If one looks at China, it is not difficult to learn that both EV 2 wheeler and EV 4 wheeler is a business with hardly any technological moat. PPFAS did a good session on EV cars in China which has very interesting insights. It is a brutal business and only the top guys are making decent money, everyone else is losing money.

Being extremely cost efficient is very important for Ola to survive the competition and possibly thrive if there is consolidation in the market. As of now profitability still looks a reasonable distance away. Unlike Ather who are in the premium end, OLA is like Samsung in mobile phones trying to throw everything at the market and see what sticks.

Not in a hurry to invest, will continue tracking. At some point the path to profitability will be clear and that might be a good time to re-look at price and take a buying decision.

Insolvency petition filed against Ola Electric

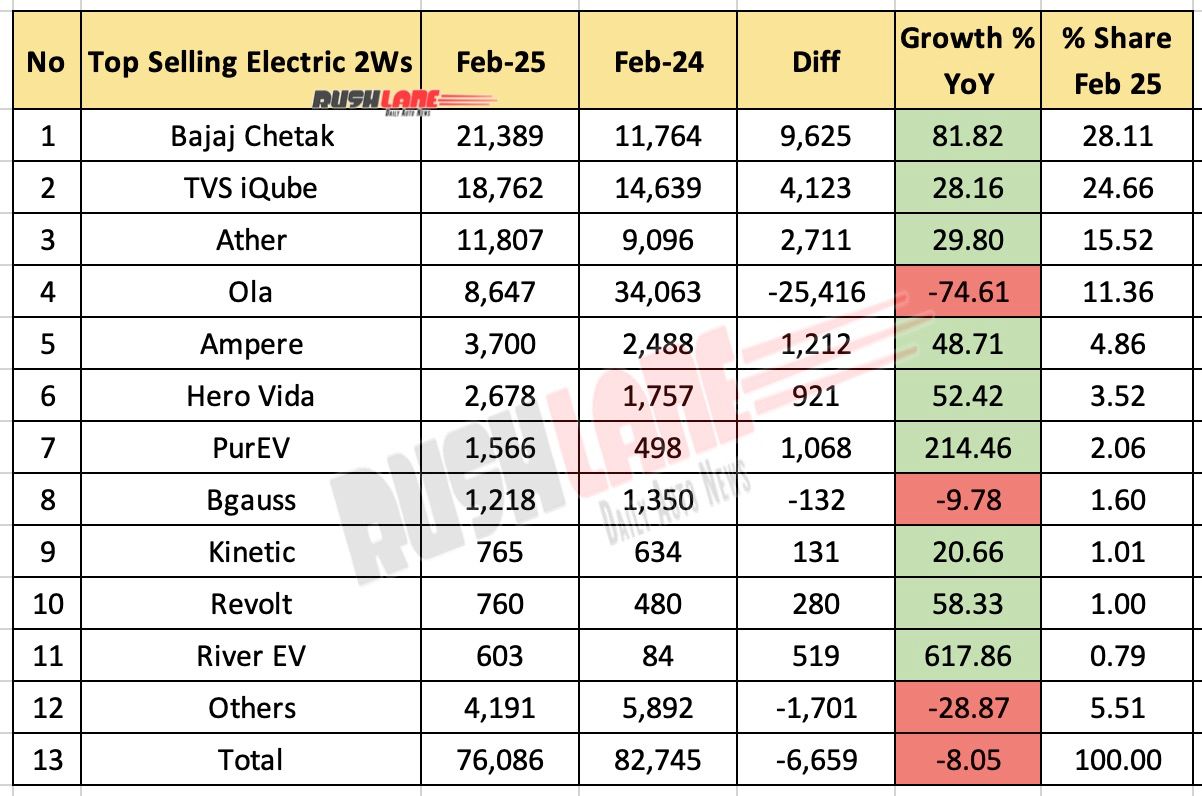

The developments seems to suggest a clear pattern where Ola is facing cash flow crunch as it is is losing its market share while traditional players like Bajaj ,TVS are beating them EV sales and even pure play EV players like Ather and Ampere are showing good growth while Ola sales is degrowing.

I think the data is incorrect as OLA Electric has reported sales of over 25000 2W in Feb 2025 as told by Mr. Bhavish Aggarwal in Q3 2025 concall maintaining about 28% market share of the 2W Feb sales.

It seems the data has been intentionally engineered to make figures look poor for OLA.

I am not denying that there aren’t any challenges for OLA but if there would have been no challenges then it would not have been selling at these price levels.

Dis- Invested. Views may be biased.

They have already clarified regarding this in a BSE press release dated 28 February 2025.

The company recently announced the renegotiation of its contracts with its vehicle registration agencies, a move that temporarily affected registration numbers on the VAHAN portal during February 2025. The negotiations aim to reduce costs and streamline the registration process.

Interestingly the reason provided by Bhavish was "“We are renegotiating the terms of agreement with our agencies, namely Rosmerta Digital Services Private Limited " and this is the same company which has filed insolvency proceedings against Ola.

I hope it’s just the negotiation of dues , which ola owes to Rosmeta , gone wrong.

And vendor is using legal route to get his dues, nothing wrong with that.

However I hope ola isn’t facing cash flows concerns / cash crunch/ working capital issues.

March sales units aren’t encouraging, however company hasn’t shared the backlog numbers , I think they don’t wanna catch further attention of govt. Agencies.

My sense is the units sold would be more, since just Feb backlog was pending by a good number of units.

The actual sales numbers as per vaha might not show the actual picture interns of units sold even in the month of March

Important snippets from concall:

Due to reduced expenses co is now expecting breakeven at 25000 units/ months.

Rs.250 Cr one-time warranty provision in Q4 FY25 addresses legacy issues, with future warranty costs expected to be lower due to platform improvements.

Disc: Invested and suffered but feels not time to exit. Co not given single positive news since IPO. This is just my note, no buy sale recommandation.

Exited in huge losses post concall.

Didn’t find a thing that could be positive in a concall.

Plus all the analysts were soft on asking some basic questions or accountability of the management, that seemed fishy.

On operational front, company expects break even at half the number of units, gross margins don’t improve that fast.

With no stores company was doing sales of around 3 times the units that it is doing now with 4000 stores.any operational guy would tell u , that u expand stores, when u are unable to meet the demand from existing stores, but here case is vice versa, sales are going down and expansion is happening.

They are unable to compete, they had first mover advantage, but when legamcy auto makers pressed the accelerator they succum.

And going forward I see legacy automakers only up the anti , and widening their portfolio.

Ola has the widest portfolio, yet it’s slipping in market share.

Bajaj and tvs are only gonna widen their range ,if ola isn’t able to compete now how is it gonna stay relevant then?

Still invested , bet on Bhavesh instead of prduct, He is single handely all the issues can note in all con calls , Super personeality , ( I know finance does not consder emotions but when you compare other start ups like PTM Zepto Zomato all are great but they just have to manage Platform but OLA is different from them ). Believe it or not it will not close it can be last but " No body knows " time can change. He is on it. Iam baised Invested.

Bhavesh has his two legs in twenty boats, which leads to lack of focus and hence issues keep arising one after the other.

Every sector they are working in has a lot of competition and needs a great team everywhere for seamless execution which will then translate to good numbers as well. But reports of culture issues are also plenty.

Still, I hope they are able to turn things around.

Disc : Invested twice and thankfully exited every time at a small profit. Will re-enter only if available at a bargain (in 30s).

TVS motors MD’st CNBC interview snippets on rare earth materials.

“same time now there is this whole supply chain challenge in terms of China

banning the export of rare earth high rare earth hre magnets which are

actually very important for our motors and other parts of the EVs so this EV

supply chain disruption is certainly going to pose a short to medium-term

challenge”

OLA mentioned below in their concall:

We continue to push boundaries on engineering through focused global-first innovations such as a unified 48V architecture across all components and peripherals. Our engineering roadmap has included a rare-earth-free motor for more than a year now, pre-empting currently ongoing supply chain risks. We expect to introduce this in our products by the end of the current calendar year.

Interesting developments going forward. Disc: As mentioned in recent post in same thread.

The question is : Can they execute?

He wanted to reach 5GW battery production capacity by FY25, and 20GW till FY27, which is now changed to just 5GW by FY27. Usage of own cells in vehicles also delayed.

If they are saying to introduce a rare-earth free motor by year end, then expect that they are also going to face the supply chain risk for entire FY25-26.

Another question, as I am not much aware of these EV parts - Is motor the only component which includes rare-earth metals?

Some clarity on this will be much appreciated.

Everyone and their dog is bearish on Ola right now. We have 16 lakh retail investors holding about 10000 crore worth of shares. Institutions have largely exited. The question arises : why are people still invested in it? Is it inertia, hope, imprudence or a combination of all of the above?

I looked at the stock recently and got somewhat interested. The company does have decent IP. It is innovative and despite losing share, is among the top 3 in the category. It has a production capacity to propel it to top if the demand comes back. The founder is brilliant even if brash(perhaps required in today’s environment). There is a plan in place to claw back its lost sales. The product is performing decently(as gathered from various rapido drivers who have been using for last 2 years). There are sector tailwinds which will continue to grow the market size at least for half a decade at a furious pace(25-30%) so that it quadraples by FY 31. Just survival and holding on to current market share will make Ola quite profitable by then so valuations from current levels would look okish. Currently, we are at 4 times price to sales. It could be 1 times price to sales by then and at decent margins that ola has, quite a low pe multiple. So the only real question is : will Ola survive next 5-6 years?

I think it should. However, there are many roadblocks. I see the capital intensive nature of business as a threat. By going for vertical integration and D2C, company has significantly more capital requirements than competitors, who are asset light or have accumulated cash reserves of decades. Maybe they can demerge and sell battery business down the line or maybe do a tieup with some other 2W company for distribution. Remains to be seen. Focus of founder is needed on the company. He is running 3 companies in very different sectors and may decide he needs to also go to space like Elon. Or may decide to make a car before the 2W business is stabilized. I hope the share market has taught him a few lessons. A pandemic like situation again or a recession would lead to collapse of demand, so that is a macro risk.

On balance, I would say this might a good chance to accumulate to around 1-2% of portfolio. There is a decent chance it would outperform.

I for one have started with equal allocation to Ola and Ather. Maybe reevaluate every quarter and may decide to shift to whoever is winning. I see that EVs are here to stay and grow. Let us hope we make some money out of it.

Disc : started investing at recent levels. Can sell tomorrow too. Biased. DYOR.

How is this a requirement in today’s environment?

If you are brash like Bhavesh - you wouldnt have new loyal team? He openly uses foul language in office, treats his employees as cattle, keeps firing people at his own whim and fancies. This attitude doesnt build team.

I have 2-3 friend who worked at Ola, so this is a 1st hand experience…not hearsay.

if he needs Ola’s fortune to reverse, he needs to change his sick attitude.

Your observation is correct that it does alienate people. My view is that his brashness is a sign of disappointment at being frustrated by his team. All innovation comes from a bold vision. He did create the entire category and under consideration extreme pressure, people do perform. His speedy of execution is very good.

He will ultimately find a team and perhaps mellow down a bit too.

We can have different views on this, but in my opinion this is going to be cutthroat business. You can’t be polite and survive here.

Having read multiple biographies of founders (more so about Steve Jobs or Elon Musk and many more), have all succeeded not being nice to the team members. I feel these founders by nature differently wired and only way to get the team to deliver on their vision is being brash.