be done to establish the customers of Orbit Exports. Some of the customers that I have been able to gather are - The Children’s Place, Calvin Klein, Raymonds, H&M, Manyavar etc.

- We need to be able to find competitors in exports market, especially Chinese competitors and understand their scale/products/margins.

Disc - Invested from much lower levels. This is not a buy/sell recommendation. I am not SEBI registered analyst. I may change my opinion and sell at anytime without informing the forum. Normalisation story has already played out in the stock/business.

26 Likes

Following is the list of major customers they have revealed in AR 22:

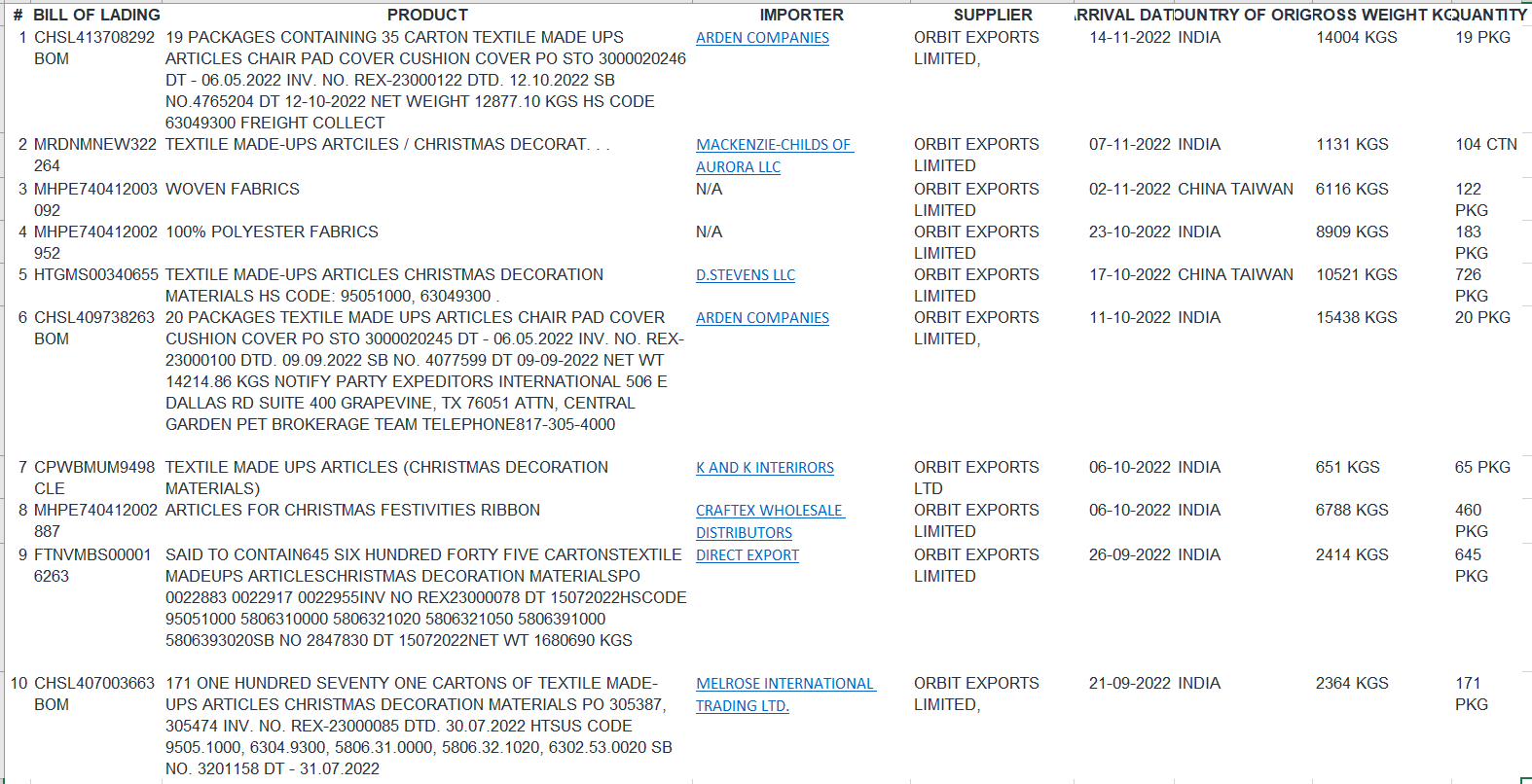

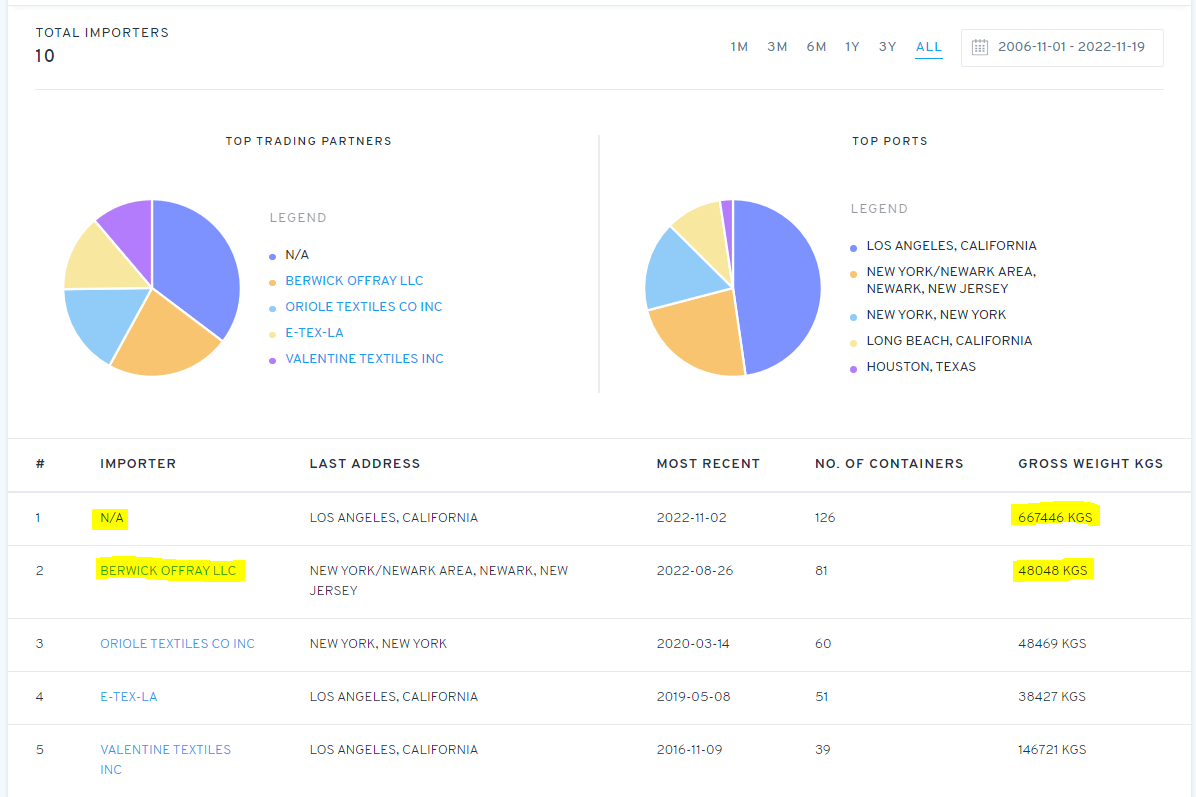

Here is the recent 10 consignment data for export to US by Orbit, most of them are made up articles(due to upcoming festival seasons).

Source: Orbit Exports Limited | See Recent Shipments | ImportGenius

There is one customer (name undisclosed in this portal) which done the most transaction in volumes (fancy fabrics). The second largest is named Berwick Offray LLC.

It was a sweet surprize while found that,

A subsidiary of CSS Industries, Inc., Berwick Offray, LLC, is the world’s largest manufacturer and distributor of decorative ribbons and bows produced by both woven and non-woven methods .

Few other major customers from North America are Arden Companies, Inc (America’s leading manufacturer and marketer of outdoor cushions and pillows), Oriole Textiles (for made ups) etc.

9 Likes