thanks @rohitbalakrish_

Yes it appears so - went through some reports which point to this fact. I guess this seems to be a key risk in this particular segment of the business.

Though its good to see their growing emphasis and efforts to move on to higher margin products.

Omkar Speciality came out with decent set of results today for q1 fy 16.

One needs to look at consolidated numbers here.

Sales for q1 fy 16 improved to 90 cr from 54 cr in q1 fy 15.

Op profit for q1 fy 16 improved to 15.4 cr from 7.5 cr in q1 fy 15.

NP for q1 fy 16 improved to 8.1 cr from 4.8 cr in q1 fy 15.

EPS for q1 fy 16 improved to 4 from 2.4 in q1 fy 15.

Full year cons eps for fy 15 was 12 per share.

Company has expanded capacities and now those are bearing fruits.

@hitesh2710 Another +ve is that promoters pledging have come down to 34.72% as mentioned in result note 5c. With NP q-to-q jumping 50% and y-to-y 64%, it puts the p/e below 15 which looks attractive.

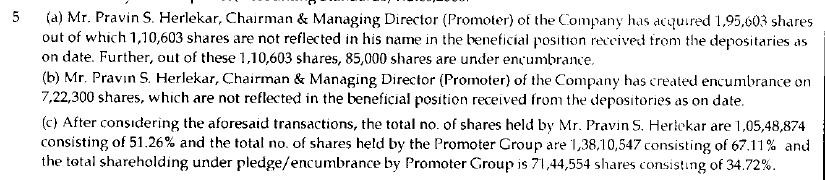

The q1fy16 and q4fy15 report has the following disclosure

I have the following question in relation to this disclosure

- Why the out of 1,95.603 shares acquired by Mr. P. S. Herlekar 1,10,603 not reflected in his name? Does depositories take so long to transfer shares in someone’s name?

- Why this disclosure has been made? What is the significance of this?

The sales increased by 70% and EBITDA margin improved by 300 basis points.

However, I am unable to fathom the depreciation policy … Q4 '15 Depreciation was Rs. 6.75 Cr whereas in Q1 16 the depreciation is only Rs. 1.82 Cr. when asset base increased from Rs. 188 Cr (Q4 14) to Rs. 268 Cr. (Q4 15)

Their working capital woes are still there as appears from the interest outgo.

Promoters pledge has reduced from 57% of their holding to 49% … It is a positive development unless the means are resorted again…

This could be due to new depreciation policy. There should be notes regarding it at end of results

Not sure about the 1st point.

On 2nd, I have seen this disclosure for past 3 quarters or so. Pledging went up in Q4 14 and has gone down again.

aveek,

If you consider y-on-y depreciation, it has increased from around 1.2 cr in q1 fy 15 to 1.8 cr in q1 fy 16.

I dont have much idea about how they divide the annual depreciation on quarterly basis, whether there is any specific ratio they follow for each quarter.

For the last 2 years, this has been the case… Q4 depreciation has been higher than the other 3 quarters.

Though I haven’t seen anything like this in any other company, but I guess they would using some formula to divide annual depreciation among quarters.

Any idea why the growth in FY15 was low? I understand the reasons for FY14 -low iodine prices etc, but am unbale to understand the reason for FY15. Their API unit is seeing stellar growth, what then is not driving the growth in topline, is it further decline in iodine prices?

Overall 2-3 things look very interesting to me - introduction of new products, reduction in client concetration, focus on exports & API business

Some other questions that I wanted to uderstand are below- would appreciate anyone’s views:

- What is driving their growth in API are they the only suppliers of these APIs?

- What is the share of exports for the company in FY15?

- Overall competitive scenario (domestic/international) of the company in various segments - viz Iodine, APIs & Others? I understand that they make some niche molecules and chemicals - can this be validated?

- Comfort on debt position and working capital- how can we get comfort on this aspect. debt levels are high given they need another 50-60 Crores of capex how will they fund it? Company also talks about QIP going forward .Their working capital hasn’t yet improved. Don’t know whats the situation in Q1, but if someone is meeting the management they can udnerstand this,

1 Like

Hi,

From HDFC sec report in 2012,

- around 80% of sales were commodity products. Iodine based products were around 45%. Does this mean that iodine based products are actually commodity products? Can’ts still figure out what compounds are niche?

- Also, i think stretched WC is a reflection of commodity nature of products. though this might change

- patents are for process, but we don’t know the advantages of it.

- from Crisil rating rationale WC can remain stretched.

For me improvements in WC will be big thing to track

Hitesh,

The point is from FY 14 to FY 15, NFA has risen by almost Rs. 80 - 90 Cr. and inspite of that depreciation is almost same.

Rohit,

All the API are for Veterinary segment but how big is the market I don’t know and trying to figure out. But I guess deworming, antiparasitic, anti-infection and these types of areas are well discovered and they don’t make anything unique but possibly regular quality supplier (this is my guess only, can’t prove as yet)

The list from their website is enclosed … It would be good if someone can find out who else makes these products and size of opportunity.

Veterinary API Products

Products –

Product CAS No. Product CAS No.

Fenbendazole 43210-67-9 Ricobendazole 54029-12-8

Toldimphos sodium 5787-63-3 Oxfendazole 53716-50-0

Cyromazine 66215-27-8 Closantel Base 57808-65-8

Albendazole 54965-21-8 Closantel sodium 61438-64-0

Triclabendazole 68786-66-3 Nitroxynil 1689-89-0

Rafoxanide 22662-39-1 Halquinol 8067-69-4

Ornidazole 16773-42-5 Oxyclozanide 2277-92-1

2,6-Diiodo-4-nitrophenol 305-85-1

The export turnover is increasing YoY as can be seen from their AR

Iodine products can’t be called a commodity though it’s price is tagged to a commodity (iodine) … The production of derivatives and handling of inorganic Iodine is not that simple process … It can be termed a specialized commodity by product say like products of Welspun Syntex (BCF) or Usha Martin (Wire Ropes)

Saurabh Shankar,

Yes, WC is the biggest drag … They talk of reduction by improving export etc. but from Interest expense figure of Q1 16 it seems their woes are yet to get mitigated.

http://www.omkarchemicals.com/cs%20pdf/PDFOnline.pdf

The link is of a dated interview but company seems to have walked the talk after coming with an IPO in 2011.These old interviews help in ascertaining the execution skills of the promoters.

The promoter is a first gen IITian entirely self made.He seems to understand the importance of R&D has a team of 30 scientists and has got patents also successfully several times.

At mktcap of 370 Cr,capex over so ROCE to improve from 13-14%,excellent recent results,huge opp size this company needs to be tracked closely

Another dated but useful interview

Vivek Gautam,

You have mentioned opportunity size is huge… Can you elaborate? Segment wise? With competitive landscape? In India, Samrat Petrochem and Caliber Chemicals make Iodine derivatives … Both are not doing well… Why?

Seems there is something special about Omkar but I am unable to specifically pinpoint except the R&D focus and trying to work in a niche area so doggedly over the years which seems possible because the key man is a scientist / techie type… So, if the opportunity size is big, it is worth digging at a much deeper level…

Your inputs would be helpful on opportunity size…

3 Likes

Sharing my consolidated set of questions. Will refine it further as I do more research

- We manufacture around 200 products, are there any few major products that drive our sales or is it fairly well diversified?

- We have added a lot of products over the last 2-3 years, when we look at adding a new product, what are the things that we look at before introducing a product - competition/market size/margins etc?

- From our existing product portfolio- what % can be termed as niche products and what are more commodity products? If possible can you possibly explain the competitive scenario in our 3 operating segments - Iodine derivates, API & Other intermediates

4.What is the opportunity size we see on our API segment? - In the iodine chemicals segment -who is the biggest player and how are we different from them?

- What was the share of APIs & Exports in FY15? In the next couple of years what kind of sales contribution will API & Exports have? If possible can you please share the operating margins in the export markets and APIs?

- In our con-calls you have talked about working capital getting improved. Can you please share how was the first quarter in terms of our working capital? By when do you expect the working capital position to stabilize. In terms of days - how much do you think you can improve the WC situation

- At what stage is our expansion program? Have we added 3000 MT of capacity in Unit 5? What abut the plans for other units? How are we planning to finance this expansion given we need another 60-70 Crores to fund it… is it going to be QIP or more debt or internal accurals.

3 Likes

Omkar management came on Ndtv profit to discuss Q1 results, link of which is below-

Summary of the interview is as below-

- Q1 growth led by API segment; growth from API will continue

- Filed DMFs in Europe, Latin America

- Looking at Export-Domestic ratio of 50:50

- Prices better in local, WC better in export

- Monopolistic products

- Looking at Pat margin of 11%

- Order book of 220 crs

- Current capacity utilization is 65%

- New capacity coming, this will double existing capacity

- Can go up to 750 crs of top-line

- Veterinary API market size is 4000 crs

- Market ready in-front of company

3 Likes

Great to have a thread on Omkar. Do they have a working capital issue as is mentioned above?

They have a working capital of about 160 cr when i checked in screener.in and wcr of 3…Can someone explain more on the working capital issue…

The 2nd Gen promoter interview will answer your questions on opp size.

1)Seems OSCL is a leader in veterinary API mkt which itself alone is approx 4000 Cr

2) Post expansion company is targeting turnover of 750 Cr

3) Seems demand is not a problem as co is sitting on an order book of 220 Cr

4) Most of the products are monopolistic patented products

5) Co invests heavily into R & D founder being a IITian Techie scientists

6) Once operating leverage sets in EPS & topline cud rise sharply

7) Co makes large no of projects

Discl-invested post results recently

A dated but informative interview of founder Pravin Herlekar.

Co is having qtrly negotiations with all its customers so is able to pass on the RM fluctuations.

2 Likes