This is how bad management can ruin your otherwise good investment in good business…What a misuse of ESOPs!

http://www.bseindia.com/stock-share-price/stockreach_insidertrade.aspx?scripcode=532466&expandable=2

This is how bad management can ruin your otherwise good investment in good business…What a misuse of ESOPs!

http://www.bseindia.com/stock-share-price/stockreach_insidertrade.aspx?scripcode=532466&expandable=2

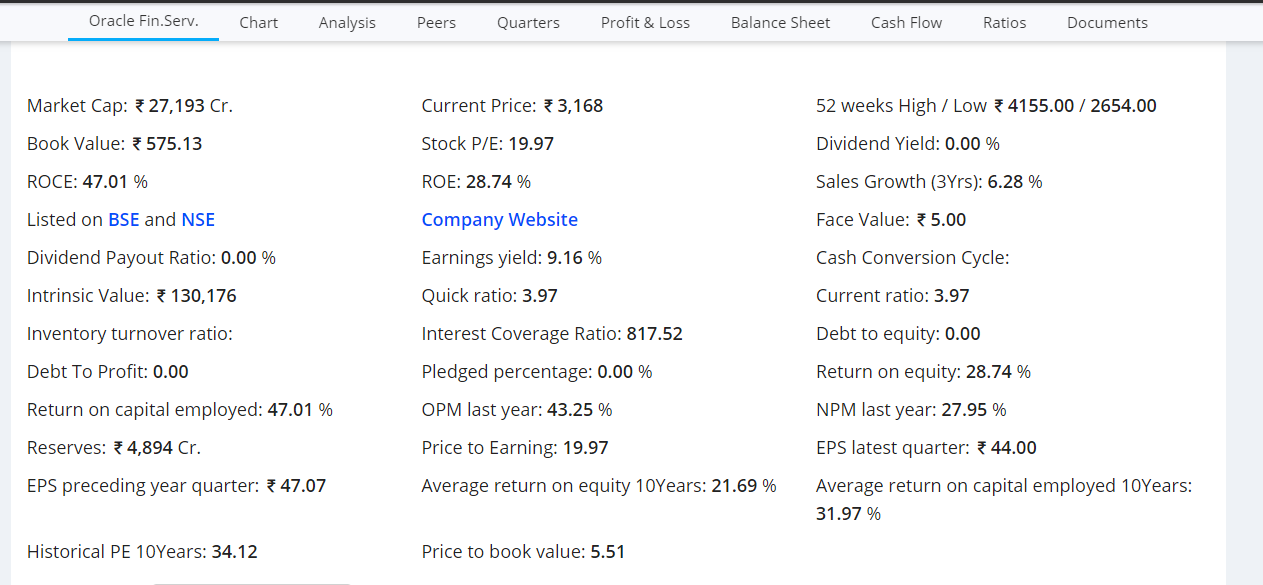

Isn’t this stock attractive at current valuations ?

Earning Yield: >9%

TTM PE: 19

BV: 5

DIV PAY OUT : >90%

I think this will not benefit from the Current Corporate Tax decreases as it has foreign owner. But despite that it’s looking good.

One more thing , because of attractive tax rates, any domestic company can go ahead and buy the company and then pay less taxes. (Most likely may not happen, but we never know)

Disc: Not invested, but exploring.

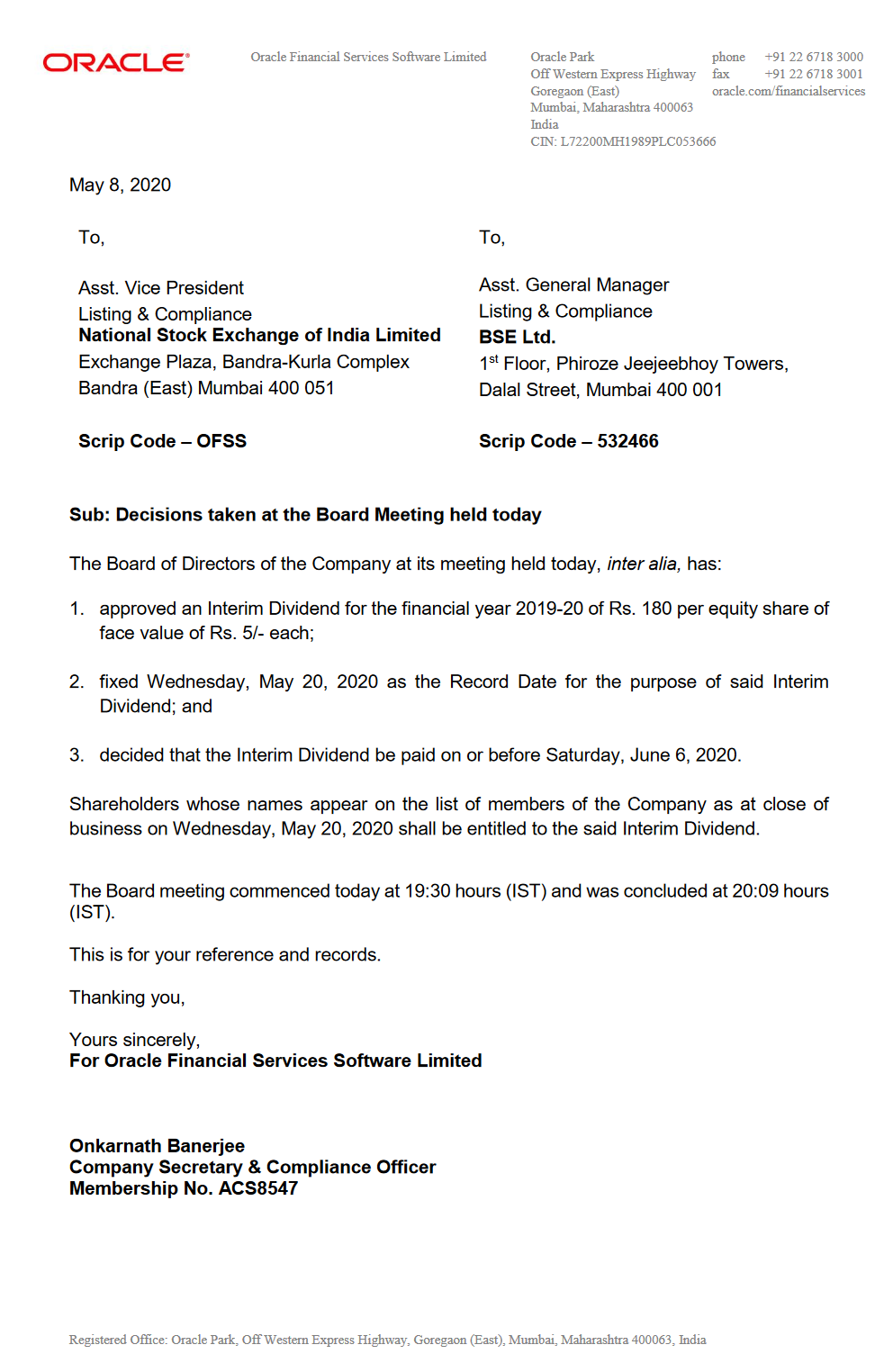

What about 2019? Did they declare the dividend this year?

Pattern seems to be like -

Accumulate cash for few years and then return lump sum to shareholders.

I am tracking this stock for some time as well. What is the long term growth rate for Oracle as all companies are moving to cloud and as per the preliminary feedback , Oracle has no cloud software. I am not an IT expert, so someone with understanding of IT and Oracle products can advise on long term sustainability of company.

If the company can grow at same rate as in the past then it is worthwhile to buy and hold at current price.

It seems they did not give any dividend for 2019. But that doesn’t mean that they will not return in future. Their track record is that all FCF is given as generous dividends.

Is their any impact on OFSS due to PSU bank merger ? Finacle licensing ?

Finacle is an Infosys product. Oracle Core Banking System is called FLEXCUBE (wrongly mentioned as i-flex in the table, i-flex is the older name of the company itself).

With Canara Bank merging with Syndicate, Oracle gets a new project to implement. So short term, the merger is positive.

In the long run, two customers will reduce to one. Pricing in these types of products is a complex thing and generally depends on mutual negotiating power. As a design, pricing is a mix of license fees (which in turn could depend on many factors such as number of users, branches, modules used etc.), AMC support required, customizations, ancillary products sold along with the CBS such as hardware like database and servers, reporting tools, internet banking and so on. Costs will also come down for Oracle as fewer people will be required to support one large client instead of two separately. The net effect is difficult to assess for us outsiders. But whatever the impact, I think it may not be significant in terms of the company’s total revenues.

(Disc.: No position)

Only 8% of total revenue in local, rest comes from outside India.

Only concern I have is sudden reduction in employee expenses and employee count. Are they downsizing? Layoffs?

On the Gartner score, the Oracle digital banking product scores less than Infosys/Temenos.

It scores very well on retail banking product

https://blogs.oracle.com/financialservices/oracle-a-leader-in-2019-gartner-magic-quadrant-for-global-retail-banking

It is their insurance product which is top quartile, though does not look like a big portion of revenue.

After skipping dividend last year,now they have a board meeting on May 8,2020 for declaration of interim dividend.

can you explain this part?

Its disappointing that they skipped dividend with NO explanation with logic. One cannot be a part owner without any logical conclusion on when or when not profit will be shared.

Consistency is important. My sole reason to avoid this counter despite valuation ease.

Stock is at 2600 per share and with dividend of 180 bucks cost of the acquisition comes down to 2400. That’s is equivalent to market cap of roughly 20k crores. With another 1500 crores cash which gives an EV of 18500. Last year it had fcff of 1500 crores. Which indicates a 8% FCFF yield.

What could be the downside risk (10%-20%) to FCFF during 2021/2022? Is this a sticky business?

Interesting observation. Don’t know why there are not many comments about this company in this thread?

It’s an unloved stock. Majority shareholders do not care about the stock price. Brokers not interested as there is not enough liquidity in the name so not a lot of interest from the buy side. And institutions do not find it in the “hot” sector as it grows at only 10%.

With the recent dividend it was at trading at a 6% dividend yield and add a 10% growth on that which gives you a return of a cool 16%.

Disclosure: Invested.

Hey there!

I would like to tell my (shareholder) side of the story.

First of all, I love to invest in listed subsidiaries of Global MNCs in India.

(Invested in Siemens, 3M, Honeywell, Heidelberg etc)

The most important reason for me to ignore this stock, was due to its struggling parent. Oracle has been the name of past which maybe didnt adapt with time.

In cloud infrastructure, it’s biggest competitor is AWS and MS-Azure. Amazon is, well, known to disrupt every industry it’s present in.

The next big thing is Cloud softwares, here too, Salesforce leads the pack.

A decade or so, ago, Oracle’s ERP was the best, but companies have since start to offload it.

Not that I (or anyone should) follow big investors, but Buffett too, sold his stake in Oracle.

These things are related to the parent company and not the Indian subsidiary per se, but it is a big red flag for me (may or may not be someone else).

There might be some corporate governance issues as well →

Coming to the Indian subsidiary, their 10-year Sales and Profit growth have been mediocre at best, hence I considered other alternatives.

Disc - Not invested.

Oracle has another (private) subsidiary which provides services in cloud infrastructure actually called Oracle India Services Private Limited. I am not sure happy about the business being separate (other MNC’s Pfizer, Sanofi, Abbott have separate private businesses as well) but it’s not the end of the world for me.

Also, i always thought that Oracle strong suite was the financial services space but i could be mistaken. I still have to do more work on that and maybe that’s the risk in my investment thesis but at this valuation i have enough margin of safety to take that risk. For me I understand more about the business once you are invested in it cause I have skin in the game.

Didn’t know re the bribery charges but that’s 8 years back thanks for flagging that and the management team has changed post that. One can argue that it could be a culture issue but if it was then you would have more cases that would come up.

As far as the discrimination cases are concerned if i had a penny for every discrimination case that were settled by businessess i would be rich. I don’t see a slew of class action suits so i am okay with it.

Yeah can’t argue with WB actions out there. He also invested in airlines twice in his life  but again I consider them statistcal anomalies and over a portfolio has a great track record. Just to be clear I am not looking for “consistent compounders” I am looking okay biz with reasonable balance sheet and franchisee which throw out cashflow, decent growth and do not use a lot of balance sheet size.

but again I consider them statistcal anomalies and over a portfolio has a great track record. Just to be clear I am not looking for “consistent compounders” I am looking okay biz with reasonable balance sheet and franchisee which throw out cashflow, decent growth and do not use a lot of balance sheet size.

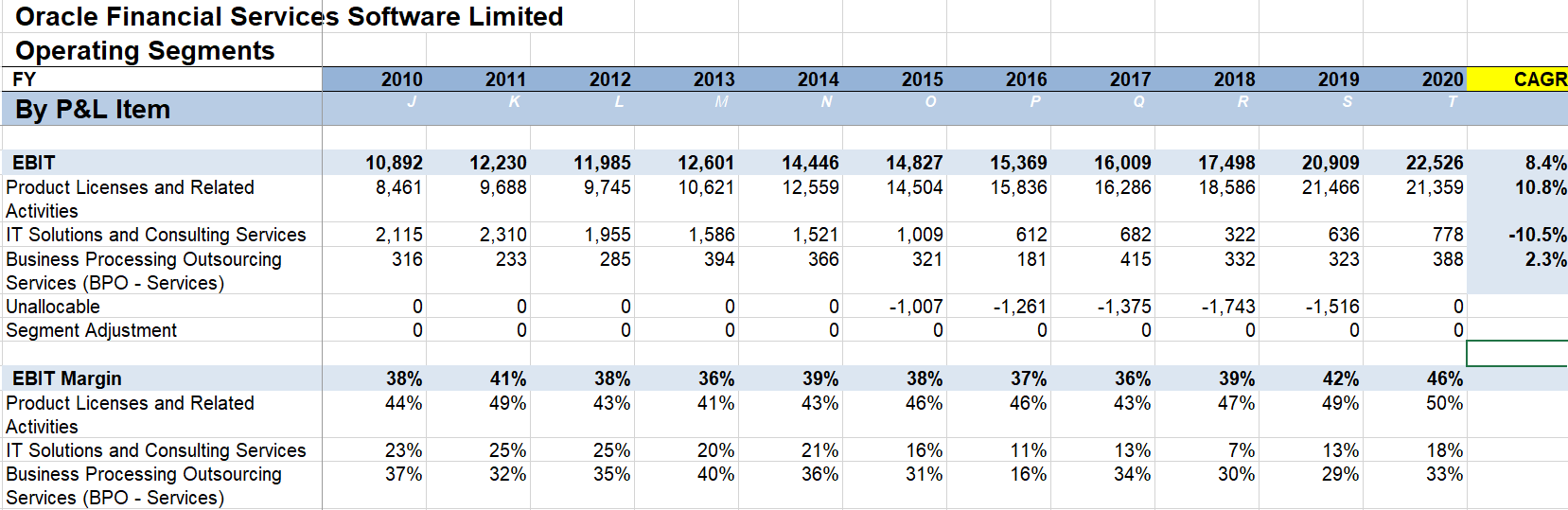

So if I look at Operating Profit increased from 100 crores (2010) to 220 crores (2020) that’s a little over 8% growth. The ROC’s of this business has doubled from 23% to 47% during the last decade. It doesn’t get me excited yes but if i get it at a value of <8x EV/EBIT(that’s like a 12.5% yield) when I think i have enough margin of safety to start a position intiated the position .

My expectations are: a) Growth 8-10% + b) Multiple rerating for a steady eddie (i can see all those pension funds salivating at these yields) like this 8-10 (4.5% annually) + c) Dividend of 6%. If i do the math over a 5 year period i am at 18%-20% returns. That’s why it made sense for me. Possibly there are better opportunities out there but this kinda made sense to me.

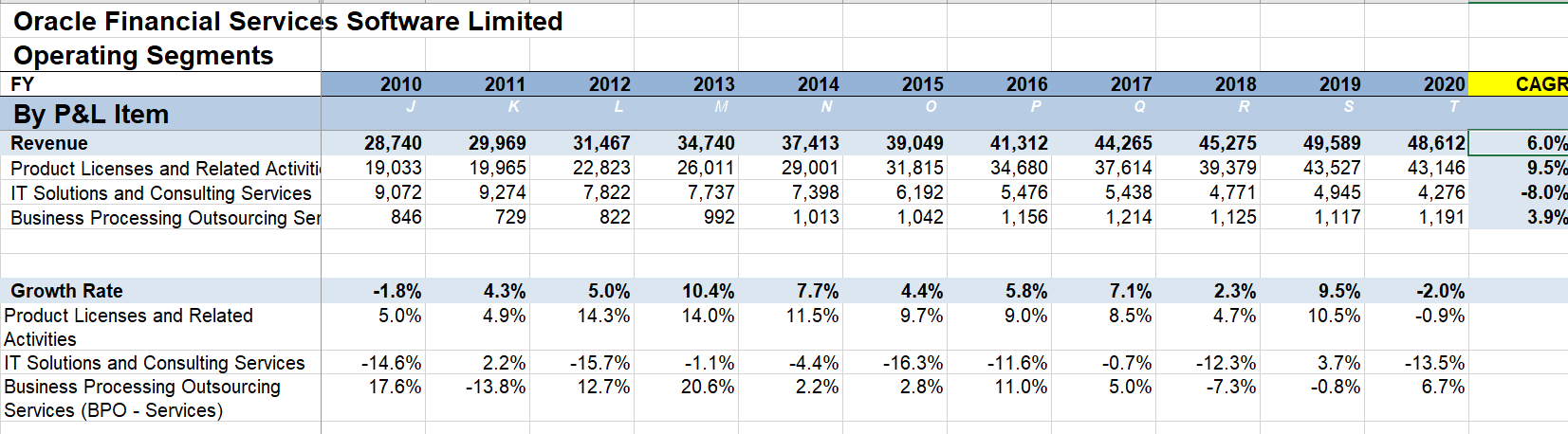

Just a few more details since we are at it. Following is the revenues by segment.

So the product and license segment (which is the sticky core part of the biz) has grown by 9.5 %ish over the last decade which ain’t so bad while EBIT has grown by 11ish %. So the core contributors are growing at a high rate while the detractors to performance are really the IT consulting and the BPO business. To be honest I am not super clear why do they do those businesses/what is in those business. As you might have guessed the IR isn’t very reachable. I plan to do more work around these biz.

A Detailed Analysis with Highlights of Q1 2021 performance of OFSS by the Management…

https://documentcloud.adobe.com/link/track?uri=urn:aaid:scds:US:a9128fb1-8e38-4dc3-8497-7deadaa3a2c9