Just to give a perspective the following are pointers from Balance Sheet at consolidated level-

Book Value- 2114 crores

Trade Receivables- 1584 Crores

Market Cap- 553 Crores

Now, the market is giving a medical equipment business 1 P/B even after assuming that entire trade receivable is bad debt. This is for a company which has historically created significant shareholder value and is currently under fire due to over aggressiveness of promoters. Management seems to come to media and commit a lot every now and then but nothing much in visible as of now. However, i think there is huge value in the stock and it can easily be a 5-10 bagger as soon as there are any signs of consolidation from management (on ground).

I am planning to replace quite a few non performing stocks (5-6% of total portfolio of small/mid caps anyway does’nt seem to go anywhere in the current market condition) with opto circuits. Would really be helpful to get some comments from more experienced guys.

There are business related issues here regarding product recalls which were not shared with the common investors. Also, the book value with significant percentage of goodwill from past acquisitions at inflated IP premium doesn’t hold much ground.

I recall a talk we had last August when we met at Baroda when Ayush had clearly suggested that Opto looks like a very good short candidate… It was around 120-130 levels and now down to 21 odd levels.

Thanks Rudra for your reply. Never knew about the product recalls. No pricecan be termedcheap in such cases. Wonder how they have kept mostinvestors in dark for so long.

Am really beginning to apprecaite the knowledge people have in this forum. Thanks again.

The author of the analysis of Opto Annual report needs to be congratulated. Reading such skeptical analysis, definitely refines one’s own analysis skills. Thanks to Rudra for sharing link.

Before anybody buys Opto Circuit they should read the above report on Opto Circuits. It has a lot of good questions that should make one think multiple times.

I looked at it today after the report around Goldman buying 26% in the company. However, having read part of the report convinced me to stop looking at this co any further. A lot of effort saved.

I too am holding a small quantity of Opto and was planning to add on to it. But look at the above report I have negative feelings about the stock now. But am still not sure why the prices have fallen so much from its earlier highs…and if its still a decent buy?

Once upon a time, Opto circuits was a darling of investors. This company could do no wrong. Dividends, bonuses, continuous growth, etc

Then came the disasters. Rating agencies, cash flow problems, key people resigning, corporate governance issues, etc

Would there by any time in the future where this stock could be once again considered as a multibagger potential? A turnaround?

Because some business fundamentals seem to be really good.

On the fundamental side a lot of negative news is built up in case of Opto circuits.

The company was forced to withdraw its GDR after keeping it open for 2 and half months.

The credit rating of the company was down graded to default grade.

There is no news on the receipt of insurance money for the damage caused by the Vizag cyclone.

Management just does not communicate anything with the investors.

And in this choppy market conditions, it is natural to expect a high debt company like opto to go down quite steeply and that’s what appears to be happening.

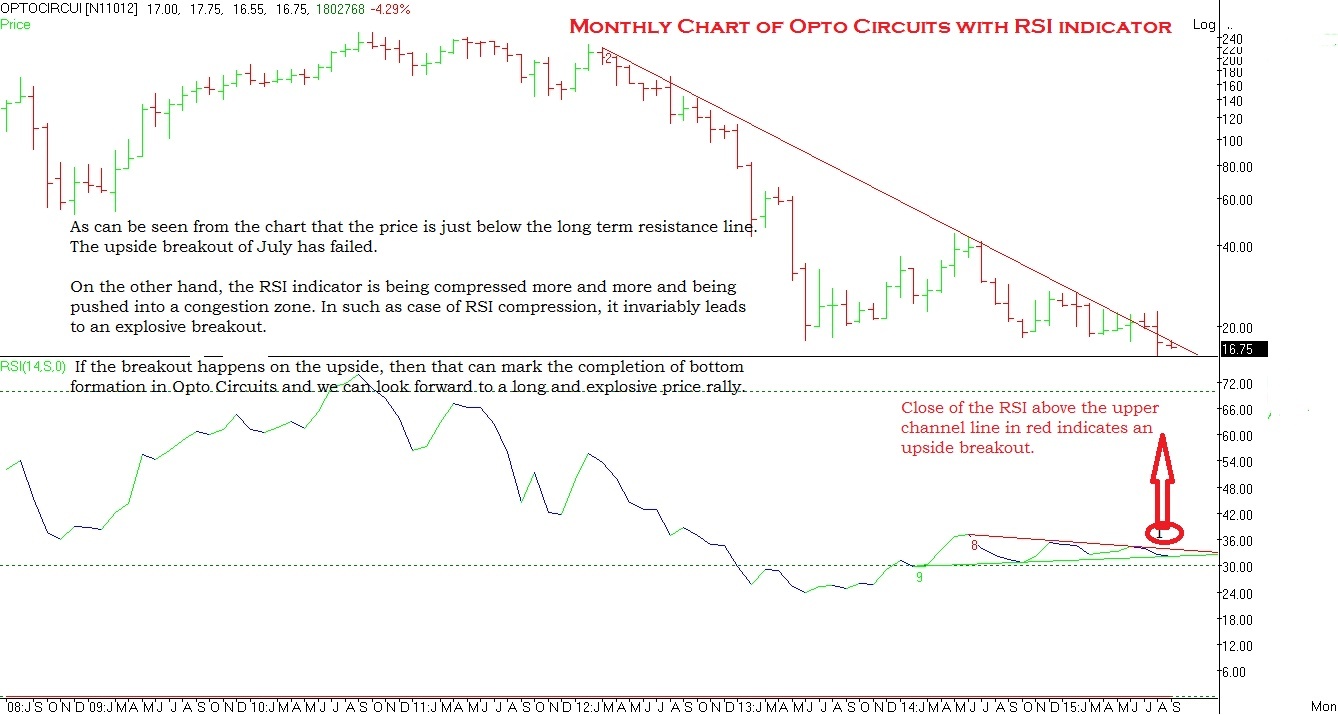

But Technically it seems that all this negative news is already priced in. AND if we shift our focus from daily charts to monthly charts, then it becomes apparent that if by the end of Sept 2015 the RSi does not go below the lower / support line, then there is a good chance of a bottom formation in Opto circuits as well as a bullish divergence on monthly charts. This is a very strong reversal signal.

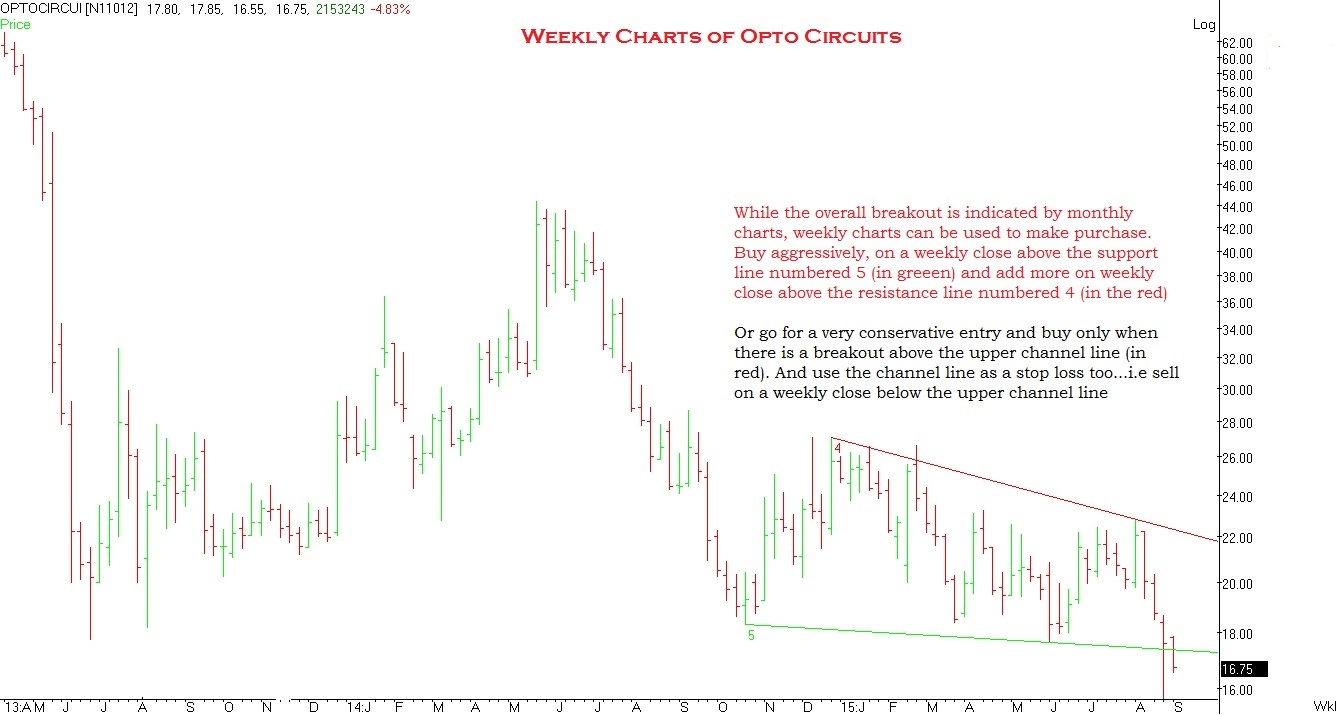

I have presented to investment strategies for those interested in opto circuit using weekly charts - Aggressive entry and conservative entry. Investors may consider using either of these to make an initial entry in Opto Circuits.

If bottom formation process is nothing but a process of dissipation of negative momentum; then it appears that the negative momentum is already dissipated to a large extent. Or in other words, all the sellers / weak hands may have been thrown out of the stock.

I had the opportunity to look at this company very closely when i was working in a bank in 2012. I noticed too many red flags during my due diligence and we declined a loan proposal at that time. Subsequently, our concerns came true!! Few learnings for me, from this are as below:

a) Try and connect with various stakeholders (banks, customers, suppliers etc) of a company to understand their operations in a better way. Here, i noticed CFO was way below their net profit. Then i dug deeper to understand their customers profile (as their receivables were spiralling up q-o-q). I realised, company had set up group companies in Singapore etc and have been raising invoices on these companies (and there was no cash realisation for days together). While q-o-q, company was showing higher profits, but i guess there was no actual cash realisation.

b) one of their existing banks was trying to terminate the relationship and move out. When, i enquired, i received a typical response that the company was not meeting their target returns for the bank and hence they wanted to move out. While, in such cases most of the well managed companies find a replacement bank easily, here company was struggling for some time to replace this bank.

c) MD& CEO meeting- post my meeting with them, i realised there is a lot more to read between the lines, as their responses were incoherent.

d) company borrowed short term funds and used them to purchase fixed assets. I think, auditor had even made a qualification to this effect.

Within a couple of months (from the time we declined the proposal), CFO of the company had resigned and thereafter stock fell like nine pins.

I joined VP forum this year. Today, i saw this thread and hence posting my reply now.

Thanks for sharing the history of Opto. I had a fairly large holding when

it crashed. At that time even well known stock advisory firms like Equity

Master were strongly recommending this stock.

Optocircuit is now a turnaround story.In FY18, it made a profit of 35.59 Crores, which turns out to be an EPS of 1.34(On consolidated basis). As base is low, it is expected to double its EPS to approximately 2.68. So it is a good candidate of re-rating.